Rivian (RIVN) Stock After Recent Volatility Is The Current Price Attractive

Rivian Automotive RIVN | 0.00 |

- For investors considering whether Rivian Automotive at around US$15.54 is priced for a potential comeback or still reflects excessive hype, this article focuses on what the current share price might be implying about value.

- The stock has been volatile recently, with the share price down about 14.2% over the past week, up 11.4% over the last 30 days and delivering 11.7% over the past year. Year to date it is down 19.9%, and over three years it is up 2.0%.

- Recent coverage of Rivian has focused on its position in the electric vehicle space, its access to capital markets and the pace at which it is scaling production capacity. Together, these themes help explain why the market has been quick to reassess both the risk around the business and the price it is willing to pay for the stock.

- Simply Wall St currently assigns Rivian a valuation score of 2 out of 6. The rest of this article breaks down what different valuation methods are indicating about the stock and finishes with a broader framework that can help you think about value beyond just the numbers.

Rivian Automotive scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

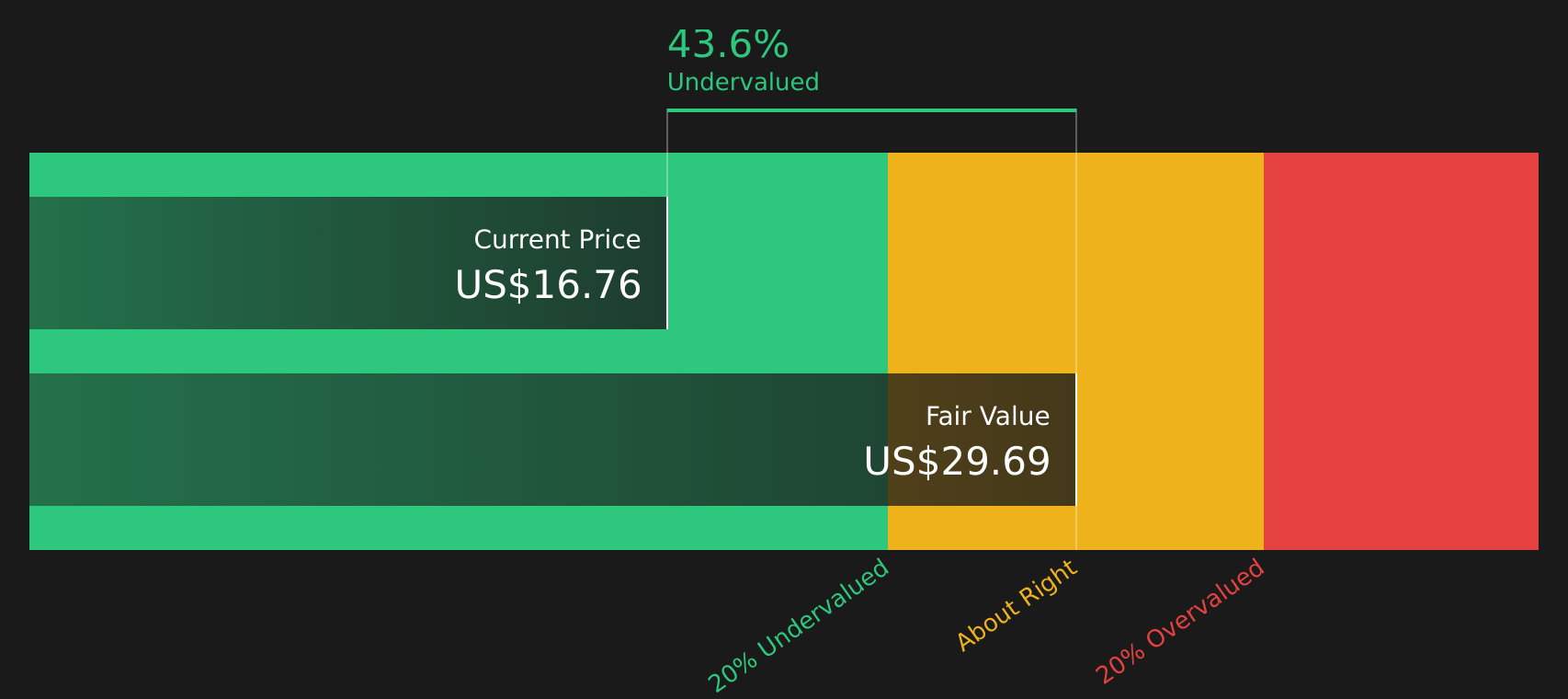

Approach 1: Rivian Automotive Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of a company’s future cash flows and discounts them back to today using a required rate of return, aiming to translate long term cash generation into a single present value per share.

For Rivian Automotive, the latest twelve month free cash flow shows a loss of about $2.71b. Analysts and extrapolated estimates point to free cash flow staying negative for several years, then moving into positive territory, reaching a projected $1.54b by 2030. Simply Wall St uses a 2 Stage Free Cash Flow to Equity model, which combines these yearly projections, including extrapolated figures out to 2035, and discounts each of them back to today.

On this basis, the model arrives at an estimated intrinsic value of about $29.44 per share for Rivian Automotive. Compared with the current share price of around $15.54, the DCF output implies the stock is 47.2% undervalued according to these assumptions and projections.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Rivian Automotive is undervalued by 47.2%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

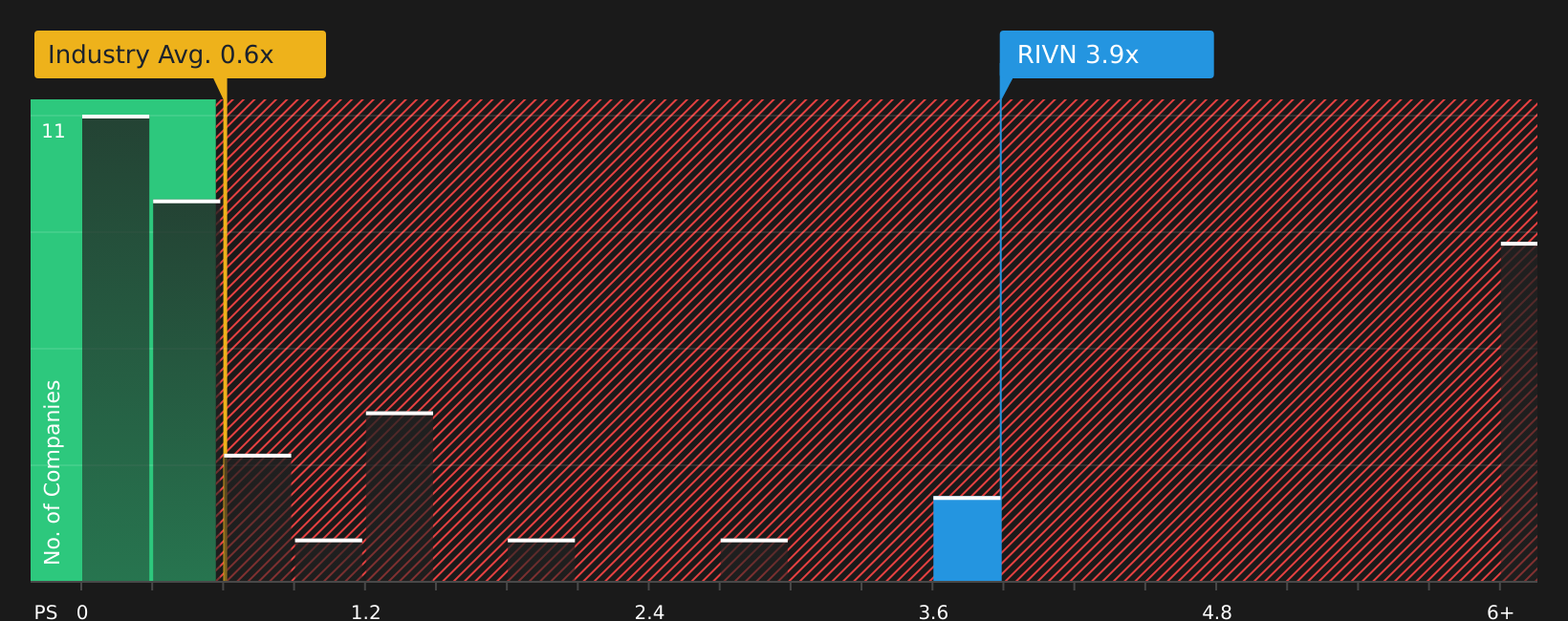

Approach 2: Rivian Automotive Price vs Sales

For companies that are not yet consistently profitable, the P/S ratio is often more useful than P/E because it compares the value of the stock to current revenue rather than earnings that may still be in a loss position.

In general, higher growth expectations and lower perceived risk can justify a higher normal or fair P/S multiple. Slower expected growth or higher risk usually align with a lower multiple. What you are really asking is how much investors are willing to pay for each dollar of sales given those trade offs.

Rivian Automotive currently trades on a P/S of 3.60x, compared with the Auto industry average of about 0.61x and a peer average of 0.83x. Simply Wall St also calculates a Fair Ratio of 1.87x for Rivian, which is the P/S level suggested by factors such as earnings growth estimates, industry, profit margin, market cap and risks.

This Fair Ratio is more tailored than a simple peer or industry comparison because it adjusts for Rivian’s specific growth profile and risk characteristics rather than assuming all Auto stocks deserve similar multiples. With the current 3.60x P/S sitting well above the 1.87x Fair Ratio, the multiple points to the stock trading on a richer valuation than those inputs would suggest.

Result: OVERVALUED

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Upgrade Your Decision Making: Choose your Rivian Automotive Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so Narratives are introduced here as simple stories that capture your view on Rivian Automotive’s future revenue, earnings and margins, link that story to a forecast and a Fair Value per share, and then compare that Fair Value with the current price, all within an easy tool on Simply Wall St’s Community page that updates automatically when fresh news or earnings arrive.

In practice, this means one investor might build a Rivian Narrative closer to the bullish Fair Value of about US$25.00 per share, assuming faster growth and stronger margins. Another might sit near the more cautious Fair Value of roughly US$9.42 per share. By setting up and following these different Narratives side by side, you can quickly see how your own view compares with the wider community and use that as one more input when deciding whether the current price around US$15.54 feels high, low, or roughly in line with the story you believe is realistic.

For Rivian Automotive, here are previews of two leading Rivian Automotive Narratives:

Fair value in this bullish narrative: US$18.15 per share

Implied discount to that fair value at the recent US$15.54 price: about 14.4% undervalued

Revenue growth assumption: 51.29% a year

- This narrative leans on the R2 platform and manufacturing efficiency to lower unit costs, improve gross margins and support a clearer route toward profitability.

- It expects technology integration and partnerships, including software and commercial deals, to add higher margin revenue streams on top of vehicle sales.

- It still flags policy shifts, supply chain pressures and competitive intensity as key risks that could disrupt the path to those outcomes.

Fair value in this bearish narrative: US$9.42 per share

Implied premium to that fair value at the recent US$15.54 price: about 64.9% overvalued

Revenue growth assumption: 33.85% a year

- This narrative focuses on shrinking policy support, higher costs and softer demand as pressures on Rivian's margins, cash flow and ability to support large spending plans.

- It highlights competition, higher tariffs and macro headwinds as factors that could keep losses elevated and increase the likelihood of further funding needs.

- Even while acknowledging potential benefits from R2 and software, it assumes these will not be enough to offset cash burn and execution risk at the current share price.

Put together, these Narratives show how two sets of reasonable assumptions can lead to very different fair values. This is why it helps to decide where your own expectations for revenue growth, margins and funding needs sit between them before taking a view on the stock at around US$15.54.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Rivian Automotive on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Do you think there's more to the story for Rivian Automotive? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.