Record-Beating Quarter And Higher Guidance Might Change The Case For Investing In EMCOR Group (EME)

EMCOR Group, Inc. EME | 0.00 |

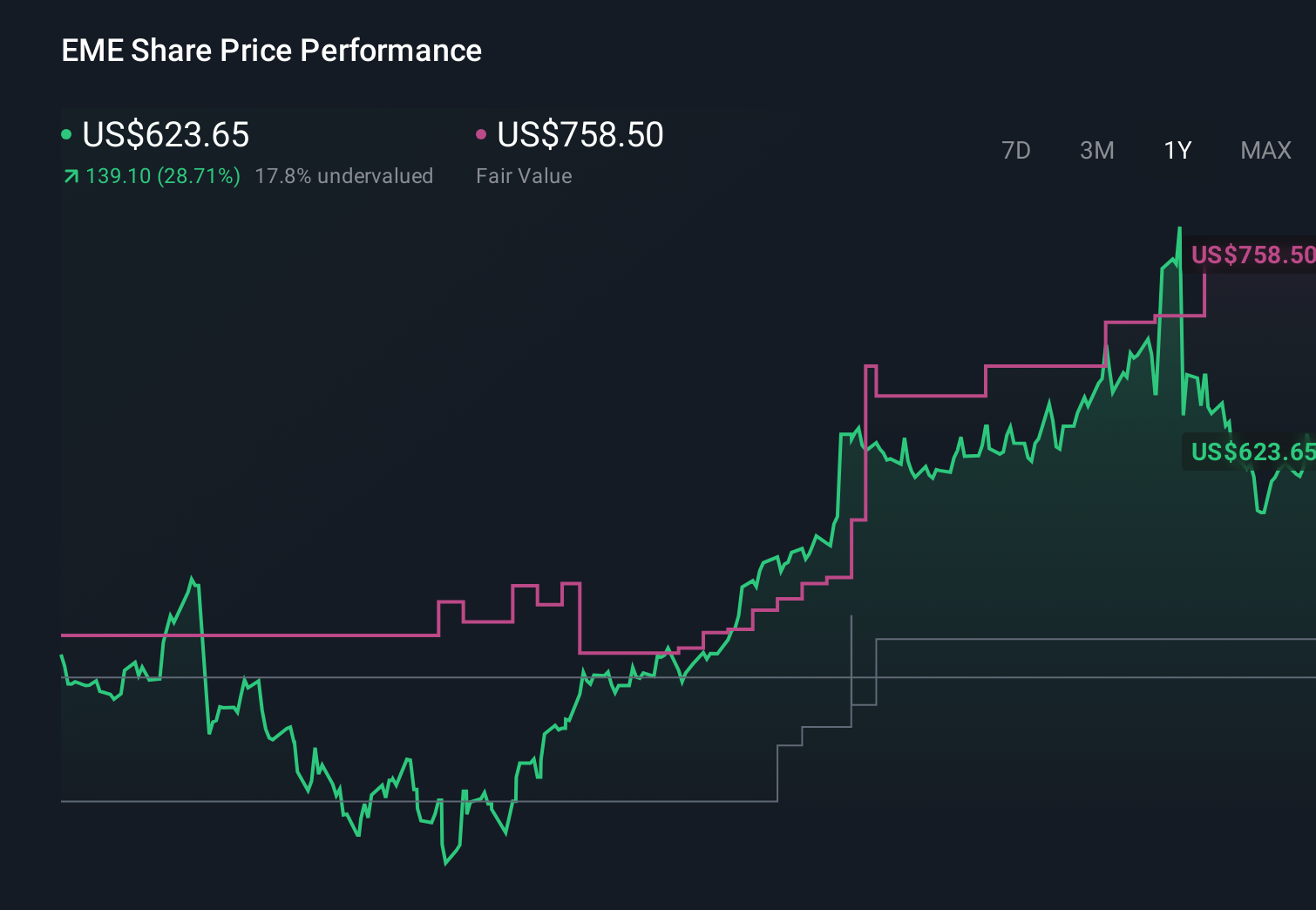

- Earlier in 2026, EMCOR Group reported record quarterly revenues and operating income, beating expectations and lifting its full-year revenue guidance above prior analyst forecasts.

- Management also pointed to strong bookings and sustained momentum across key end markets, suggesting its growing project pipeline is translating into operational efficiencies and higher returns on capital.

- With EMCOR’s raised revenue guidance now on the table, we’ll examine how this operational strength influences the company’s existing investment narrative.

This technology could replace computers: discover 30 stocks that are working to make quantum computing a reality.

EMCOR Group Investment Narrative Recap

To own EMCOR Group, you need to believe its record revenues, rising guidance, and healthy backlog can offset exposure to cyclical end markets and labor cost pressures. The latest beat and higher 2026 revenue outlook reinforce the near term catalyst around backlog conversion and margin resilience, but they do not remove the key risk that a slowdown in data centers, industrial, or energy projects could quickly weigh on volumes and earnings.

The most relevant recent announcement is EMCOR’s April 2026 guidance raise, lifting full year revenue expectations to US$18.50 billion to US$19.25 billion while holding operating margin guidance steady at 9.0% to 9.4%. This ties directly to the current story: strong bookings and execution are feeding into higher expected sales, while management still has to prove it can sustain margins if labor costs rise or large project awards become more episodic.

But against these strong headlines, investors should still be aware of the risk that concentrated exposure to large, cyclical projects could...

EMCOR Group's narrative projects $21.5 billion revenue and $1.6 billion earnings by 2029.

Uncover how EMCOR Group's forecasts yield a $983.50 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Compared with consensus, the most optimistic analysts see EMCOR’s high tech and retrofit work as a springboard, projecting roughly US$25.0 billion of revenue and US$2.1 billion of earnings by 2029, which is a far more bullish take on how today’s record results and raised guidance might reshape the company’s long term risk and reward profile.

Explore 5 other fair value estimates on EMCOR Group - why the stock might be worth as much as 47% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your EMCOR Group research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free EMCOR Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EMCOR Group's overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Find 44 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.