Revenue Jump and Portfolio Expansion Could Be a Game Changer for MannKind (MNKD)

MannKind Corporation MNKD | 0.00 |

- MannKind Corporation recently reported third-quarter results showing revenue of US$82.13 million, up from US$70.08 million a year earlier, driven by strong performance in its inhaled insulin products and new contributions following the acquisition of scPharmaceuticals.

- The company's portfolio expansion and regulatory progress, including FDA review milestones for Afrezza and FUROSCIX, highlight MannKind's continuing push into diabetes and rare disease markets.

- We'll assess how MannKind's stronger-than-expected revenue growth and product diversification affect its updated investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

MannKind Investment Narrative Recap

To be a MannKind shareholder, you need to believe in the company’s ability to drive adoption of innovative inhaled therapies like Afrezza, expand its pipeline, and benefit from growing demand in diabetes and rare disease markets. While strong Q3 revenue growth reinforces the story and boosts optimism about new product launches, it does not materially change the fact that broad adult prescriber adoption of Afrezza remains the most important near-term catalyst, while persistent challenges in expanding Afrezza’s market share continue to pose the biggest risk.

The recent FDA acceptance of the supplemental Biologics License Application for pediatric use of Afrezza stands out as a potentially meaningful catalyst, as regulatory progress could unlock access to new patient populations and accelerate adoption. This announcement’s significance ties directly to MannKind’s narrative of expanding revenue sources and diversifying away from a concentrated product portfolio.

In contrast, investors should be aware of ongoing concerns around prescriber hesitancy toward Afrezza and how...

MannKind's narrative projects $437.5 million in revenue and $70.4 million in earnings by 2028. This requires 13.2% yearly revenue growth and a $37.6 million increase in earnings from the current $32.8 million.

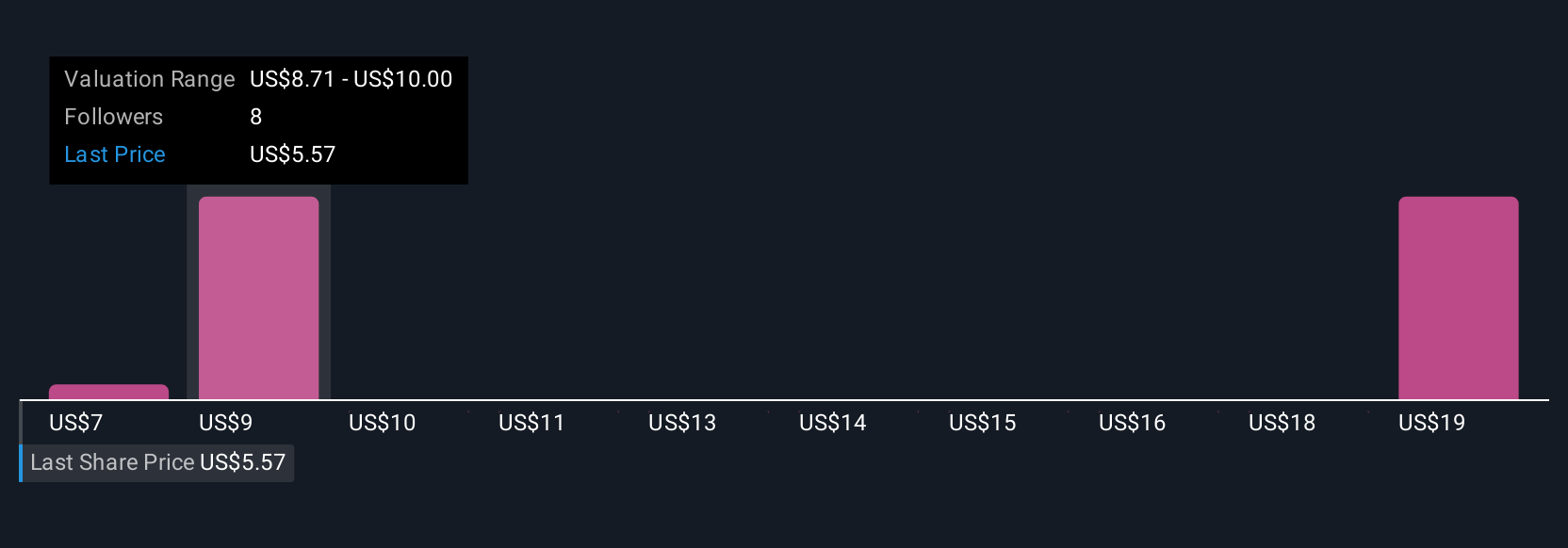

Uncover how MannKind's forecasts yield a $10.57 fair value, a 85% upside to its current price.

Exploring Other Perspectives

Fair value estimates from four Simply Wall St Community members for MannKind range from US$2.62 to US$10.57 per share. Amid such varied outlooks, the company’s reliance on Afrezza’s market penetration remains a critical focal point for future performance and warrants close attention to different viewpoints.

Explore 4 other fair value estimates on MannKind - why the stock might be worth less than half the current price!

Build Your Own MannKind Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your MannKind research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free MannKind research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MannKind's overall financial health at a glance.

No Opportunity In MannKind?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.