Record Backlog And Narrower Losses Could Be A Game Changer For Boeing (BA)

Boeing Company BA | 0.00 |

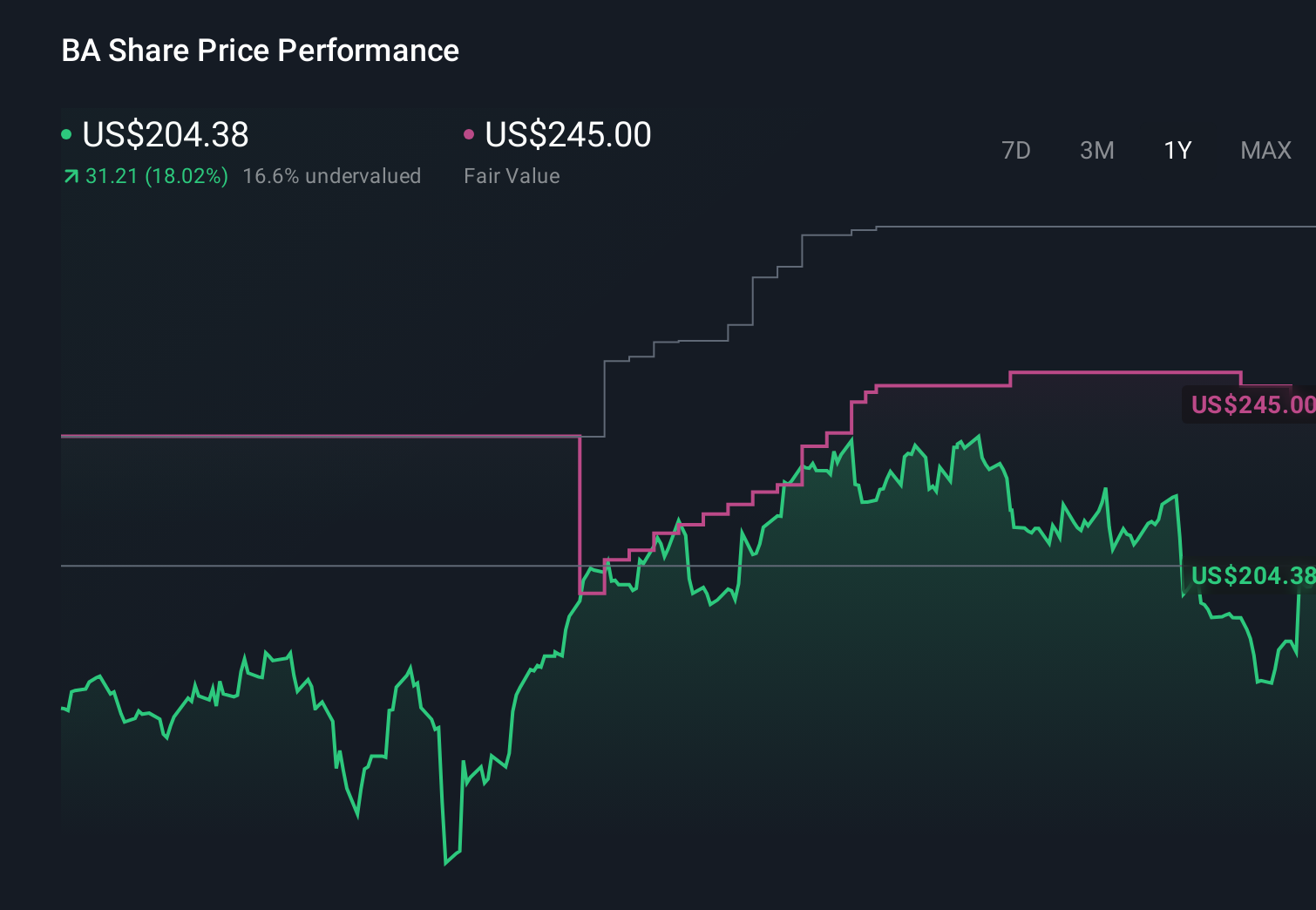

- In the first quarter of 2026, Boeing reported revenue of US$22,217 million versus US$19,496 million a year earlier, with its net loss narrowing to US$4 million and loss per share from continuing operations improving to US$0.11.

- Alongside this earnings improvement, Boeing’s record US$695.00 billion order backlog and higher commercial jet deliveries highlight substantial embedded demand across both its commercial and defense businesses.

- With this backdrop of stronger-than-expected Q1 results, we’ll now examine how rising aircraft deliveries and record backlog influence Boeing’s investment narrative.

Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

Boeing Investment Narrative Recap

To own Boeing today, you generally have to believe it can convert a record US$695.0 billion backlog and rising deliveries into durable profits while managing certification, execution, and balance sheet risks. The latest Q1 2026 beat supports the near term catalyst of higher 737 and 787 output, but the biggest risk remains program delays and quality issues that could slow cash generation and keep commercial margins under pressure.

Within the recent news, the Q1 2026 earnings release is the most relevant, as it ties directly to that backlog and delivery story. Revenue rose to US$22,217 million and the net loss narrowed to just US$4 million, helped by 143 commercial aircraft deliveries. This operational improvement matters because it tests whether Boeing can work through its order book efficiently enough to strengthen cash flow while still contending with certification milestones on the 737-7, 737-10, and 777X.

Yet beneath the improving numbers, investors should still watch Boeing's high debt load and ongoing certification and quality risks that could...

Boeing's narrative projects $122.7 billion revenue and $7.8 billion earnings by 2029. This requires 11.1% yearly revenue growth and a roughly $5.9 billion earnings increase from $1.9 billion today.

Uncover how Boeing's forecasts yield a $271.21 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already projecting revenue of about US$132.7 billion and US$11.7 billion in earnings by 2028, which sits in clear tension with ongoing quality control and certification risks, and Q1’s progress may push those narratives in very different directions depending on how you see Boeing’s recovery path.

Explore 9 other fair value estimates on Boeing - why the stock might be worth just $233.50!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Boeing research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Find 56 companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 31 stocks are leading the charge.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.