Royalty Pharma (RPRX) Valuation Check After Strong Q1 Earnings And Rising Investor Interest

Royalty pharma plc RPRX | 0.00 |

Royalty Pharma earnings and buyback catch investors’ attention

Royalty Pharma (RPRX) has drawn fresh investor focus after reporting first quarter 2026 earnings with revenue of US$630.58 million and net income of US$294.69 million, alongside continued progress on its multi year share repurchase program.

The stock has picked up momentum, with a 1 day share price return of 3.0% and a year to date share price return of 37.03%, while the 1 year total shareholder return of 68.83% signals that recent strength builds on a solid longer term outcome.

If earnings and buybacks have you rethinking healthcare exposure, it could be worth scanning the broader opportunity set through the 33 healthcare AI stocks

With revenue at US$630.58 million, net income at US$294.69 million, a 68.83% 1 year total shareholder return and shares trading below the average analyst price target, is there still a buying opportunity here or is the market already pricing in future growth?

Most Popular Narrative: 3% Overvalued

Royalty Pharma’s most followed valuation narrative pegs fair value at $51.56, slightly below the last close at $53.25. This frames current enthusiasm against a modest premium to that estimate.

Strategic reinvestment of large, stable cash flows into new and increasingly innovative royalty acquisitions, enhanced by improved data-driven diligence and risk management, allows Royalty Pharma to continually expand its portfolio with attractive economics, increasing operating leverage and net margins over time.

Read the complete narrative. Read the complete narrative.

Curious what kind of revenue path, margin reset and future earnings multiple need to line up to support that valuation? The narrative builds a detailed case using explicit growth, profitability and discount rate assumptions, and sets a bar for how the stock would need to be priced a few years from now to justify today’s fair value line in the sand.

Result: Fair Value of $51.56 (OVERVALUED)

However, there are still pressure points to watch, including the Vertex royalty dispute and growing competition for royalty deals, which could challenge those fair value assumptions.

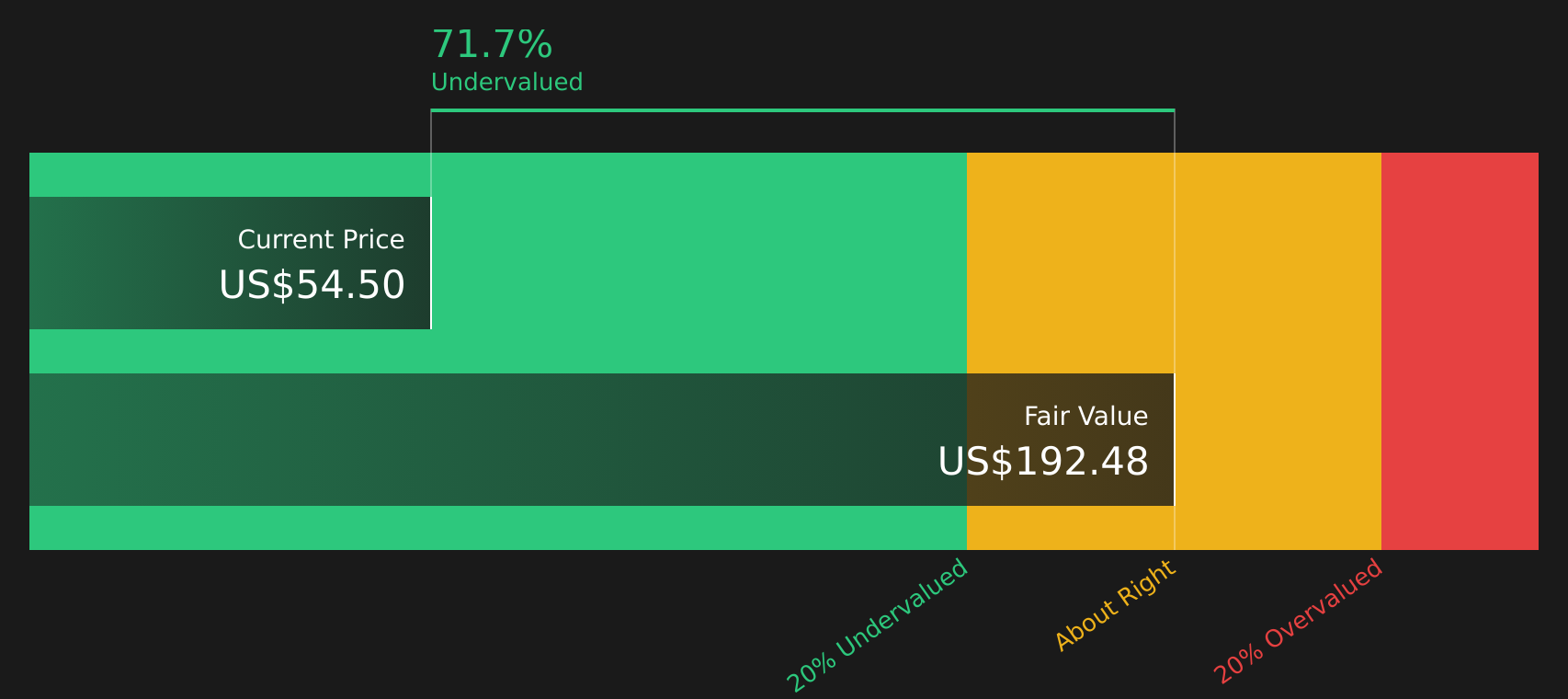

Another View: Cash Flows Paint A Different Picture

The narrative based on analyst assumptions concludes that Royalty Pharma is modestly overvalued around $53.25 versus a fair value estimate of $51.56. Our DCF model tells a very different story, with a future cash flow value of $192.48, which implies the stock trades at a steep discount. Which set of assumptions feels more realistic to you?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Royalty Pharma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across valuation models and sentiment, the real edge comes from understanding the details for yourself. Move quickly, review the underlying data and weigh the 2 key rewards and 3 important warning signs

Looking for more investment ideas?

If you stop with just one stock, you may miss opportunities that fit your goals even better, so use the tools available and keep your watchlist evolving.

- Spot potential value opportunities before they are widely followed by checking out the screener containing 23 high quality undiscovered gems.

- Strengthen your portfolio’s foundation by reviewing companies featured in the solid balance sheet and fundamentals stocks screener (45 results).

- Target income focused opportunities by screening for stocks in the 14 dividend fortresses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.