Redwire (RDW) Valuation Check After SHIELD Contract Access To US$151b Missile Defense Opportunity

Redwire Corp RDW | 9.91 9.83 | +1.02% -0.81% Post |

SHIELD contract opens a new channel of potential work

Redwire (RDW) recently secured a position on the Missile Defense Agency's SHIELD indefinite delivery indefinite quantity contract, a multi company vehicle with a US$151b ceiling and no guaranteed revenue.

Redwire's latest SHIELD contract news comes after a sharp 62.72% 90 day share price return, even though the 1 year total shareholder return is a 52.03% decline and the 3 year total shareholder return remains very large at about 3x. Taken together, these figures suggest sentiment has recently improved from a weak longer term base.

If defense and space exposure is on your radar after this contract win, it could be worth seeing what else is out there through our screener of 33 AI infrastructure stocks as another way to spot potential opportunities in related themes.

So with Redwire sitting about 31% below the US$13.11 average analyst price target after a sharp 90 day rebound, is the recent SHIELD news creating a genuine entry point, or has the market already priced in future growth?

Most Popular Narrative: 24.1% Undervalued

Redwire's most followed narrative pegs fair value at about $13.22 per share versus the $10.04 last close, framing SHIELD as one piece of a bigger long term story.

The rapid proliferation of commercial satellites and upcoming public/private low Earth orbit projects continues to build demand for Redwire's advanced in space manufacturing, deployable structures, and subsystems, supporting multi year visibility on high margin product sales and recurring earnings.

Read the complete narrative. Read the complete narrative.

Want to see what is sitting behind that confidence in multi year demand, margins, and earnings power? The narrative leans heavily on compounding revenue growth, improving profitability, and a richer earnings multiple than many peers. Curious which specific revenue mix shift and margin path are doing most of the heavy lifting in that $13.22 fair value?

Result: Fair Value of $13.22 (UNDERVALUED)

However, there are still real swing factors, such as ongoing government contract delays and cost overruns on complex fixed price projects, that could quickly dent that optimism.

Another View: Multiples Point To A Richer Price

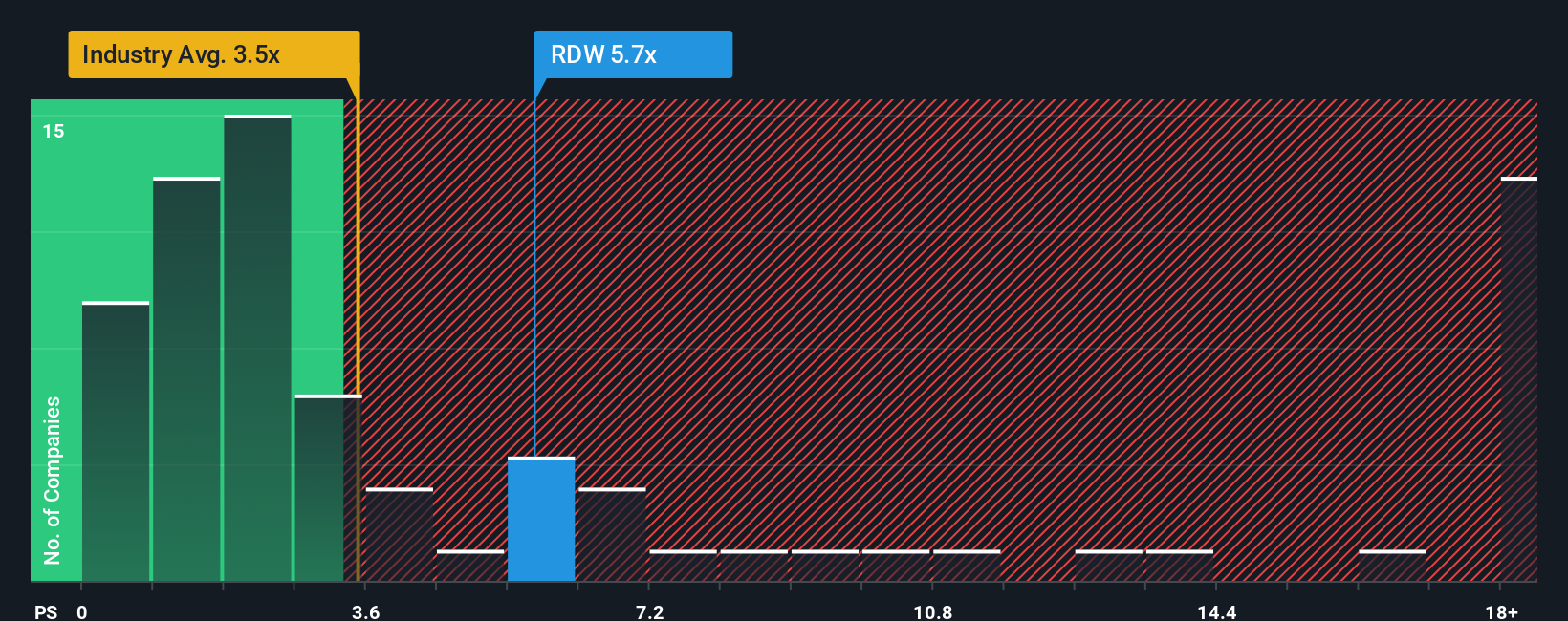

That 24.1% “undervalued” narrative sits awkwardly next to how the market is actually pricing Redwire today. The shares trade on a P/S of 5.6x, compared with a fair ratio of 2.3x, the US Aerospace & Defense average of 3.8x, and a peer average of 2.2x. In plain terms, you are paying a far steeper sales multiple than both the sector and peers, and well above where the fair ratio suggests the stock could move toward, which raises the question of how much execution risk you are really comfortable owning at this price.

Build Your Own Redwire Narrative

If you are not fully on board with these assumptions, or you simply prefer to test your own inputs and judgments, you can spin up a custom Redwire story in just a few minutes and see how your version of fair value stacks up against the crowd, then Do it your way

A great starting point for your Redwire research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about broadening your watchlist beyond a single contract story, using a focused screener can quickly surface new angles you might otherwise miss.

- Spot potential mispricings by scanning our list of 52 high quality undervalued stocks that pair fundamentals with prices that may not fully reflect them.

- Prioritise resilience by checking out 82 resilient stocks with low risk scores, highlighting companies that score well on factors linked to lower overall risk.

- Get ahead of the crowd by reviewing our screener containing 24 high quality undiscovered gems, where smaller names with solid underpinnings may not yet be widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.