Robert Half (RHI) Stock Could Be 46% Below Fair Value After Macro Relief Boosted Shares

Robert Half Inc. RHI | 0.00 |

Robert Half (RHI) stock recently moved after investors responded to easing geopolitical risks and softer rate hike expectations, which together support client budgets for staffing and consulting services across its global talent and consulting platform.

Recent macro news, including the prospect of a US Iran peace deal and softer rate expectations, has coincided with a sharp 30 day share price return of 28.74% and a 90 day share price return of 42.22%. However, the 1 year total shareholder return has fallen 16.63% and the 5 year total shareholder return has declined 55.52%, which suggests short term momentum is improving against a weaker long term record.

If the recent move in Robert Half has you thinking about other opportunities tied to workforce and technology trends, it could be a good moment to scan 61 profitable AI stocks that aren't just burning cash

With Robert Half shares up sharply over the past quarter, yet still carrying a weaker multi year record and an implied 46% intrinsic discount, the question is simple: is this a fresh opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 20% Undervalued

At a last close of $32.34 versus a narrative fair value of $32.39, Robert Half stock is effectively aligned with that model, even though the broader Simply Wall St estimate still implies a sizeable intrinsic discount.

Recent research on Robert Half shows a split view, with some analysts lifting targets and others pulling back after the company disclosed a US$17 million cost action charge in its latest 10 K. Here is how the debate is shaping up for you as an investor watching execution and valuation risk.

Want to see what sits underneath that fair value for Robert Half, including the revenue path, margin reset, and lower future earnings multiple that still backs the story?

Result: Fair Value of $32.39 (UNDERVALUED)

However, the Robert Half narrative still faces pressure from revenue declines in key Talent Solutions lines, as well as higher SG&A ratios that squeeze margins and earnings progress.

Another View on Robert Half Stock Valuation

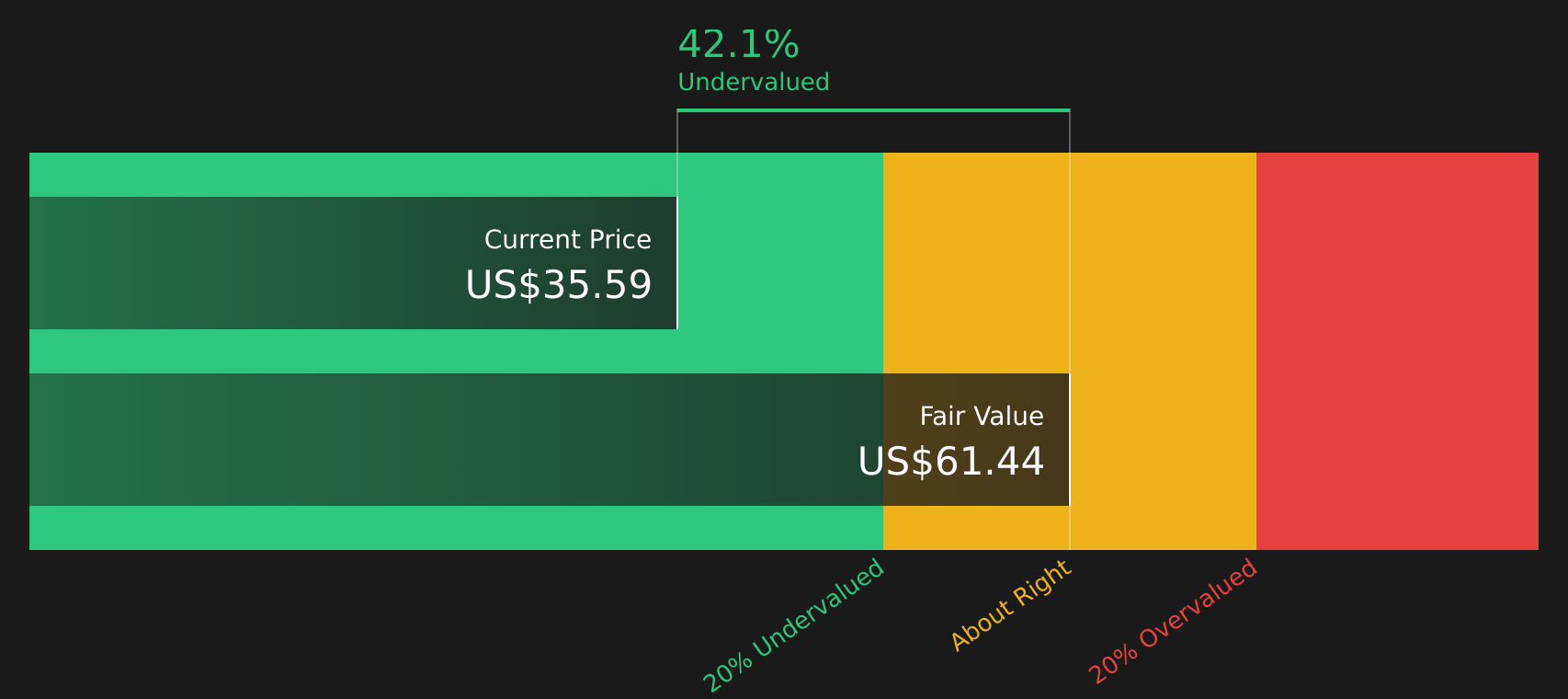

The Simply Wall St DCF model points to a fair value of $60.30 for Robert Half, compared with the current share price of $32.34. This suggests the stock appears undervalued on this approach, particularly when viewed alongside its weaker 1 year and 5 year return record. The key question for investors is whether they agree with the cash flow and margin assumptions underlying that estimate.

Next Steps

With mixed signals around Robert Half, it makes sense to move quickly, review the underlying data, and decide where you stand on the stock. To see both the concerns and the potential upside in one place, take a look at the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Robert Half?

If Robert Half has sharpened your focus on quality opportunities, do not stop here. Use Simply Wall St tools to surface fresh stock ideas that fit your style.

- Target potential mispricings by scanning 44 high quality undervalued stocks that combine solid fundamentals with prices that may not fully reflect their underlying businesses.

- Strengthen your income playbook by reviewing 9 dividend fortresses that pair higher yields with business models focused on sustaining regular payouts.

- Prioritise resilience by filtering for 67 resilient stocks with low risk scores designed to highlight companies with steadier profiles and fewer red flags.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.