Rithm Property Trust (RPT) Q3 Revenue Of US$3.6 Million Tests Bullish Growth Narratives

Rithm Property Trust Inc. RPT | 14.48 14.48 | +2.77% 0.00% Post |

Rithm Property Trust (RPT) has put out its latest FY 2025 numbers with third quarter total revenue of US$3.6 million and basic EPS of a US$0.21 loss, following second quarter revenue of US$4.7 million with EPS of US$0.08. Over recent quarters, the company has seen revenue move from US$5.4 million in Q4 2024 to a US$0.9 million loss in Q1 2025, alongside EPS shifting from US$0.35 to a US$0.49 loss. This leaves investors weighing how much of the current earnings profile reflects temporary margin pressure versus a more persistent squeeze on profitability.

See our full analysis for Rithm Property Trust.With the headline figures on the table, the next step is to line these results up against the most common narratives around Rithm Property Trust to see which stories the numbers actually support and which ones start to look stretched.

Losses ease, but trailing 12 month net loss still US$2.1 million

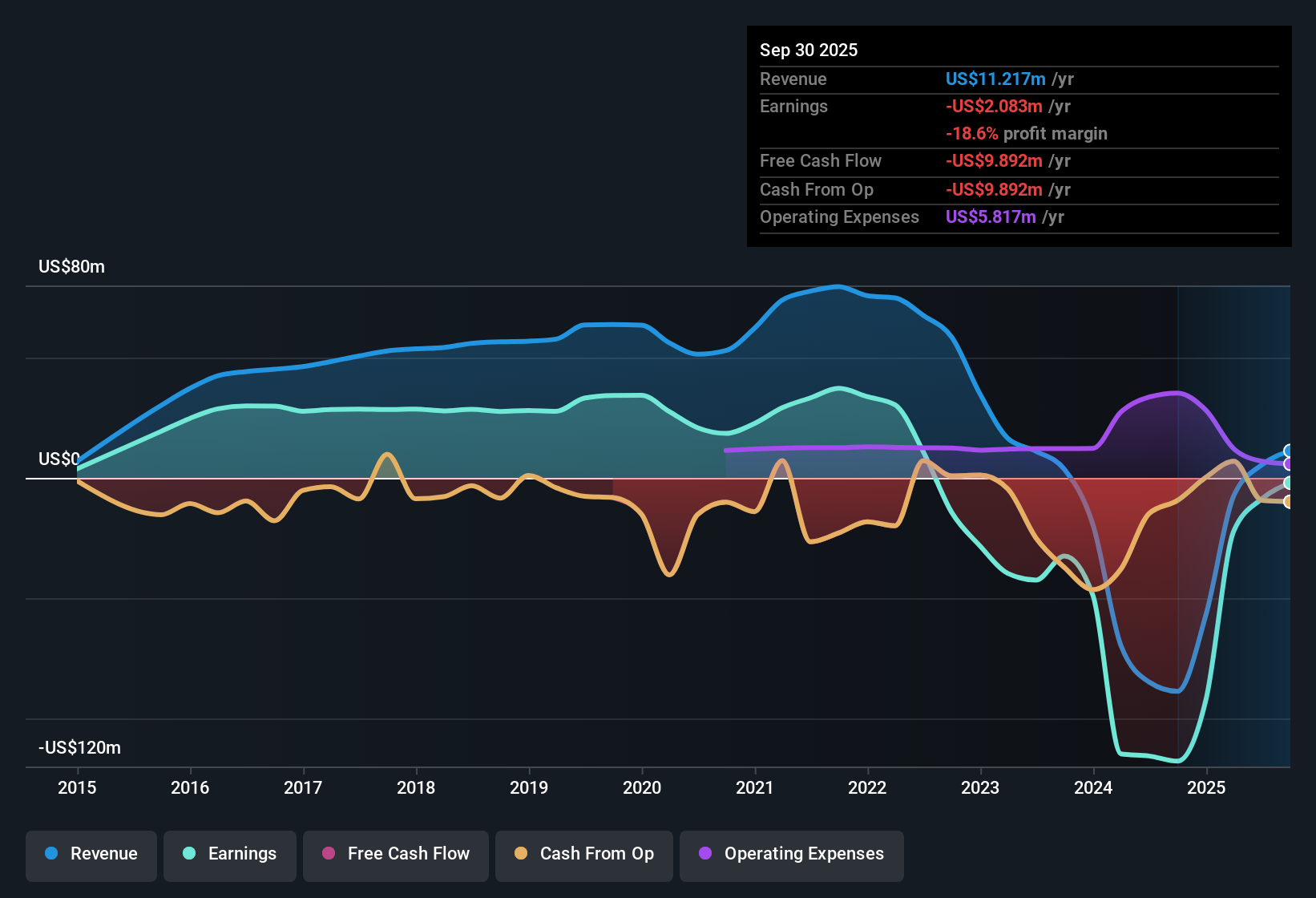

- On a trailing 12 month basis to Q3 2025, Rithm Property Trust reported total revenue of US$11.2 million and a net loss of US$2.1 million, with trailing basic EPS at a loss of US$0.28.

- Bulls argue that a clean balance sheet and roughly US$300 million of equity give plenty of room to grow earnings. However, the current trailing loss of US$2.1 million and quarterly net loss of US$1.6 million in Q3 2025 show that the higher yielding loans they are targeting have not yet turned into sustained profits.

- The bullish narrative points to potential earnings of US$31.6 million by 2029, but that sits in sharp contrast to the latest 12 month loss and the data showing the company is still unprofitable today.

- Supporters highlight expected revenue growth and margin expansion, while the FY 2025 numbers so far show revenue of US$3.6 million in Q3 and US$4.7 million in Q2 with only one of those quarters producing positive net income.

High 9.79% yield, but payouts not backed by earnings

- The stock currently offers a 9.79% dividend yield, yet over the last 12 months that dividend has not been covered by reported earnings or free cash flow, which have both been negative.

- Bears focus on this gap between payout and profits, arguing that unprofitable trailing 12 month results and losses that have grown at an annualized rate of 52.7% over five years make the current yield look fragile.

- The trailing 12 month net loss of US$2.1 million and negative operating cash flow coverage of debt directly feed into those concerns about how comfortably the dividend can be maintained.

- Even with some profitable quarters like Q4 2024 net income of US$2.6 million, the overall trailing pattern of losses is what bears point to when they question dividend sustainability.

P/S at 9.9x while company remains unprofitable

- Rithm Property Trust trades on a P/S multiple of 9.9x, compared with about 5x for the US Mortgage REITs industry and 6.4x for peers, even though it is loss making on a trailing 12 month basis.

- Consensus narrative talks about strong commercial real estate pipelines and analysts looking for earnings of US$23.1 million by 2028. However, the current combination of elevated P/S and trailing losses means today’s valuation is being set against results that still show US$2.1 million of losses and no identified upside rewards in the risk and reward dataset.

- Analysts’ collective target of US$61.99 sits above the current share price of US$14.71, which assumes future revenue of US$83.7 million and profit margins turning positive, a very different picture to today’s modest US$11.2 million of trailing revenue.

- Critics highlight that operating cash flow does not currently cover debt and that the company is unprofitable, so any case for that gap between US$14.71 and US$61.99 relies heavily on the improvement path analysts are modeling rather than the latest reported numbers.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Rithm Property Trust on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers pointing in a different direction? Take a couple of minutes to turn that view into your own clear narrative. Start with Do it your way.

A great starting point for your Rithm Property Trust research is our analysis highlighting 3 important warning signs that could impact your investment decision.

See What Else Is Out There

Rithm Property Trust is still loss making, with dividends not covered by earnings or cash flow, and a relatively high P/S multiple despite trailing losses.

If that mix of fragile payouts and ongoing losses feels uncomfortable, take a few minutes to size up income ideas in 13 dividend fortresses that have more robust support.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.