Reassessing Target (TGT) Valuation As Short Term Momentum Contrasts With Longer Term Shareholder Returns

Target Corporation TGT | 119.53 119.44 | +1.40% -0.08% Pre |

Why Target (TGT) Is Back on Investors’ Radar

Target (TGT) has moved onto many watchlists after recent share price swings and fresh valuation signals, with some investors reassessing how its current pricing lines up against its fundamentals.

Recent moves in Target’s share price have been relatively steady, with a 30 day share price return of 5.41% and a 90 day share price return of 28.77%. This contrasts with a 1 year total shareholder return of 5.33% decline and a 5 year total shareholder return of 29.10% decline, which suggests short term momentum has picked up while longer term holders have seen weaker outcomes.

If this has you rethinking where retail fits in your portfolio, it could be a good time to broaden your search and check out 23 top founder-led companies.

With Target trading at $115.76 against an intrinsic estimate that suggests a 17.39% discount, but sitting above the analyst price target, you have to ask: is there real value left here, or are markets already pricing in future growth?

Most Popular Narrative: 19.9% Overvalued

Compared with Target’s last close at $115.76, the most followed narrative pegs fair value closer to the mid $90s. This sets up a clear gap for investors to weigh.

The analysts have a consensus price target of $103.688 for Target based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $135.0, and the most bearish reporting a price target of just $82.0.

Want to see what is really behind that mid $90s fair value? The narrative leans on modest revenue growth, pressured profit margins, and a future earnings multiple that sits below many peers. Curious which specific assumptions pull the valuation down from today’s price, yet still support solid profitability expectations?

Result: Fair Value of $96.52 (OVERVALUED)

However, there is still a chance that faster progress in owned brands or higher margin digital segments could challenge the idea that Target’s shares are overpriced today.

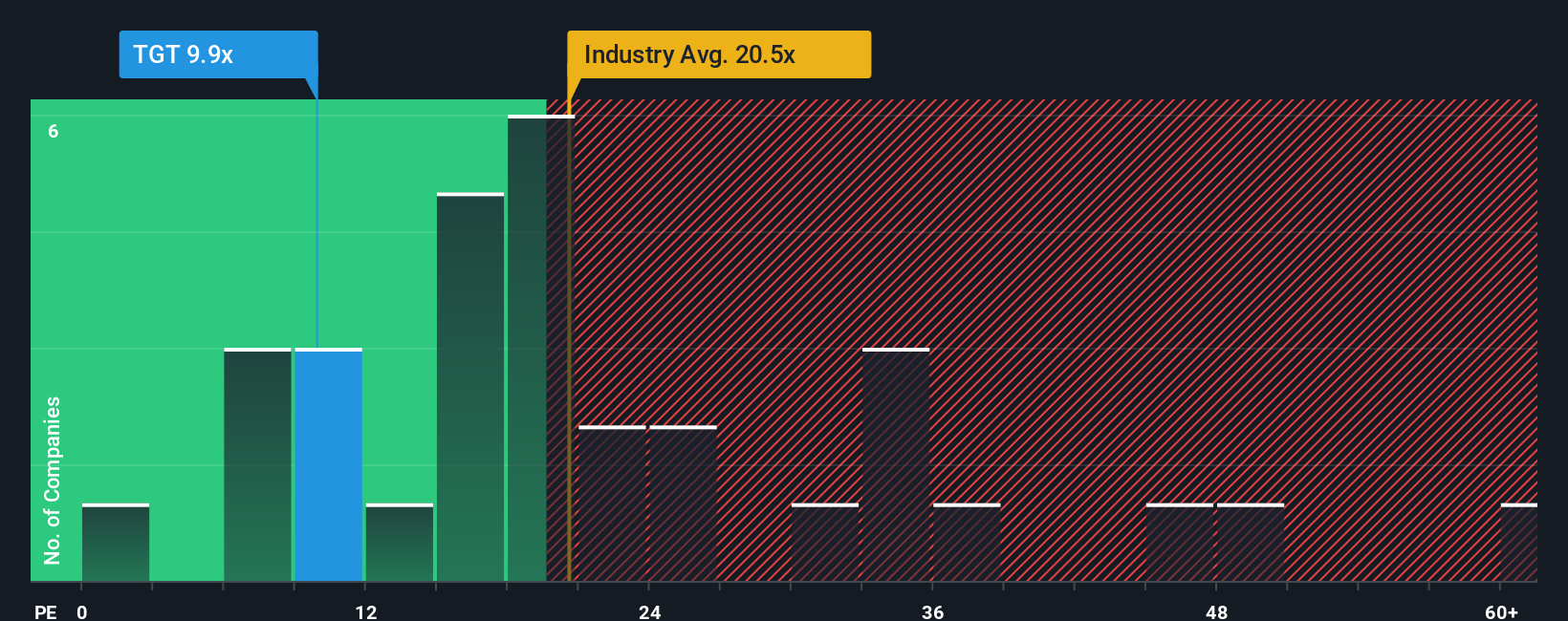

Another View: Earnings Multiple Sends a Different Signal

While the most popular narrative tags Target as roughly 19.9% overvalued against a $96.52 fair value, the earnings multiple story is very different. At a P/E of 13.9x versus 23.4x for the US Consumer Retailing industry, and a 31.7x peer average, the stock screens as cheaper than both.

The fair ratio sits at 20.2x, well above today’s 13.9x. This suggests the market could move closer to that level if sentiment shifts. The question for you is whether this discount reflects real risk, or a pricing gap that eventually closes.

Build Your Own Target Narrative

If you see Target differently, or you prefer to weigh the numbers yourself, you can pull the key data together and Do it your way in just a few minutes.

A great starting point for your Target research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready to hunt for your next idea?

If Target has sharpened your thinking, do not stop here. The real edge comes from comparing opportunities side by side and seeing where the numbers truly stand out.

- Spot potential bargains quickly by scanning companies trading on attractive fundamentals through our 53 high quality undervalued stocks.

- Prioritise resilience first and check out stocks that aim to keep risk in check using the 85 resilient stocks with low risk scores.

- Expand your watchlist with under followed names that still show solid financial traits via our screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.