Ridgepost Capital (RPC) Earnings Margin Holds At 5.1% And Tests Bullish Narratives

Ridgepost Capital, Inc. Class A RPC | 0.00 |

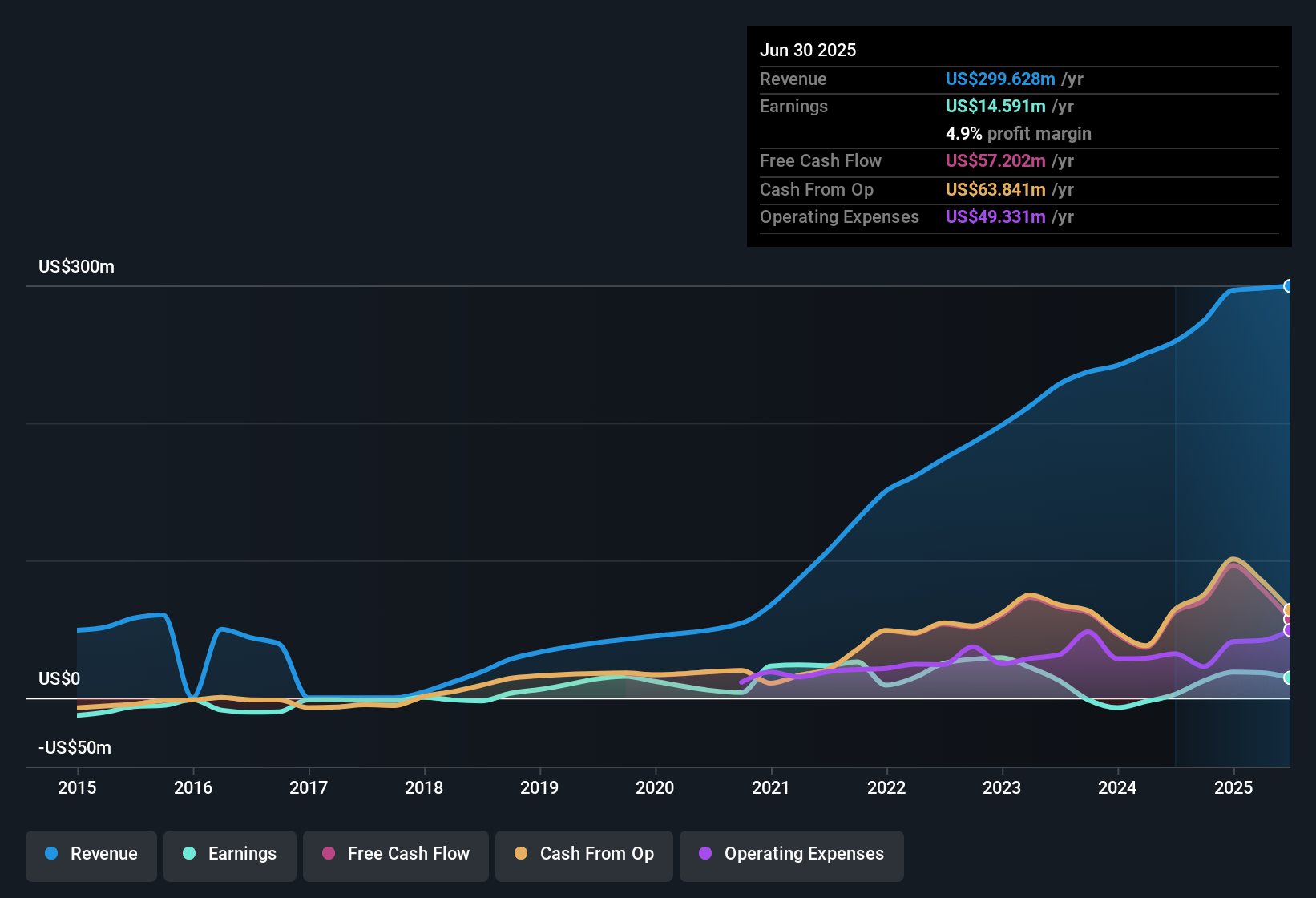

Ridgepost Capital (RPC) has just posted its FY 2025 numbers with Q3 total revenue at US$75.9 million and basic EPS of US$0.02, while trailing twelve month revenue stands at US$301.3 million and EPS at US$0.14, as investors weigh these against a mixed earnings backdrop affected by a one off US$33.1 million loss. Over recent quarters, revenue has moved from US$71.1 million in Q2 2024 to US$75.9 million in Q3 2025, while quarterly EPS shifted from US$0.06 to US$0.02. This sets the stage for a debate around how a 5.1% net margin and a 24.3% earnings lift over the past year fit with longer term earnings pressure. With that context, the latest print puts the focus squarely on how durable Ridgepost Capital’s margins really are.

See our full analysis for Ridgepost Capital.With the headline numbers on the table, the next step is to see how this earnings profile lines up with the widely followed narratives around Ridgepost Capital’s growth potential, risk profile, and profit quality, and where those stories might need to be updated.

5.1% net margin with earnings still under pressure

- Over the last 12 months, Ridgepost Capital recorded US$301.3 million in revenue and US$15.3 million in net income, which works out to a 5.1% net margin that sits alongside an 18.7% per year earnings decline over five years.

- Analysts' consensus view that earnings can improve over time meets a mixed record here, as:

- Recent earnings rose 24.3% over the past year and margin moved from 4.5% to 5.1%, yet the longer term trend still shows that 18.7% annual earnings decline over five years.

- A one off US$33.1 million loss has also had a large impact on the trailing 12 month figures, so headline profitability and any implied margin progress are partly shaped by that event.

AUM growth contrasts with softer quarterly profit

- Assets under management moved from US$25.7b at the start of Q1 2025 to US$29.1b at the end of Q3 2025, while quarterly net income excluding extra items over those same three quarters ranged between US$2.1 million and US$4.5 million on US$67.7 million to US$75.9 million of revenue.

- Consensus narrative often leans bullish on AUM as a driver, and this lines up with the numbers but also faces a tension:

- AUM grew alongside net inflows of US$1.4b in Q1, US$1.9b in Q2 and US$915 million in Q3, which fits the idea that fee earning assets are building.

- At the same time, basic EPS stepped down from US$0.04 in Q1 to just under US$0.02 in Q3, so the recent profit per share trend does not yet match the AUM expansion.

61x P/E and dividend coverage concerns

- Ridgepost Capital trades on a 61x P/E, compared with 22.9x for the US Capital Markets industry and 7.9x for peers, while paying a 1.76% dividend yield that is flagged as weakly covered by earnings and backed by operating cash flow that does not comfortably cover debt.

- Critics highlight these valuation and balance sheet pressure points as a bearish angle, and the data gives them several talking points:

- The 61x P/E is almost 3x the broader industry multiple and far above the 7.9x peer average, even though multi year earnings have fallen by 18.7% per year.

- With dividend coverage described as weak and debt not well covered by operating cash flow, income focused investors have to weigh that 1.76% yield against the cash generation strain that the risk summary points out.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Ridgepost Capital on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a couple of minutes to test your own view against the data and turn it into a clear, shareable story: Do it your way

A great starting point for your Ridgepost Capital research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

See What Else Is Out There

Ridgepost Capital is wrestling with a 61x P/E, five year earnings pressure and weak dividend coverage, while cash flow does not comfortably cover debt.

If those red flags worry you, take a moment to compare them with companies in our solid balance sheet and fundamentals stocks screener (45 results) that focus on stronger coverage and sturdier fundamentals right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.