Sable Offshore (SOC) Raises Fresh Capital, Is The Stock Trading At A Discount?

Sable Offshore SOC | 0.00 |

Capital raising moves put Sable Offshore in focus

Sable Offshore (SOC) has attracted fresh attention after unveiling a dual capital raise: a $300 million fixed rate convertible note offering alongside a $100 million follow-on equity issuance.

The concurrent bond and stock offerings highlight active balance sheet management at Sable Offshore, prompting investors to reassess how the company might fund future obligations, address existing debt and position itself for potential corporate initiatives.

Against this backdrop of refinancing and fresh capital, Sable Offshore’s share price has come under heavy pressure, with the stock down 78.98% on a 30 day share price return and recording an 85.67% decline in 1 year total shareholder return.

If you are weighing up what to watch next as this refinancing story plays out, it may be a good time to broaden your search and check out 33 elite gold producer stocks

With Sable Offshore’s stock under heavy pressure despite recent revenue growth and a sizeable capital raise, the key question is whether sentiment has swung too far and created a potential entry point, or if markets are already pricing in future growth.

DCF valuation suggests a wide gap to Sable Offshore’s share price

Sable Offshore is currently trading at $3.08, while the SWS DCF model estimates the value of its future cash flows at $413.63 per share. This implies a very large gap between the modelled fair value and the market price.

The DCF model works by projecting the cash Sable Offshore could generate in the future, then discounting those cash flows back to today using a required rate of return. The sum of those discounted cash flows produces an estimate of what the stock might be worth on a per share basis.

For a company like Sable Offshore, which is currently unprofitable and reports a loss of $497.64m alongside limited reported revenue of about $1.27m, this kind of cash flow based approach can be particularly sensitive to assumptions. Forecasts indicating revenue growth and an eventual move into profitability play a central role in producing such a high DCF value relative to the current $3.08 price. Small changes in those inputs can have a large impact on the output.

Result: DCF Fair value of $413.63 (UNDERVALUED)

However, Sable Offshore still carries meaningful risk, including ongoing losses of $497.64m and share price declines of 85.67% in 1 year total shareholder return.

Another view on Sable Offshore’s valuation

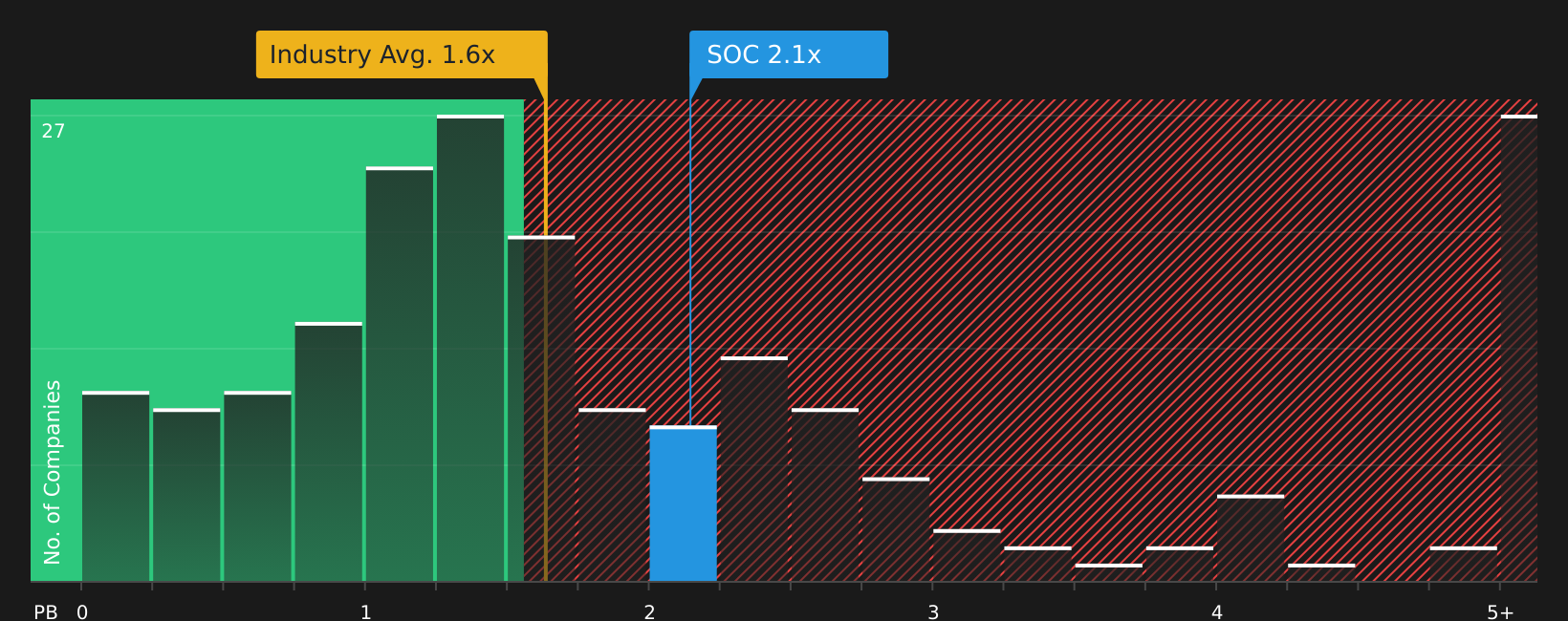

While the SWS DCF model points to a very large gap between fair value and Sable Offshore’s $3.08 share price, traditional balance sheet metrics send a different signal. SOC trades at a P/B of 1.1x compared with 1.5x for the US Oil and Gas industry and 36.8x for peers, suggesting a more modest discount anchored in current assets and liabilities.

That contrast leaves a key question for you as an investor: is the DCF highlighting future potential the market is ignoring, or are book based measures a better guide to what Sable Offshore is worth today?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sable Offshore for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 43 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals around Sable Offshore, are markets being too harsh or simply realistic about the risks and rewards on the table? Act while sentiment is unsettled by reviewing the company data, weighing the concerns and potential upside, and checking the 2 key rewards and 5 important warning signs

Looking for more investment ideas beyond Sable Offshore?

Do not stop with Sable Offshore; use this moment to widen your watchlist with fresh ideas that match your style before other investors move first.

- Target potential mispricing by scanning 43 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their underlying businesses.

- Strengthen your income stream by reviewing 10 dividend fortresses that focus on higher yielding companies screened for consistency and balance sheet support.

- Prioritise resilience by leaning on 74 resilient stocks with low risk scores so you can focus on companies assessed to have lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.