Rocket Lab News Has Investors Rethinking Aerospace And Satellite Communication Stocks

HawkEye 360, Inc. HAWK | 0.00 |

SpaceX’s rebound and fresh enthusiasm around satellite communications have turned a niche corner of aerospace into a focus for many investors overnight. With call option activity heavily outweighing puts and Rocket Lab’s new agreement with Iridium Communications drawing attention to space related partnerships, interest is spreading beyond private markets and smaller contractors. This article looks at how that news connects back to large, financially solid aerospace stocks, and identifies 3 companies from a broader screener that appear most exposed to these headlines, helping you evaluate whether they deserve a closer look or a place on your watchlist.

HawkEye 360 (HAWK)

Overview: HawkEye 360 is a US based space enabled defense technology company that uses its own constellation of satellites and radio frequency (RF) analytics platform to help government and allied agencies monitor maritime activity, track military and extremist communications, protect borders, and support battlefield intelligence.

Operations: HawkEye 360 generates all of its US$144.5m in revenue from Aerospace & Defense, split between the United States at US$85.7m and international customers at US$58.8m.

Market Cap: US$2.1b

HawkEye 360 sits directly in the path of the renewed interest in space and satellite communications. It has a battlefield proven RF intelligence platform that addresses defense, intelligence, and national security needs in the US and overseas. Recent updates highlight strong revenue growth, multiple international contract wins, and fresh capital from its IPO and satellite launches, which together expand its data set for customers. At the same time, the company is still unprofitable, carries higher funding risk due to reliance on external borrowing, and trades on a P/S multiple well above aerospace and defense peers. With Wall Street divided between very bullish and more cautious views, the key consideration is whether the growth and contract momentum justify that premium.

HawkEye 360’s rapid contract wins and premium P/S multiple suggest investors are pricing in a very specific outcome, but the real story sits inside the 4 key rewards and 1 important warning sign

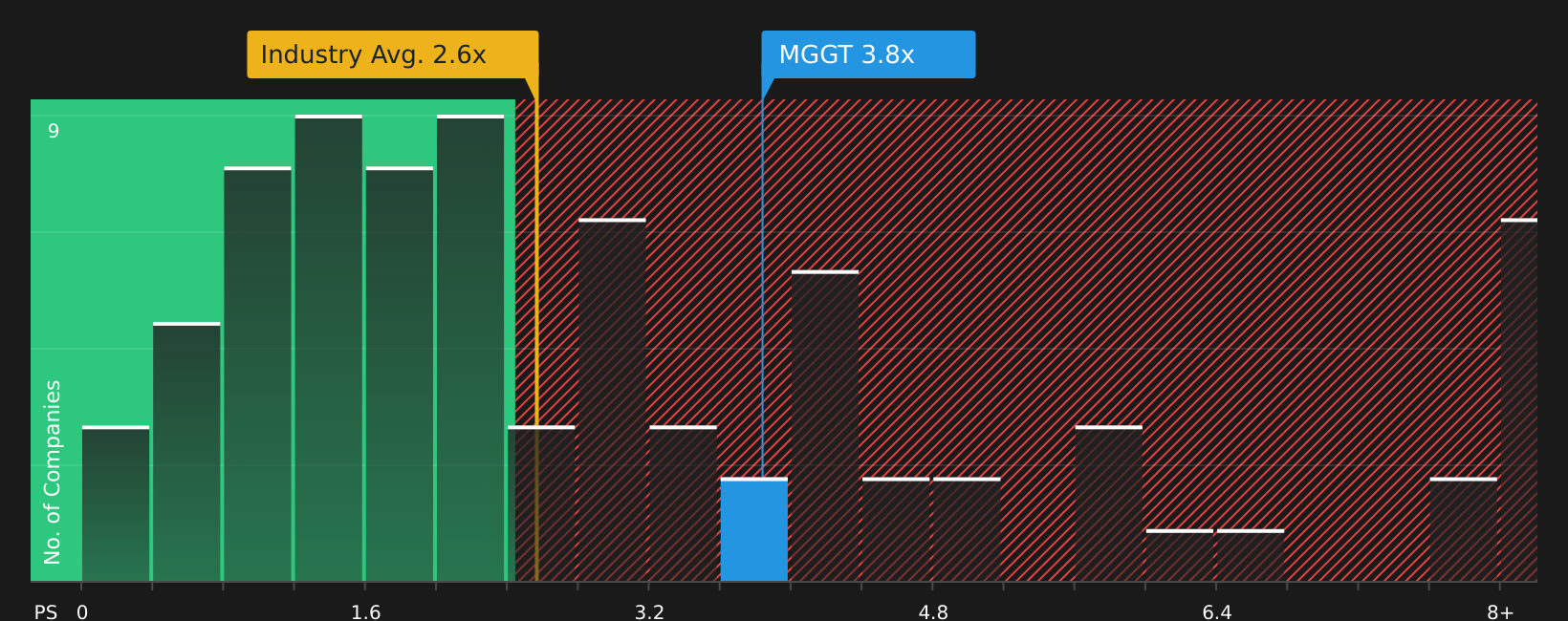

Meggitt (LSE:MGGT)

Overview: Meggitt is a long established UK aerospace and defense supplier that makes critical components and sub systems for aircraft and energy equipment, from braking and fuel systems to sensors, fire protection and training solutions used by commercial airlines, militaries and industrial customers worldwide.

Market Cap: £6.2b

Meggitt looks interesting in the current wave of enthusiasm for space and satellite communications because it already supplies key hardware for aircraft, defense platforms and space related infrastructure, giving it direct exposure to any sustained pick up in demand. Analysts expect revenue and earnings growth ahead of the wider UK market, supported by stronger aerospace aftermarket activity and a focus on higher margin services, even though recent earnings fell sharply and net margins sit at just 0.3%. This comes alongside higher funding risk from external borrowing and a richer P/S ratio than many peers, so improving order intake and margin plans need to be weighed carefully against valuation and balance sheet pressure.

Accelerating aerospace demand with razor thin 0.3% margins makes Meggitt look like a story investors have not fully priced in yet, and the real tension between growth plans, valuation and balance sheet shows up in the 2 key rewards and 2 important warning signs

Vicor (VICR)

Overview: Vicor designs and manufactures high performance power modules and custom power systems that convert electricity for use in demanding electronics, supplying original equipment makers across aerospace, satellites, defense, data centers, automotive and industrial markets worldwide.

Operations: Vicor generates all of its US$426.7m in revenue from Advanced Products or Brick Products, with US$221.5m from the United States, US$156.6m from Asia Pacific, US$46.6m from Europe and the remainder from other regions.

Market Cap: US$14.9b

Vicor sits at the intersection of two themes in this screener: rising interest in satellite communications after the SpaceX and Rocket Lab headlines, and the heavy computing and automotive demand behind AI and electrification. The company has reported very strong recent earnings momentum, expanding net margins to 32% and reporting record quarterly revenue, while licensing income and IP enforcement add high margin royalty streams on top of product sales. That strength comes with trade offs, including a very high P/E, reliance on external borrowing, sizable one off gains and insider selling that may indicate potentially bumpier periods ahead. The key question is whether Vicor’s patents, manufacturing build out and exposure to AI, aerospace and satellite systems are enough to justify those expectations or signal caution.

Vicor’s rapid earnings momentum, rich P/E and patent heavy model make the story feel like it is only half told, and the missing chapter sits inside the 2 key rewards and 3 important warning signs

The three aerospace and satellite communications stocks covered here are only a starting point. The full screener has surfaced 38 more companies with equally compelling narratives around launch services, RF data, defense exposure and space infrastructure in the Aerospace and Satellite Communications screener. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter to you so you can focus on the highest conviction opportunities in this theme.

Take Control of Your Investment Journey

If HawkEye 360 or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Stocks

New breakout stories are forming while you read this, and the best entry points often vanish once momentum is clearly flying. Scan these fresh ideas before the crowd and act now.

- Spot under the radar strength in quality companies by reviewing a curated list of solid balance sheet and fundamentals (48 results). This can help you avoid chasing stretched balance sheets later.

- Consider the structural shift toward smarter automation by checking out carefully selected 29 robotics and automation stocks that could be positioned to benefit as demand for productivity tools evolves.

- Evaluate AI infrastructure spending trends by assessing focused 52 AI infrastructure stocks before attention potentially broadens and entry points change.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.