Rivian Automotive (RIVN) Could Be 53% Below Fair Value After Raised 2026 Guidance

Rivian Automotive RIVN | 0.00 |

Why Rivian’s raised 2026 guidance matters for shareholders

Rivian Automotive (RIVN) raised its full year 2026 delivery guidance to 65,000 to 70,000 vehicles after second quarter production and deliveries came in above its earlier outlook.

For you as a shareholder or potential investor, this updated guidance ties directly to how confidently the company currently sees demand and its ability to keep production running at the Normal, Illinois facility while it ramps the new R2 SUV.

Rivian’s raised guidance landed alongside a strong recent share price move, with an 8.44% 1 day and 25.37% 7 day share price return. However, the year to date share price return is still down 4.02% while the 1 year total shareholder return is 42.54%, which points to momentum rebuilding after a weaker patch.

If the latest delivery beat has you looking beyond Rivian for other EV related ideas, it could be a useful time to scan 52 AI infrastructure stocks. These are the companies building the hardware backbone behind connected and autonomous vehicles.

With Rivian shares up strongly in the past week and trading close to the average analyst price target, the key question now is whether the stock still trades at a discount or if the market is already pricing in future growth.

Most Popular Narrative: 2.6% Overvalued

Rivian Automotive last closed at $18.63, slightly above the most followed narrative fair value estimate of $18.15, which frames how some analysts see the risk and reward trade off today.

The launch of the R2 platform represents a step-change improvement in Rivian's cost structure, with management securing supplier contracts and component sourcing that reduce bill of materials by nearly 50% versus R1, significantly lowering per-unit costs; this operational overhaul is expected to improve gross margins and path to profitability as scale is achieved.

Curious what has to happen for that fair value to hold up? The narrative leans heavily on rapid revenue expansion, improving margins and a future earnings multiple more often seen in growth heavy sectors.

These expectations are built using a 10.86% discount rate, which reflects how the narrative weighs Rivian's potential future cash flows against execution risk in a still unprofitable business.

Analysts contributing to this view see a path where higher deliveries, software and services revenue, and manufacturing efficiencies gradually change today’s loss making profile, even if profitability is not forecast within the next three years.

At the same time, the narrative acknowledges that this path is exposed to policy changes, sector wide pricing pressure and ongoing cash needs, all of which could affect how quickly Rivian Automotive can move toward the earnings power implied in that fair value.

Result: Fair Value of $18.15 (OVERVALUED)

However, this narrative could still be knocked off course if high cash burn forces fresh equity raises or if R2 demand falls short of expectations.

Another View on Rivian Automotive’s Valuation

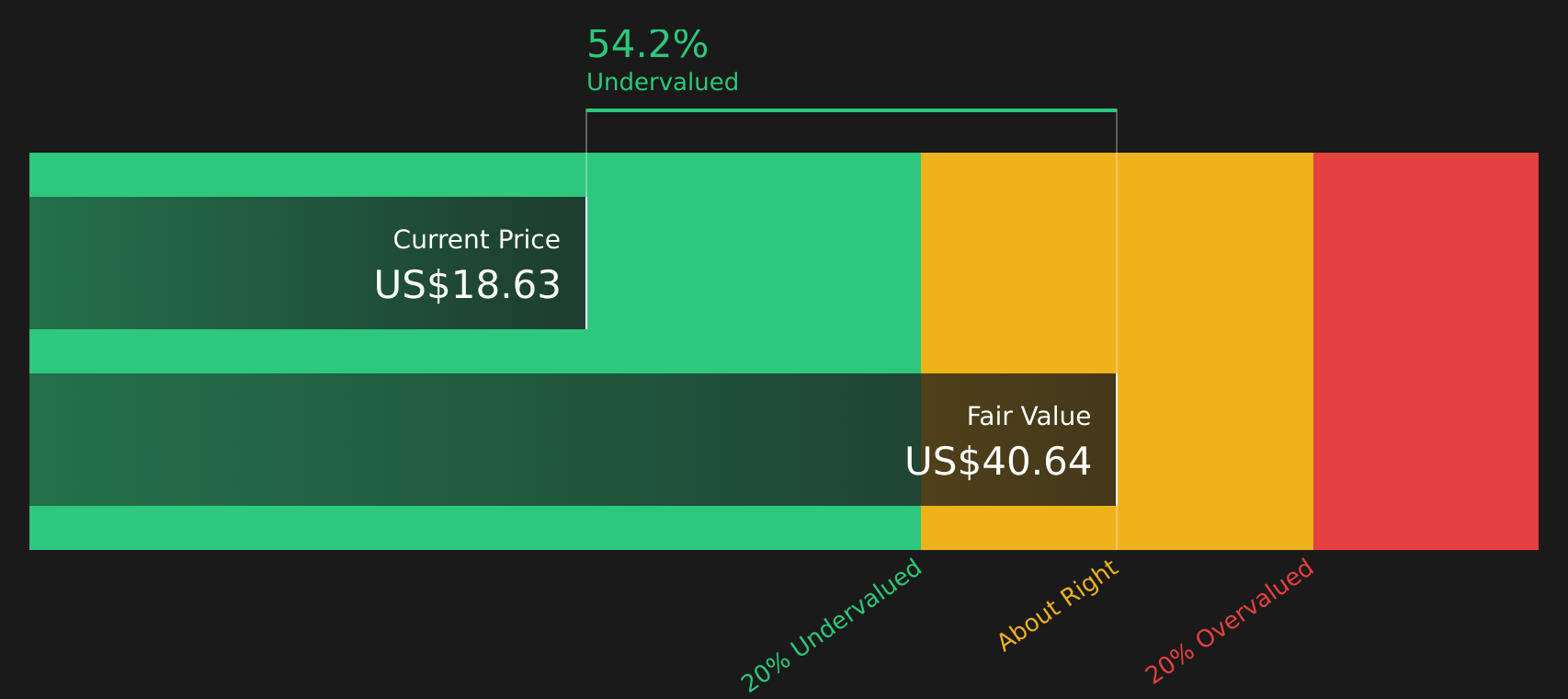

The analyst narrative frames Rivian Automotive as about 2.6% overvalued at $18.63 versus a fair value of $18.15, yet the SWS DCF model points in a different direction, with the stock trading at a 52.7% discount to an estimated future cash flow value of $39.42. Which lens do you trust more when real cash flows are still in the distance?

For a closer look at how those projected cash flows translate into that gap between $18.63 and $39.42, it can help to walk through the underlying assumptions in the Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Rivian Automotive for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across Rivian Automotive’s valuation and outlook, how confident are you in the balance of risks and rewards, and how quickly do you want to form your own view by reviewing the 2 key rewards and 1 important warning sign?

Looking for more investment ideas beyond Rivian Automotive?

Do not stop at Rivian if you want a fuller picture of opportunities. Use the Simply Wall St screener to surface other stocks that fit your approach.

- Target income potential by reviewing companies that qualify as 7 dividend fortresses for investors who want yield with a focus on resilience.

- Hunt for quality at a discount by scanning the screener containing 18 high quality undiscovered gems before others catch on and valuations adjust.

- Prioritise capital preservation by focusing on companies in the 75 resilient stocks with low risk scores that score well on financial strength and risk controls.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.