Recursion Pharmaceuticals (RXRX): Exploring Valuation as AI Expansion, Key Merger, and Clinical Progress Boost Interest

Recursion Pharmaceuticals, Inc. Class A RXRX | 0.00 |

Recursion Pharmaceuticals (RXRX) saw its stock gain momentum as investors reacted to several developments, including its Exscientia merger, progress on new oncology drugs, and updates on upcoming late-stage clinical trials.

The latest rally in Recursion Pharmaceuticals’ share price comes on the back of optimism surrounding its AI-driven drug discovery platform, major partnership news, and progress toward late-stage clinical milestones. After a bumpy first half of the year, momentum has clearly shifted, with a 33% 1-month share price return helping to offset earlier declines. While total shareholder return for the past year remains negative, recent investor enthusiasm and strong news flow suggest that sentiment is warming up as the company enters a pivotal phase.

Curious about other innovative healthcare names catching attention? Explore new opportunities with the See the full list for free.

With the stock rallying and upcoming data on the horizon, the real question for investors is whether Recursion Pharmaceuticals is trading below its true worth, or if the recent excitement means any future upside is already included in the current price.

Most Popular Narrative: 2.6% Undervalued

Recursion Pharmaceuticals’ current share price of $6.30 sits just below the widely watched narrative fair value estimate of $6.47. The modest gap is fueling debate over what’s driving the latest analyst consensus. With that backdrop, the next quote lays out one of the most important factors behind this valuation.

Rapid integration and iterative improvement of the Recursion OS 2.0 platform, incorporating advanced AI and ML tools (such as Boltz-2 and causal AI for clinical trial design), are expected to drive faster, more cost-effective drug discovery and development, improving R&D efficiency and supporting long-term margin expansion.

What’s the secret behind this fair value? There is a dramatic expected leap in growth that is anything but ordinary for drug developers. Want to see which aggressive future assumptions propel this number? Click to uncover the optimism and the underlying numbers that inform this narrative’s bold target.

Result: Fair Value of $6.47 (UNDERVALUED)

However, persistent reliance on pharma partners or setbacks in clinical trials could quickly undermine Recursion’s positive outlook and challenge its prospects for long-term growth.

Another View: Price Ratio Tells a Different Story

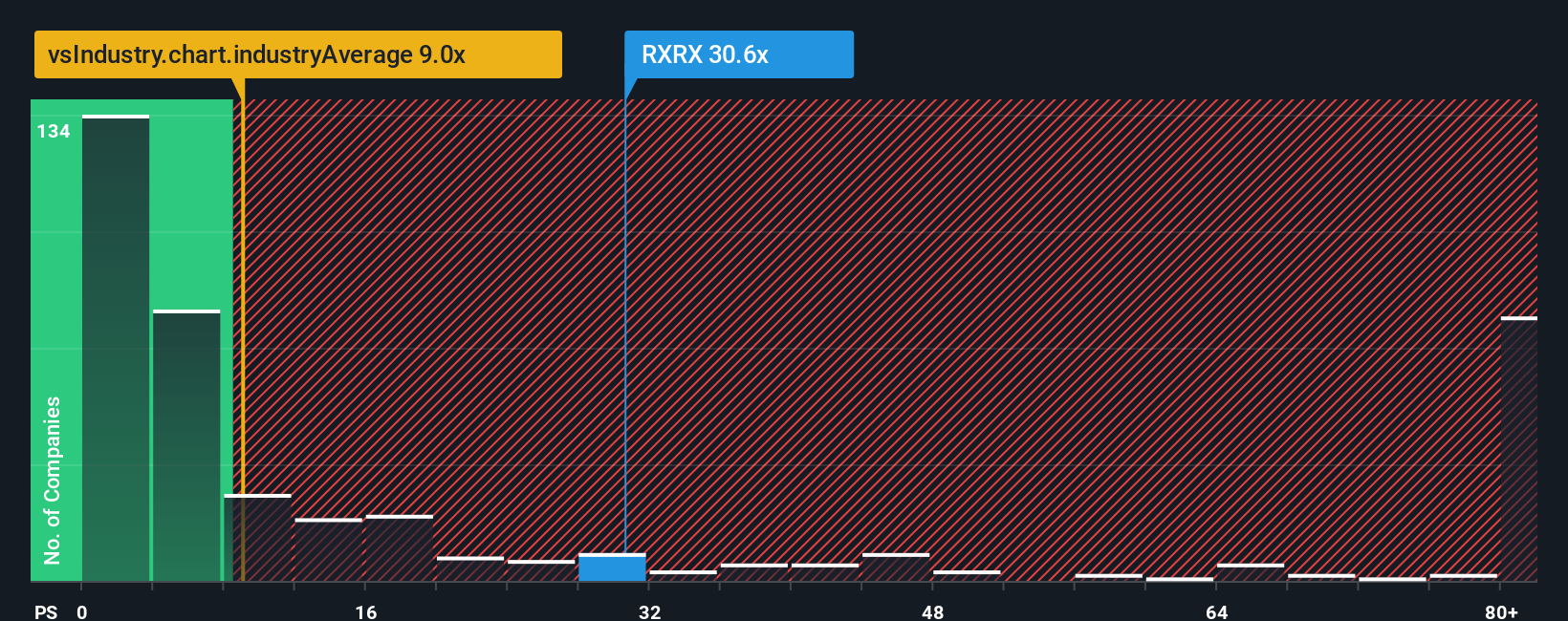

Looking beyond fair value narratives, market pricing tells its own tale. Recursion’s price-to-sales ratio is 42.6x, significantly higher than both its US biotech peers at 11.3x and its closest sector rivals at 15.8x. Even the modelled fair ratio is dramatically lower, which may point to considerable valuation risk if the market sentiment shifts.

Build Your Own Recursion Pharmaceuticals Narrative

Prefer to approach the numbers from your own angle, or put together a different story? Dive into the data and shape your personal view in just a few minutes with Do it your way

A great starting point for your Recursion Pharmaceuticals research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for More Smart Investing Ideas?

Don’t wait for the next headline to move the markets. Get ahead by targeting stocks with strong fundamentals, future themes, and untapped value using powerful filters.

- Target reliable passive income. Review these 19 dividend stocks with yields > 3% that consistently deliver attractive yields above 3% to help grow your portfolio’s earnings.

- Ride the future of automation and data. Act early with these 27 AI penny stocks that are revolutionizing industries by harnessing advanced machine learning and artificial intelligence.

- Unearth serious bargains. Zero in on these 870 undervalued stocks based on cash flows that may be trading below their true worth according to cash flow analysis, giving you an edge over the crowd.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.