Rising Unhedged Fuel Costs Could Be A Game Changer For Carnival Corporation & (CCL)

Carnival Corporation CCL | 0.00 |

- Carnival Corporation & plc recently highlighted strong post-pandemic performance, record adjusted net income in fiscal 2025, and renewed capital discipline, even as the broader cruise industry confronts sharply higher fuel costs from a more than very large jump in oil prices linked to conflict in Iran.

- However, Carnival’s decision not to hedge fuel prices leaves it more exposed than hedged peers to rising bunker costs, amplifying investor focus on how efficiency improvements, itinerary changes such as the cancelled Carnival Firenze Baja sailings, and private-destination investments will influence future profitability.

- We’ll now examine how Carnival’s heightened exposure to unhedged fuel costs could reshape its investment narrative and outlook on earnings quality.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 22 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Carnival Corporation & Investment Narrative Recap

To own Carnival today, you need to believe its post-pandemic earnings power and demand recovery can more than offset rising fuel costs and a still-heavy debt load. The key short term catalyst is the upcoming Q1 2026 earnings and guidance on yields and costs, while unhedged exposure to sharply higher bunker fuel remains the single biggest near term risk. The latest headlines on oil and Iran are material because they cut straight into that margin story.

Among recent developments, Carnival’s reinstated quarterly dividend of US$0.15 per share stands out because it signals confidence in cash generation even as fuel costs spike. How management balances ongoing deleveraging, higher interest costs, and elevated fuel expense with returning cash to shareholders will be central to how the market reacts to Q1 results and any update on capital allocation priorities.

Yet behind the strong recovery story, investors should also be aware that rising oil, unhedged fuel exposure, and a high debt load could...

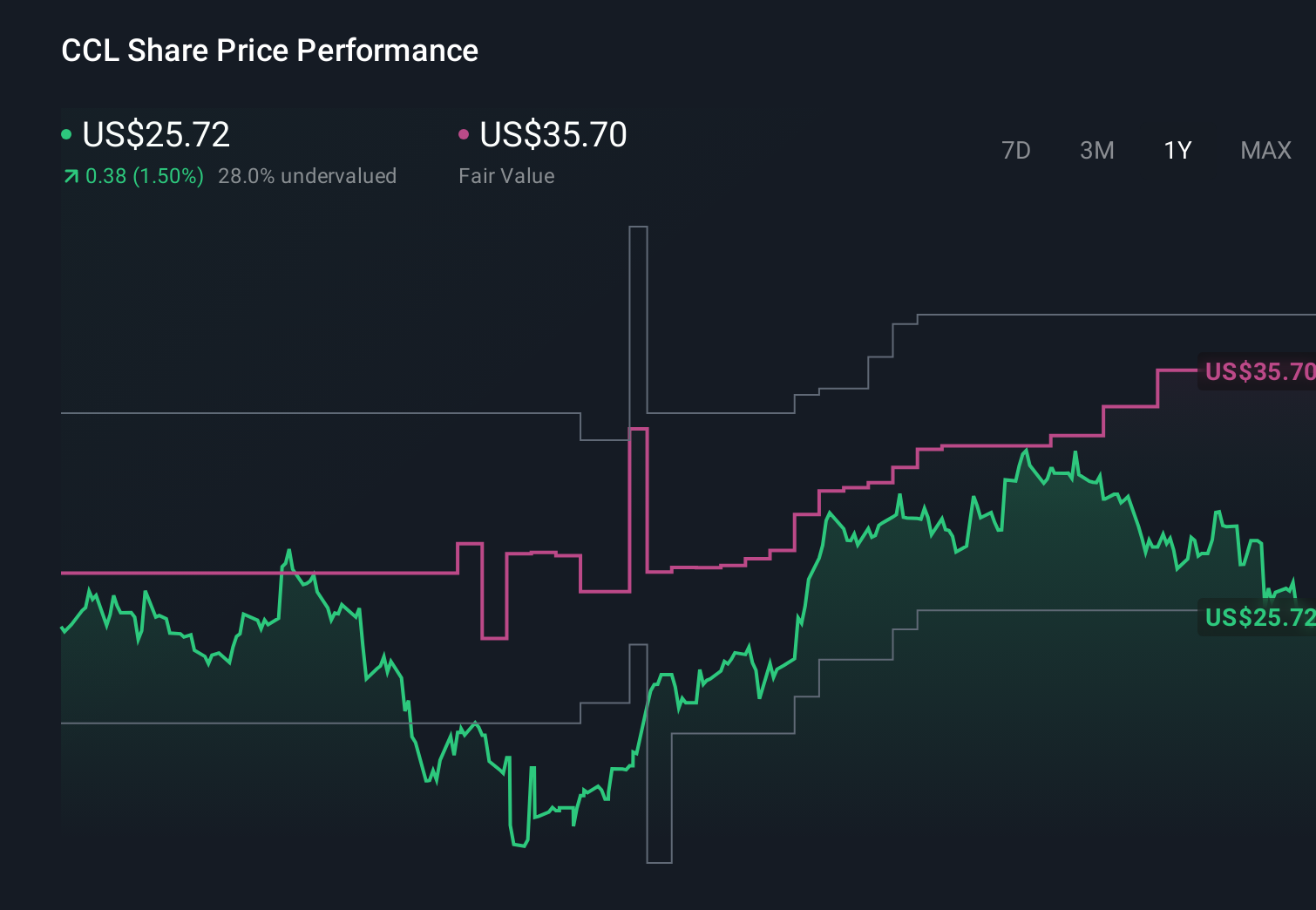

Carnival Corporation &'s narrative projects $29.0 billion revenue and $3.7 billion earnings by 2028. This requires 3.8% yearly revenue growth and about a $1.2 billion earnings increase from $2.5 billion today.

Uncover how Carnival Corporation &'s forecasts yield a $37.70 fair value, a 50% upside to its current price.

Exploring Other Perspectives

Before the oil shock, the most optimistic analysts were penciling in about US$30 billion of revenue and US$4.3 billion of earnings by 2028, but if fuel and geopolitical risks persist, those upbeat margin and deleveraging assumptions could prove far more fragile than they looked on paper.

Explore 12 other fair value estimates on Carnival Corporation & - why the stock might be worth as much as 94% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carnival Corporation & research is our analysis highlighting 5 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Carnival Corporation & research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carnival Corporation &'s overall financial health at a glance.

No Opportunity In Carnival Corporation &?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.