Rocket Companies (RKT) Wins Fresh Coverage, Is The Stock Cheap?

Rocket RKT | 0.00 |

Rocket Companies (RKT) is back in focus after Benchmark initiated coverage with a positive view on its role in online real estate, coinciding with supportive housing and mortgage data that have drawn fresh attention to the stock.

The recent 7 day share price return of 7.6% and 30 day share price return of 11.78%, helped by Benchmark’s new coverage and stronger housing data, contrasts with a year to date share price decline of 20.27% and a 3 year total shareholder return of 80.88%. This suggests longer term holders have seen stronger overall gains than recent buyers.

If Rocket Companies has put real estate back on your radar, this could be a good moment to broaden your search and check out 20 top founder-led companies

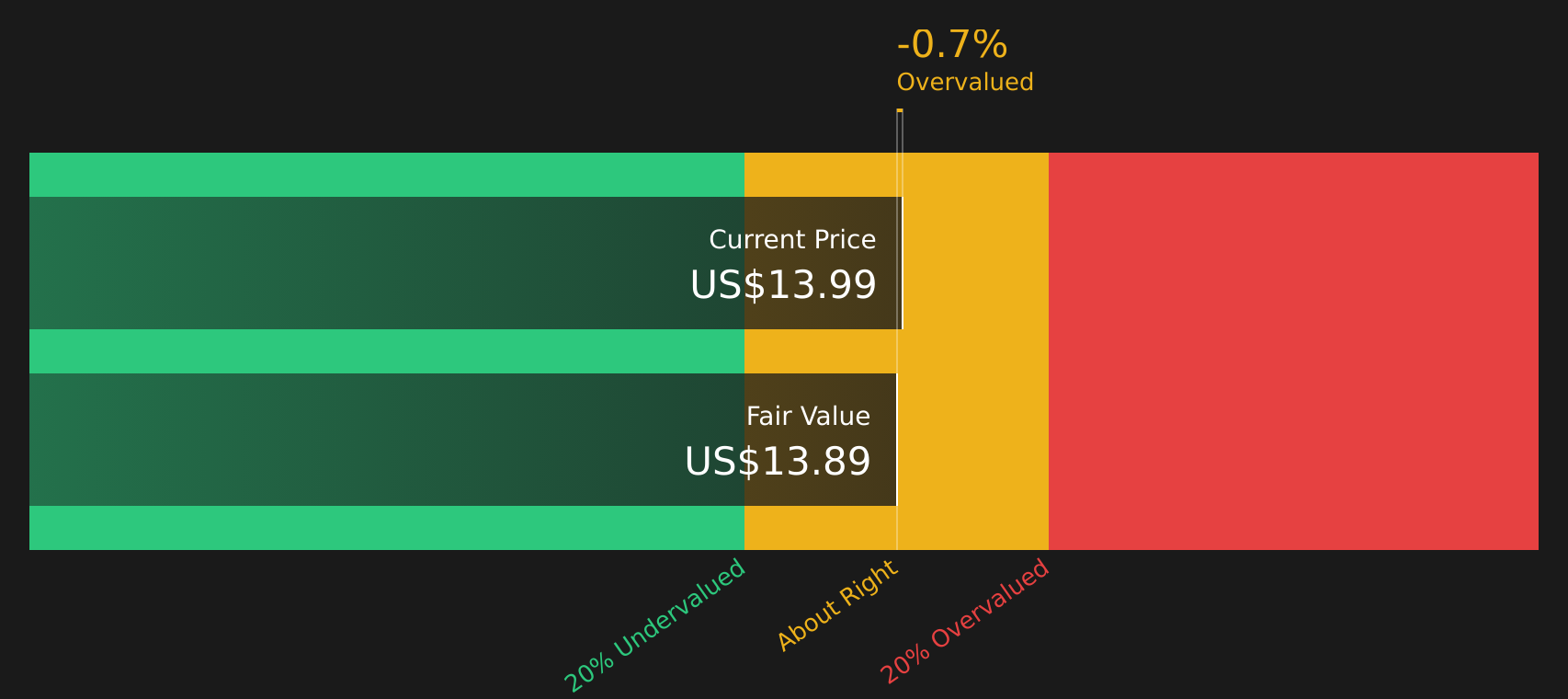

With Rocket Companies now valued at about US$44b after a sharp multi day run and trading below some analyst targets but above some fair value estimates, the key question is whether this remains a buying opportunity or whether markets are already pricing in future growth.

Most Popular Narrative: 21% Undervalued

Rocket Companies last closed at $15.85 compared with a widely followed fair value estimate of about $20.05, creating a clear valuation gap that current headlines alone do not explain.

The integration of Redfin and the planned acquisition of Mr. Cooper are expanding Rocket's customer reach and local agent network, which is unlocking new cross sell and purchase opportunities, potentially driving higher revenues and customer lifetime value in the long term.

Want to see what supports that kind of upside for Rocket Companies? The narrative leans heavily on faster earnings growth, rising margins and a richer profit multiple. Curious how those elements fit together to reach that fair value and what assumptions need to hold for years to come?

Result: Fair Value of $20.05 (UNDERVALUED)

However, Rocket Companies still faces two key swing factors: housing affordability pressures that could limit mortgage demand, and rising fintech competition that may squeeze margins and required tech spending.

Another View: Rocket Companies Through a Cash Flow Lens

There is another angle to Rocket Companies worth keeping in mind. While the analyst narrative points to a fair value of $20.05, our DCF model, which focuses on projected future cash flows, suggests a value closer to $12.40. This implies the stock is overvalued on that basis. Which set of assumptions do you find more realistic for the next few years?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Rocket Companies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Seen enough mixed signals on Rocket Companies for one sitting? Act while the details are fresh, compare the upside and downside, and ground your judgment in the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Rocket Companies?

Before moving on from Rocket Companies, take a moment to widen your watchlist. You could miss out on other stocks that better match your risk and income goals.

- Target resilient balance sheets and steadier fundamentals by scanning the solid balance sheet and fundamentals stocks screener (47 results) tailored to companies with stronger financial footing.

- Hunt for potential value opportunities by reviewing the 41 high quality undervalued stocks that filters for quality businesses trading below their estimated worth.

- Build a steadier income stream by checking the 8 dividend fortresses focused on higher yielding companies with more durable payout profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.