Salesforce (CRM) Is Down 9.9% After Landmark U.S. Army AI Contract And EMBERPOINT Role - Has The Bull Case Changed?

Salesforce.com, inc. CRM | 187.18 | +0.50% |

- In late January 2026, Salesforce announced a US$5.60 billion, 10‑year IDIQ contract with the U.S. Army and joined EMBERPOINT LLC alongside Lockheed Martin, PG&E and Wells Fargo to supply AI‑enabled data, cloud and coordination tools for defense and wildfire mitigation.

- These moves highlight how Salesforce is positioning its Agentforce and data platforms at the core of mission‑critical government and public‑safety systems, even as software peers face mounting AI‑related business model questions.

- Next, we’ll explore how this major U.S. Army contract and Salesforce’s AI focus could reshape the company’s longer‑term investment narrative.

Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

What Is Salesforce's Investment Narrative?

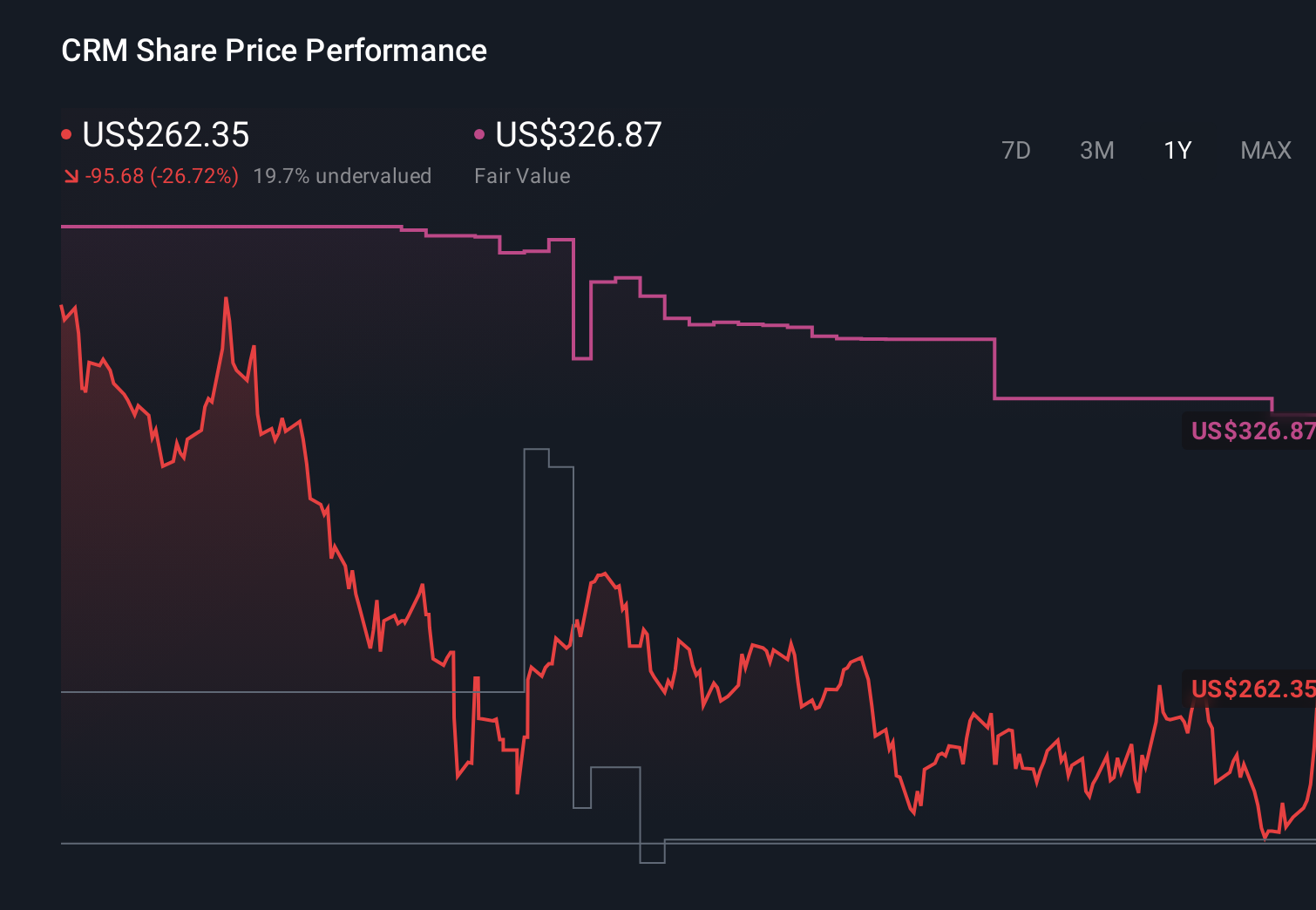

To stick with Salesforce after a 40% one‑year total return slide, you have to believe the core Customer 360, Data 360 and Agentforce stack can stay central to how large organisations run sales, service and operations, even if AI agents reshape how software is bought and priced. The US$5.60 billion, 10‑year U.S. Army IDIQ deal and the EMBERPOINT wildfire venture give that thesis some real‑world backing, anchoring Salesforce inside long‑duration, mission‑critical workloads at a moment when investors are questioning the durability of subscription models. In the near term, though, the key catalysts still sit around the February 25 earnings call, updated AI monetisation detail and any colour on renewals and seat counts, while risks center on AI pressure on per‑seat pricing, leadership churn in acquired clouds and whether recent AI wins meaningfully offset sector‑wide multiple compression.

However, one risk around AI’s impact on Salesforce’s seat‑based pricing power deserves closer attention. Despite retreating, Salesforce's shares might still be trading 42% above their fair value. Discover the potential downside here.Exploring Other Perspectives

Across 42 views in the Simply Wall St Community, fair value estimates span roughly US$242 to US$435 per share, reflecting sharply different expectations for Salesforce’s AI transition. That spread sits against a backdrop where the new US$5.60 billion Army contract could influence how investors think about long term demand resilience and short term worries over AI squeezing subscription revenues. You can compare these community views with the changing risk picture around AI agents, margins and enterprise budgets.

Explore 42 other fair value estimates on Salesforce - why the stock might be worth over 2x more than the current price!

Build Your Own Salesforce Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Salesforce research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Salesforce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Salesforce's overall financial health at a glance.

No Opportunity In Salesforce?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 53 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 14 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.