Redwire (RDW) Valuation Check After Edge Autonomy Integration And Shift To Space And Defense Tech

Redwire Corp RDW | 9.73 | +7.16% |

Redwire (RDW) is reshaping its business after fully integrating the Edge Autonomy acquisition, unifying uncrewed aerial systems and defense technology under one brand while restructuring around two core segments: Space and Defense Tech.

Redwire's share price has recently cooled, with a 1-day share price return showing a 4.88% decline after earlier gains. The 30-day share price return of 39.09% suggests momentum has recently been building, even as the 1-year total shareholder return shows a 26.42% decline, which contrasts with a very large 3-year total shareholder return around 3.8x.

If Redwire's mix of space infrastructure and defense tech has caught your eye, this could be a good moment to see what else is moving among aerospace and defense stocks.

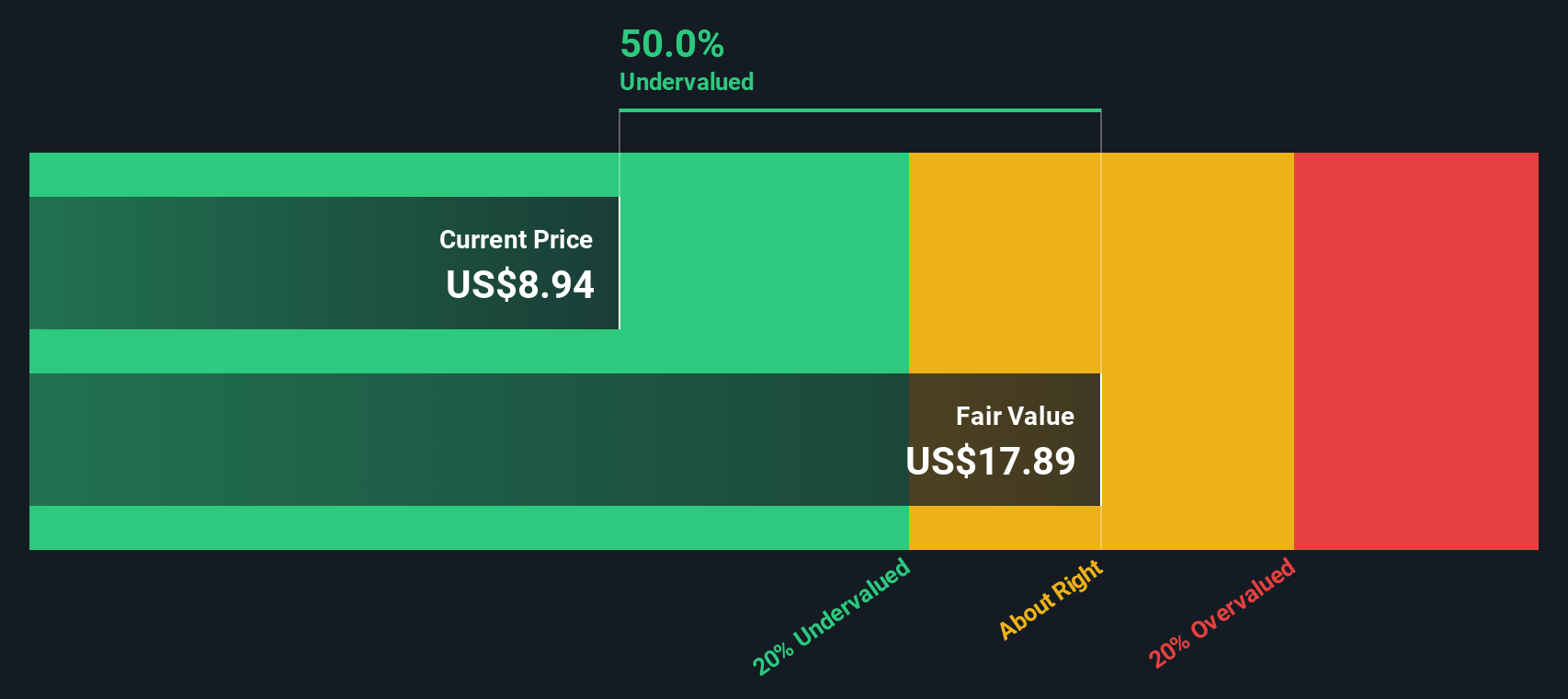

With Redwire now trading at US$10.14, sitting below a US$12.00 analyst target and showing a very large 3 year return alongside ongoing losses of US$268.028 million, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 23.3% Undervalued

With Redwire last closing at US$10.14 against a narrative fair value of about US$13.22, the story centers on how future contracts and margins could reshape the picture.

The rapid proliferation of commercial satellites and upcoming public/private low Earth orbit projects continues to build demand for Redwire's advanced in-space manufacturing, deployable structures, and subsystems, supporting multi-year visibility on high-margin product sales and recurring earnings.

Curious what kind of revenue expansion and margin reset would need to line up to support that valuation gap? The narrative leans on aggressive top line growth, improving profitability assumptions and a rich future earnings multiple tied to a maturing contract base. The full picture connects those moving parts into one valuation roadmap.

Result: Fair Value of $13.22 (UNDERVALUED)

However, execution missteps on large fixed price contracts, or prolonged government funding delays, could quickly challenge the optimistic revenue and margin assumptions that investors are leaning on.

Another Way To Look At It

While the popular narrative points to Redwire trading about 23.3% below an estimated fair value of roughly US$13.22, our SWS DCF model paints a very different picture. On that view, fair value comes out around US$0.27 per share, which would imply the stock screens as expensive rather than undervalued. For you, the real question is which story feels more realistic given the company’s current losses and execution risks.

Build Your Own Redwire Narrative

If you see the data pointing in a different direction, you can stress test every assumption yourself and build a fresh thesis in minutes. Do it your way

A great starting point for your Redwire research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Redwire has sharpened your focus, do not stop here. The wider market is full of other angles that could fit your goals even better.

- Spot early movers by scanning these 3532 penny stocks with strong financials. These combine smaller market caps with balance sheets and financials you can actually analyze.

- Tap into potential growth stories across these 25 AI penny stocks, where artificial intelligence themes meet listed companies you can track in detail.

- Zero in on value focused ideas using these 884 undervalued stocks based on cash flows. These flag companies priced below their estimated cash flow based worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.