SanDisk (SNDK): Assessing Valuation After Buying Surge and AI-Fueled Sentiment Shift

Sandisk Corporation SNDK | 0.00 |

Sandisk (SNDK) caught the attention of traders after a recent Power Inflow alert suggested renewed buying interest from both institutions and individual investors. This followed an earlier drop in the share price.

The Power Inflow alert came as Sandisk’s 1-day share price return jumped 3.85 percent, capping off a remarkable 61.21 percent return for the month and an eye-catching 475 percent rise year-to-date. This surge signals renewed momentum, as investors grow more optimistic about prospects for memory and storage companies riding the AI-fueled demand wave.

If Sandisk’s rebound caught your attention, now could be a perfect moment to broaden your search and discover fast growing stocks with high insider ownership

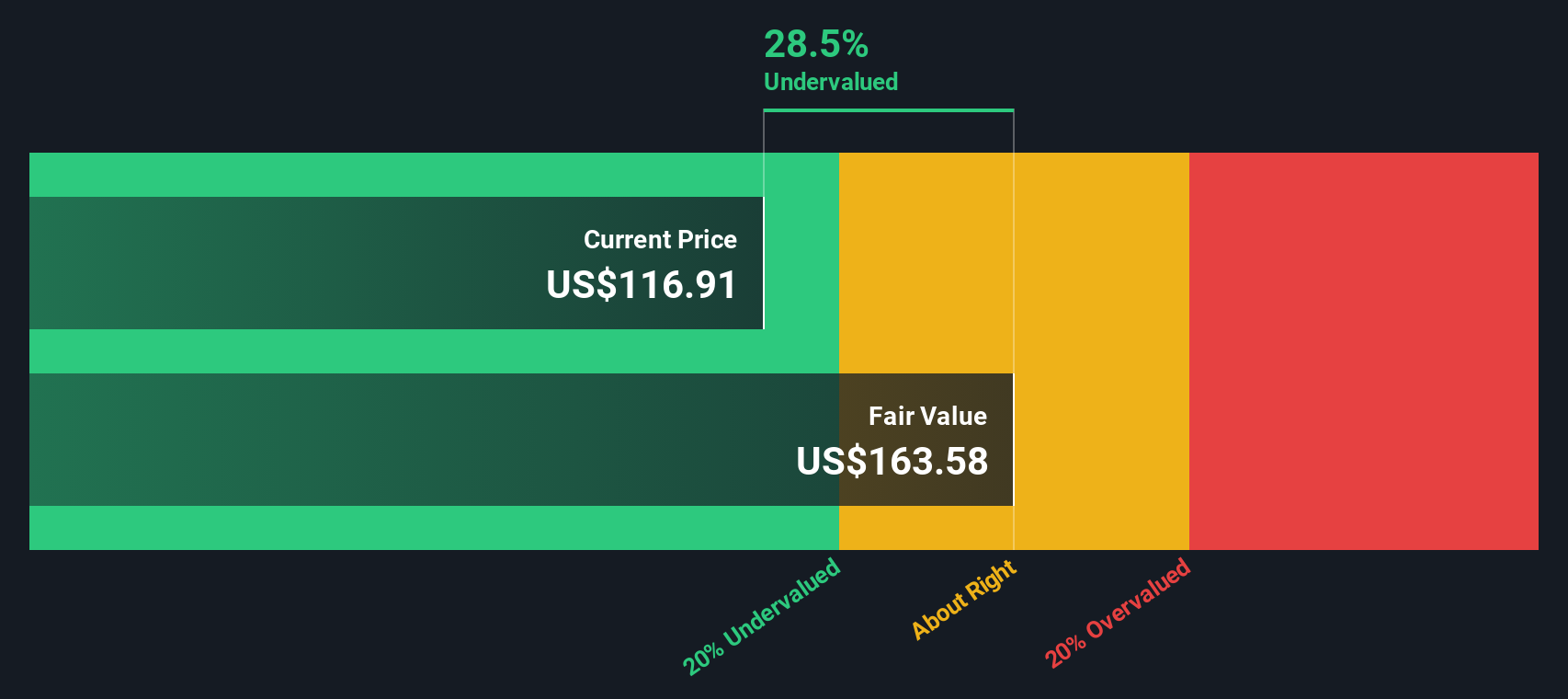

But with Sandisk’s shares soaring after a sharp rebound and analyst targets both rising and trailing the current price, the big question for investors remains: is there still value to be found here, or has the market already priced in future growth?

Price-to-Sales of 4.1x: Is it justified?

Sandisk’s current price-to-sales ratio stands at 4.1x, putting its shares at a premium compared to both peer companies and the broader US technology sector. With the stock trading at $207.01, this valuation suggests investors are willing to pay up for future growth potential, even as the share price accelerates well above typical benchmarks.

The price-to-sales ratio measures the relationship between a company’s market value and its annual revenue. This metric is useful for technology companies that may not be consistently profitable but remain in high-growth phases. The ratio is especially relevant for Sandisk, which is currently unprofitable but has shown strong annual revenue growth.

However, at 4.1x, Sandisk’s price-to-sales ratio is more expensive than the US Tech industry average of 2x and the peer group average of 3.7x. A fair value estimate for Sandisk’s price-to-sales multiple is 3.4x, suggesting that current pricing is stretched. If market sentiment cools or growth falls short, the multiple could compress towards this level.

Result: Price-to-Sales of 4.1x (OVERVALUED)

However, continued unprofitability or a pullback in AI-driven demand could quickly undermine the bullish thesis that investors are currently buying into.

Another View: DCF Puts the Spotlight on Overvaluation

While the price-to-sales ratio suggests Sandisk may be trading at a premium, our DCF model offers a different perspective. Based on a discounted cash flow analysis, the stock's fair value is estimated at $168.12, noticeably below the current price. This implies that Sandisk could be overvalued even when factoring in future cash flow growth.

With two different methods both pointing to potential overvaluation, the question remains: will Sandisk’s growth story be enough to sustain investor confidence, or will the stock eventually realign with fundamentals?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sandisk for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 842 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sandisk Narrative

If you see the story unfolding differently or want to dive into the details yourself, creating your own analysis takes just a few minutes. Do it your way

A great starting point for your Sandisk research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Take charge of your financial goals and see what’s possible beyond Sandisk. Uncover fresh opportunities that others often overlook and keep your portfolio one step ahead.

- Capture reliable income streams by tapping into these 18 dividend stocks with yields > 3% with yields above 3 percent. This approach is designed for building steady returns regardless of market swings.

- Capitalize on groundbreaking breakthroughs and innovations by exploring these 26 AI penny stocks poised to drive the next great wave in artificial intelligence.

- Secure outstanding value by targeting these 842 undervalued stocks based on cash flows showing real upside based on solid underlying cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.