Revolution Medicines (RVMD) Stock After RASolute 302 Phase 3 Success A Fresh Look At Valuation

Revolution Medicines RVMD | 0.00 |

Revolution Medicines (RVMD) is back in focus after detailed Phase 3 RASolute 302 data showed daraxonrasib delivered unprecedented overall and progression-free survival outcomes versus standard chemotherapy in previously treated metastatic pancreatic ductal adenocarcinoma.

Those Phase 3 headlines arrive after a powerful run in the stock, with a 90 day share price return of 62.21% and a year to date share price return of 94.72%. The 3 year total shareholder return above 5x signals how strongly expectations around Revolution Medicines’ pipeline have shifted.

If breakthrough oncology data is on your radar, this could be a useful moment to broaden your watchlist with a curated set of 40 healthcare AI stocks

After a near 95% year-to-date share price move and a market value above US$31b, traders have clearly reacted to the Phase 3 win. But is Revolution Medicines still mispriced, or is the market already baking in years of future growth?

Most Popular Narrative: 15.1% Overvalued

The most followed valuation narrative pegs Revolution Medicines' fair value at $133.70, which sits below the latest close at $153.87 and frames the recent surge in a different light.

The move toward targeted oncology treatments for high unmet need tumors such as pancreatic, lung and colorectal cancer aligns with the company’s RAS(ON) portfolio, which could influence long term revenue growth if multiple registrational programs convert to approved therapies.

Curious what kind of revenue curve and margin profile it takes to back that fair value, and why the implied future earnings multiple is so demanding? The most followed narrative lays out a detailed path using analyst forecasts, future profitability assumptions and a discount rate that together explain how it lands at $133.70.

Result: Fair Value of $133.70 (OVERVALUED)

However, the heavy cash burn from US$1.6b to US$1.7b in planned 2026 expenses, along with the concentrated RAS pipeline, could quickly challenge this overvaluation story.

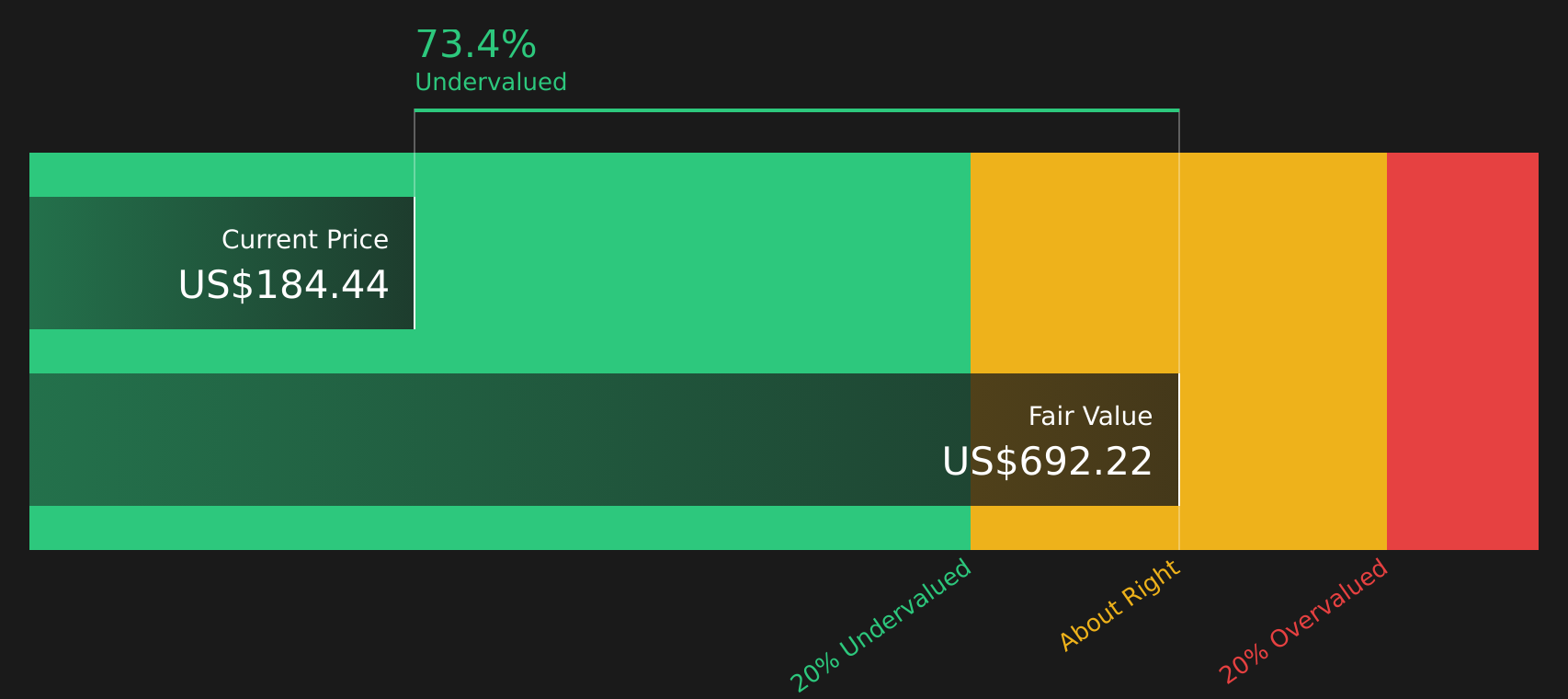

Another View: DCF Flips the Story

While the most followed narrative sees Revolution Medicines as 15.1% overvalued at $153.87 versus a $133.70 fair value, the SWS DCF model points the other way. On this view, the stock trades at a very large 74.7% discount to an estimated $608.69 future cash flow value. Which set of assumptions do you find more realistic?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Revolution Medicines for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With the article pointing to both excitement and concern around Revolution Medicines, this is a good moment to act quickly. Pressure test the story against the underlying data using 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Revolution Medicines is on your radar, do not stop there. Broaden your opportunity set now so you are not relying on a single story.

- Target potential mispricings by scanning a curated pool of 44 high quality undervalued stocks that combine quality fundamentals with room for sentiment to catch up.

- Strengthen your defensive side by focusing on solid balance sheet and fundamentals stocks screener (48 results) that can better handle pressure when conditions get tougher.

- Get ahead of the crowd by hunting through a screener containing 20 high quality undiscovered gems before wider attention starts to close the gap between price and fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.