Reassessing Iridium Communications (IRDM) Valuation After A Sharp Share Price Run And Conflicting Fair Value Signals

Iridium Communications IRDM | 0.00 |

Why Iridium Communications (IRDM) is Back on Investors’ Radar

Iridium Communications (IRDM) has drawn fresh attention after a strong recent run in the stock, inviting investors to reassess how its satellite communications business lines up with their portfolio expectations.

The recent momentum is hard to ignore, with a 31.29% 1 month share price return and a 191.55% year to date share price return. This compares with a 105.71% 1 year total shareholder return and a 10.49% decline in total shareholder return over three years, suggesting short term enthusiasm has picked up against a more mixed longer term record.

If Iridium’s recent surge has you looking beyond a single stock, this could be a good moment to widen your watchlist using the 33 power grid technology and infrastructure stocks

With Iridium trading at $51.78 against an analyst price target of $36.38 but carrying an estimated 44% intrinsic discount, you now face a key question: is there still an opportunity here, or is future growth already priced in?

Most Popular Narrative: 34.1% Overvalued

According to the most followed narrative, Iridium’s fair value sits at $38.60, which is well below the recent close at $51.78. This sets up a clear valuation gap that investors are trying to make sense of.

Iridium Communications (IRDM) represents a compelling long-term investment opportunity driven by its strategic positioning in the satellite communications industry and its recent acquisition of Satelles. This acquisition enables Iridium to leverage its existing infrastructure to capitalize on the growing demand for secure positioning, navigation, and timing systems (PNTS) as alternatives to aging GPS technology.

Want to understand why this narrative still lands below today’s price? It leans heavily on expanding PNTS demand, steady service and IoT revenue growth, and a profitability profile that assumes disciplined capital allocation over the coming years.

Result: Fair Value of $38.60 (OVERVALUED)

However, that story can crack if Satelles integration stumbles or if PNTS adoption is slower than hoped, which would limit the payoff that current optimism assumes.

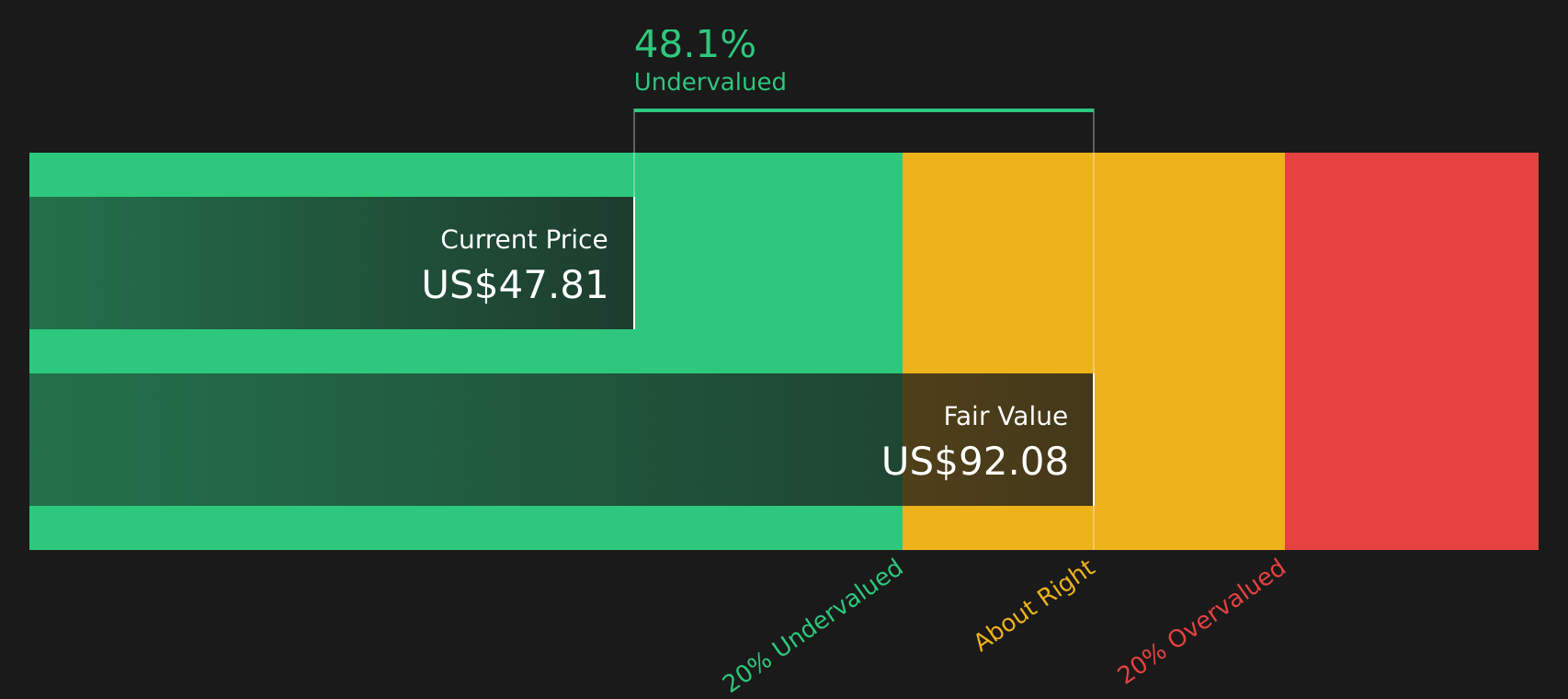

Another View: Cash Flows Point in the Opposite Direction

That 34.1% overvaluation call based on a $38.60 fair value is only half the story. Our DCF model, which prices Iridium at $92.10 per share, frames the current $51.78 level as trading at a 43.8% discount instead. Which lens do you trust when the signals clash this sharply?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Iridium Communications for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value and sentiment, the real question is what you take away from the data and how quickly you act on it. Before you decide where you stand, weigh both the upside and the caution flags highlighted in the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Iridium has caught your eye, do not stop here. Broaden your opportunity set with a few targeted stock ideas that match different portfolio goals.

- Hunt for potential mispricings by reviewing the 46 high quality undervalued stocks that combine quality fundamentals with subdued expectations.

- Strengthen your income stream by focusing on the 10 dividend fortresses that aim to pair higher yields with resilience.

- Protect your capital by concentrating on the 63 resilient stocks with low risk scores that show lower risk scores without giving up on quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.