Royalty Pharma (RPRX) Could Be 2% Undervalued On Russell 1000 Defensive Index Addition

Royalty pharma plc RPRX | 0.00 |

Royalty Pharma (RPRX) has just been added to both the Russell 1000 Value-Defensive Index and the Russell 1000 Defensive Index, a shift that often attracts closer attention from index-tracking and passive funds.

That index inclusion comes after a period of strong momentum for Royalty Pharma, with a 90-day share price return of 20.67%, a year-to-date share price return of 48.74%, and a 1-year total shareholder return of 66.26%.

If you are using this news as a prompt to widen your watchlist, it could be worth scanning other healthcare-related opportunities through our screener for 40 healthcare AI stocks

After Royalty Pharma’s sharp move and fresh index inclusion, buying now means paying up for that momentum, while waiting risks missing further repricing. How does the current valuation stack up against what you are actually getting?

Most Popular Narrative: 2% Undervalued

The most followed narrative currently pegs Royalty Pharma’s fair value at $59.25, just above the last close of $57.80, which implies only a modest discount while still baking in ambitious forecasts.

The robust scientific pipeline, driven by advancements in biologics, gene therapies, and next-generation medicines like daraxonrasib, creates high-value assets that can enter into blockbuster status. Participation in these early, high-impact assets (as in the Revolution Medicines deal) positions Royalty Pharma for long-duration, high-growth royalty streams, directly benefitting long-term revenue and earnings.

Want to see what is powering that valuation edge for Royalty Pharma? Revenue climbing faster than the market, margins stepping up sharply, and earnings pointed much higher all sit at the core of this storyline.

Result: Fair Value of $59.25 (UNDERVALUED)

However, Royalty Pharma’s story can quickly look different if the Alyftrek royalty dispute limits cash coming in, or if competition in royalty deals compresses returns on new assets.

Another View on Royalty Pharma’s Valuation

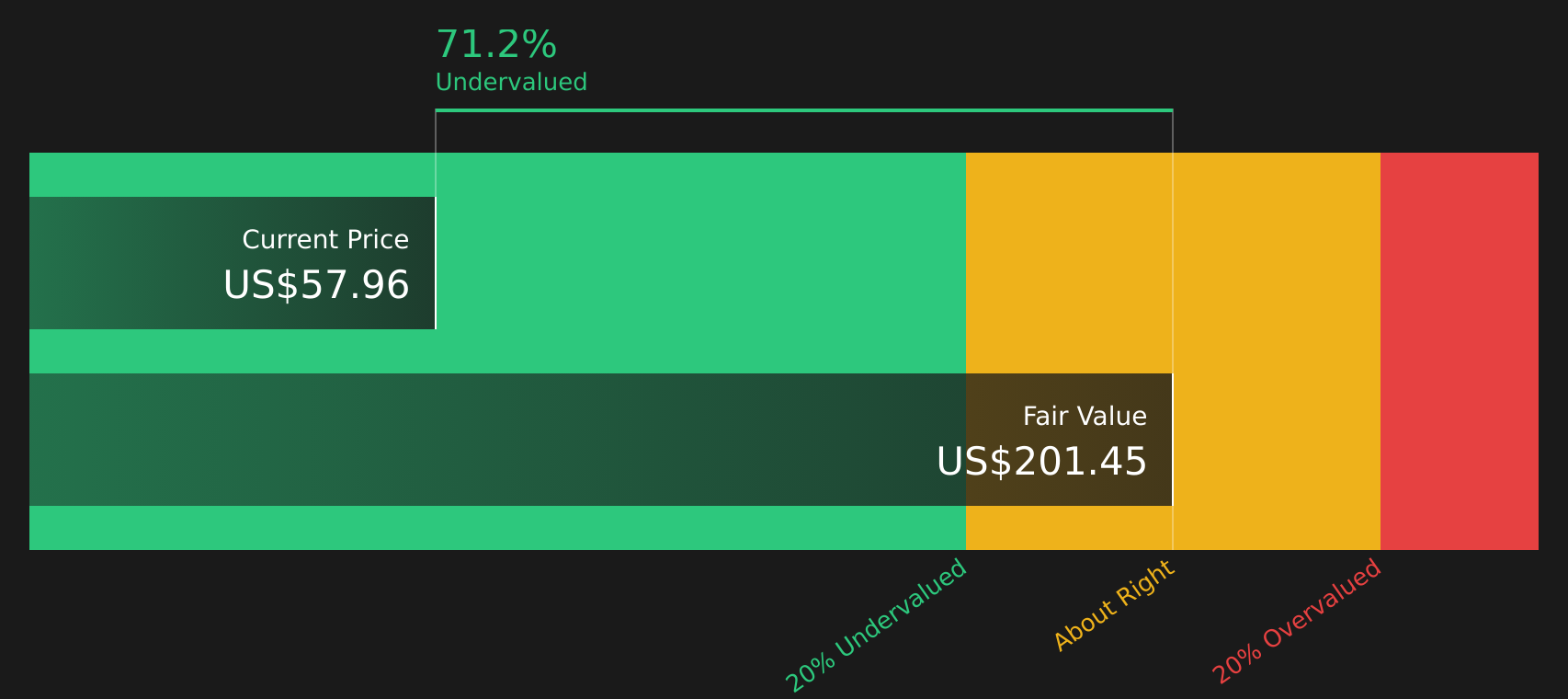

The analyst narrative frames Royalty Pharma as only about 2% undervalued against a $59.25 fair value, but the SWS DCF model presents a very different picture. With the stock at $57.80, it is shown as trading around 71% below an estimated future cash flow value of $201.45. Readers may wish to consider which assessment appears more reasonable based on their own interpretation of the data.

To understand how that gap emerges from long term cash flow assumptions and discount rates, it is useful to look at how the SWS DCF model has been applied to Royalty Pharma in detail, rather than relying on a single headline number. Look into how the SWS DCF model arrives at its fair value.

Next Steps

Given the mixed signals around Royalty Pharma’s valuation and outlook, it makes sense to review the numbers yourself and then move promptly to a clear stance using 2 key rewards and 3 important warning signs

Looking for more investment ideas beyond Royalty Pharma?

If Royalty Pharma has your attention, do not stop there. Broaden your opportunity set with high quality stocks that fit clear, disciplined criteria using the Simply Wall Street Screener.

- Strengthen your core holdings with companies that show robust financial footing and disciplined fundamentals by running the solid balance sheet and fundamentals stocks screener (47 results).

- Hunt for potential mispriced opportunities by scanning the 45 high quality undervalued stocks that pair compelling valuations with underlying business quality.

- Lock in steadier portfolio candidates by reviewing the 74 resilient stocks with low risk scores that prioritise resilience and lower overall risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.