Saia (SAIA) Valuation in Focus After Analyst Reaffirms Positive Outlook Despite Lower Price Target

Saia, Inc. SAIA | 351.28 351.28 | +4.54% 0.00% Pre |

Saia (SAIA) stock climbed 5.9% following JPMorgan's decision to reaffirm a positive rating on the company, even though the price target was lowered. The market seemed to welcome this vote of confidence.

Saia's latest jump comes after a challenging stretch, with the 1-year total shareholder return down 36.5%. Headwinds such as shifting industry classifications and uneven profitability in new regions have weighed on sentiment. However, today’s positive reaction hints that investor confidence may be firming up. While momentum has been soft so far this year, Saia’s impressive 3-year total return of nearly 50% shows why many still see long-term potential as the logistics landscape evolves.

If today’s move has you rethinking what else is out there, it’s the perfect moment to expand your radar and discover fast growing stocks with high insider ownership

With analyst optimism contrasting Saia’s recent stock underperformance, the question now is whether shares are trading below their true value or if the market has already accounted for the company’s future growth prospects.

Most Popular Narrative: 12.8% Undervalued

With Saia trading last at $294.23, the most widely-followed narrative places fair value at $337.25. This difference is driven by robust future expectations and strategic growth levers analysts believe are coming into play.

The ongoing expansion and maturation of Saia's national terminal network, combined with network densification, is starting to unlock cost efficiencies and higher shipment volumes in new and legacy markets. This positions the company for top-line revenue growth and improved operating margins as these facilities move toward scale.

Want to know the secret sauce behind Saia’s valuation? This forecast hinges on ambitious revenue and profit margin expansion, along with a pivotal shift in how the company leverages its growing logistics network. Uncover the analyst assumptions fueling that fair value and see if the optimism is warranted.

Result: Fair Value of $337.25 (UNDERVALUED)

However, persistent muted shipment growth and rising operating costs could challenge Saia’s ability to achieve the optimistic growth and margin targets that analysts expect.

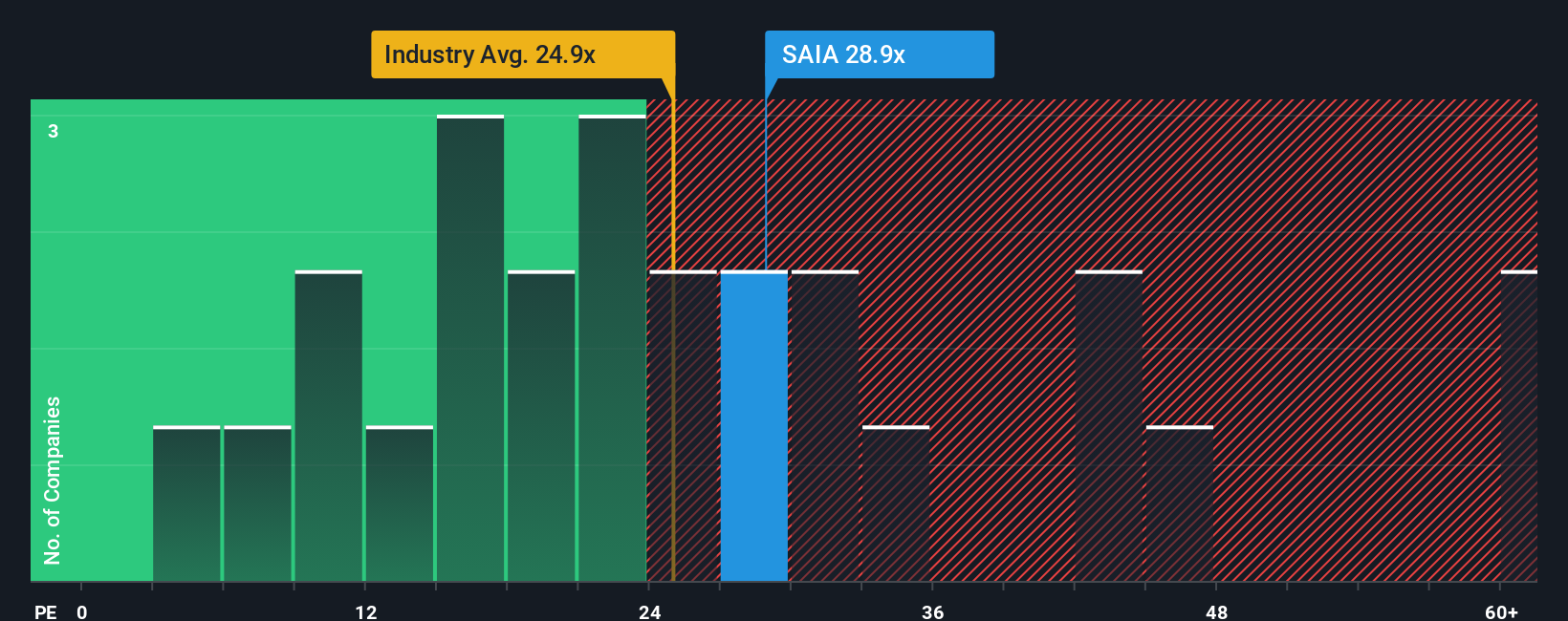

Another View: What Do Its Ratios Say?

Looking through the lens of valuation ratios, Saia’s shares currently trade at 26.9 times earnings. This is above the US Transportation industry average of 24 times and nearly double the fair ratio of 14. Among its peers, the average is even higher at 33.5, placing Saia closer to the middle of its class. However, a wide gap to the fair ratio can signal increased downside risk if sentiment changes or earnings do not meet expectations. Is the current premium justified or could it disappear as fundamentals develop?

Build Your Own Saia Narrative

If these perspectives don’t quite match your view, or if you want to dig into the numbers personally, you can build your own story in just a few minutes. Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Saia.

Looking for more investment ideas?

Step beyond Saia and get ahead of the market by finding stocks with outstanding potential. Use these handpicked shortlists before the best opportunities get snapped up.

- Lock in consistent incomes by targeting attractive yields through these 19 dividend stocks with yields > 3%, which outshine traditional savings and deliver powerful compounding benefits.

- Unleash the possibilities of digital finance when you explore these 79 cryptocurrency and blockchain stocks at the forefront of blockchain innovation and next-generation payment systems.

- Seize early-stage growth with these 3586 penny stocks with strong financials, offering the potential for impressive returns. Join forward-thinking investors spotting value ahead of the crowd.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.