RLI (RLI) Valuation Check After Recent Share Price Weakness And 10.7% Undervalued Narrative

RLI Corp. RLI | 0.00 |

RLI stock performance sets the stage

RLI (RLI) has been under pressure recently, with the share price showing a negative move over the past week, month and past 3 months, and a weaker 1 year total return.

The recent 1 day share price return of 1.21% comes after a series of weaker moves, with a 30 day share price return of 9.24% and a 1 year total shareholder return of 26.30% that may indicate fading momentum from earlier gains.

If you are reassessing your insurance exposure, it can also be useful to widen the search and review 18 top founder-led companies

With RLI trading around US$51.77, modestly below some value estimates and analyst targets, the recent 1 year total return of 26.30% raises an important question: is there still upside on the table, or is the market already pricing in future growth?

Most Popular Narrative: 10.7% Undervalued

RLI's most followed narrative tags fair value at $58, compared with the last close of $51.77, framing the recent weakness as a discount to that estimate.

The softening of the commercial property insurance market, driven by increased competition from MGAs and admitted carriers as well as significant new entrants, is expected to suppress top-line premium growth and potentially erode underwriting margins if RLI is unable to maintain current pricing discipline, ultimately pressuring revenue and net margins.

Want to see what sits behind that fair value call? The narrative focuses on changing revenue expectations, slimmer margins, and a higher earnings multiple that needs to hold.

Result: Fair Value of $58 (UNDERVALUED)

However, there is still a risk that higher catastrophe exposure, along with rising acquisition and reinsurance costs, could pressure margins and challenge that 10.7% undervalued narrative.

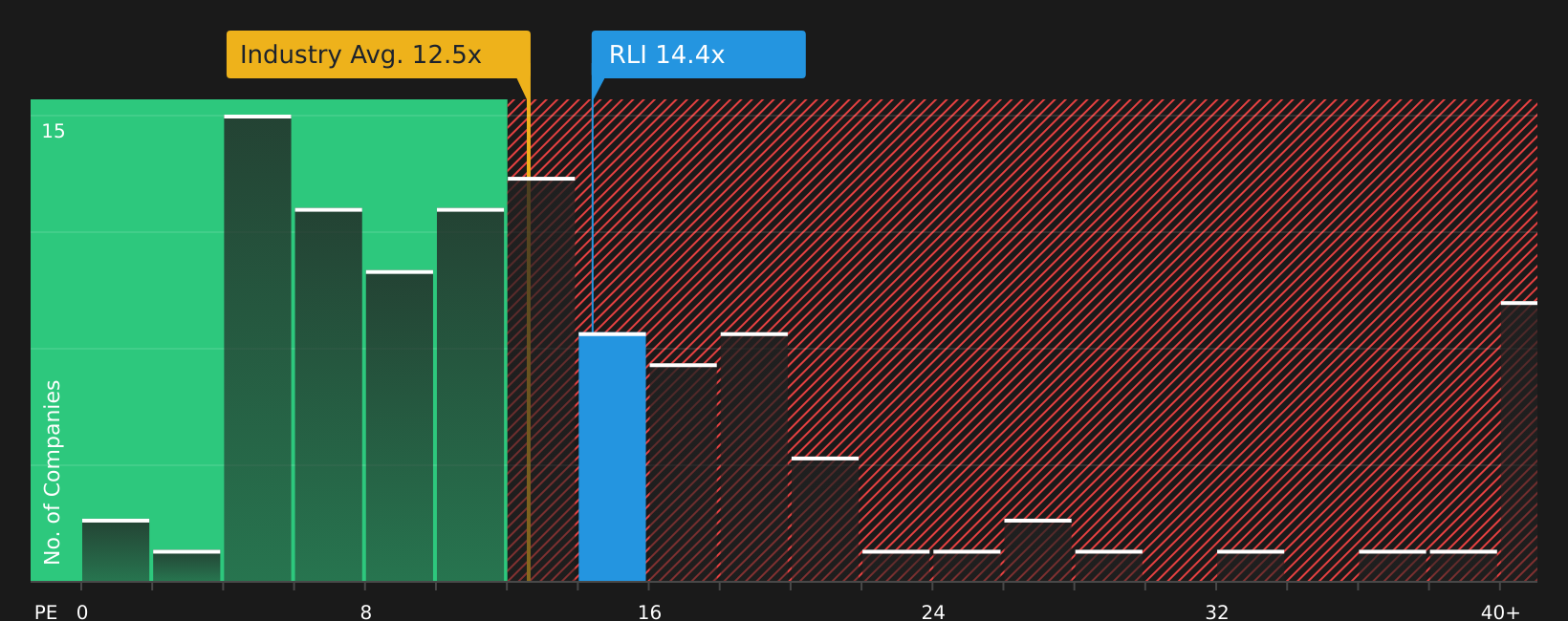

Another way to look at RLI’s valuation

The fair value work above leans on cash flows and analyst forecasts, but the current P/E of 12x tells a different story. That is slightly above the US Insurance industry at 11.7x, above peers at 10.3x, and well above the fair ratio estimate of 8.8x. This points to valuation risk if sentiment cools.

For readers, the question is whether the quality signals at RLI justify paying more than both peers and that fair ratio, or whether patience around the entry price makes more sense.

Next Steps

Mixed messages in the data so far? For a clearer view, review the full picture of risks and rewards for yourself with 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If RLI has you thinking more broadly about your portfolio, now is a good time to scan for other opportunities that fit the kind of profile you want.

- Strengthen your core holdings by reviewing solid balance sheet and fundamentals stocks screener (44 results) that can add financial resilience to your portfolio.

- Hunt for quality at a sensible price with 51 high quality undervalued stocks that could offer more compelling entry points.

- Target reliable cash flow by checking out 12 dividend fortresses that might support a steadier income stream.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.