Sanmina (SANM) Valuation Check After Q1 Results ZT Systems Deal And Share Buyback

Sanmina Corporation SANM | 130.21 | +0.02% |

What Sanmina’s latest quarter and guidance signal for investors

Sanmina (SANM) has drawn fresh attention after reporting first quarter results, issuing second quarter revenue guidance of US$3.1b to US$3.4b, and completing a share buyback that retired 2.46% of its stock.

The company reported first quarter sales of US$3,189.69m, with demand linked to communications networks, cloud infrastructure, and early shipments of next generation AI infrastructure products. Net income came in at US$49.29m.

Sanmina’s latest earnings, guidance and buyback sit against a mixed share price backdrop, with a 5.23% 1 day share price return and 73.51% 1 year total shareholder return contrasting with a 12.05% 3 month share price decline. This suggests momentum has cooled recently after strong longer term gains.

If Sanmina’s AI and cloud exposure has your attention, it could be a good moment to see what else is gaining traction in this space through our list of 33 AI infrastructure stocks.

With Sanmina’s shares down over the past 3 months but still showing very strong multi year returns, and with analysts’ price targets currently above the market price, is there still a buying opportunity here, or is future growth already reflected in the valuation?

Most Popular Narrative: 24.2% Undervalued

At a last close of $149.79 versus a narrative fair value of $197.50, the most followed Sanmina story is that the market is not fully pricing in its projected growth and profitability path.

The imminent acquisition of ZT Systems is expected to add $5–6 billion of annual run-rate revenue, positioning Sanmina to double its net revenue within three years and capitalize on explosive growth in data center and AI infrastructure investment. This is expected to provide a multi-year boost to overall revenue and EPS accretion from synergies and integration.

Curious how this kind of revenue step change, margin shift and future earnings multiple all fit together into one price? The narrative leans on specific growth, profitability and discount rate assumptions that are far from generic. Want to see exactly which forecasts have to line up for that fair value to hold?

Result: Fair Value of $197.50 (UNDERVALUED)

However, this hinges on smooth ZT Systems integration and stable demand from major customers. Any stumble on execution or orders could quickly challenge that underpriced growth story.

Another Angle On Sanmina’s Value

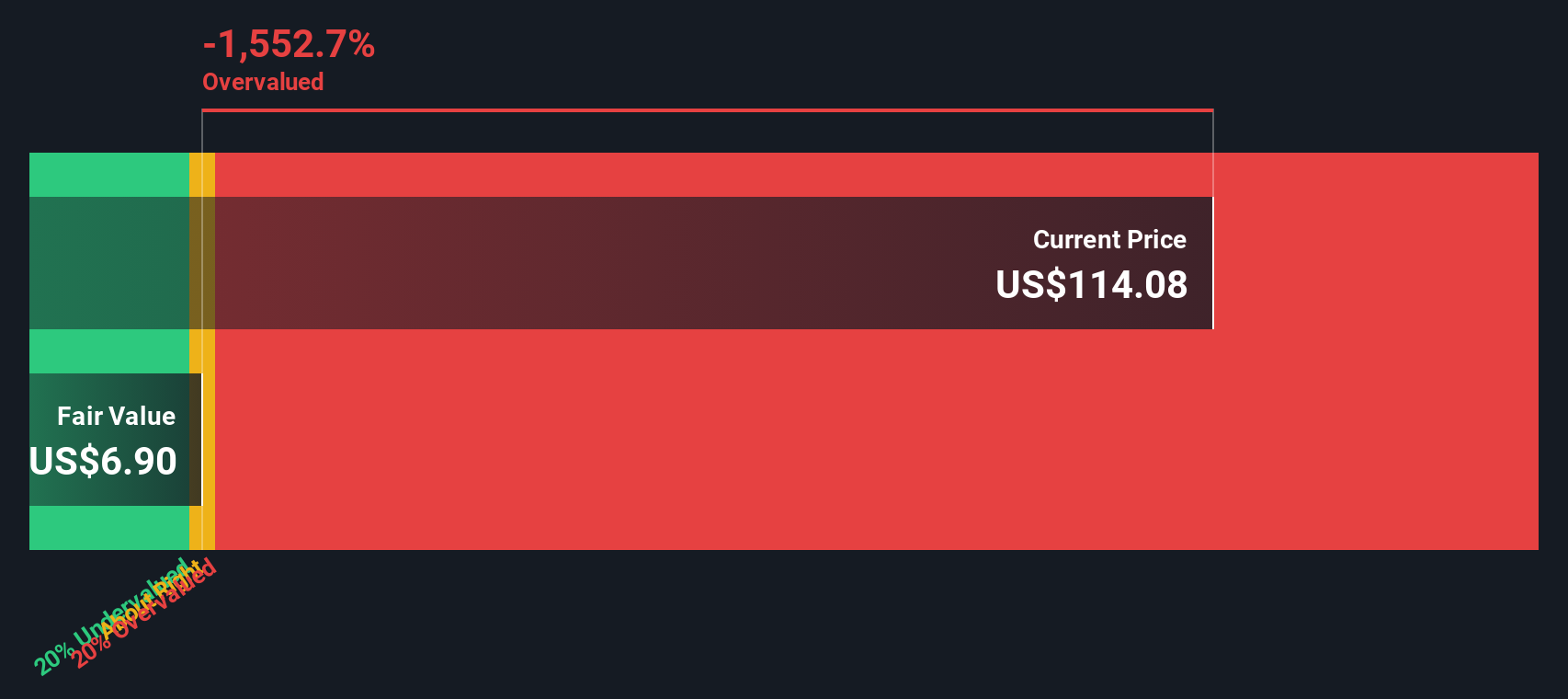

That 24.2% “undervalued” narrative differs from the signal from the SWS DCF model, which puts fair value at $76.94 versus the current $149.79. On this view Sanmina screens as overvalued. This presents two contrasting perspectives on how the market may price it over time.

Build Your Own Sanmina Narrative

If the story you are seeing here does not quite match your own view, you can test the assumptions yourself and shape a custom Sanmina thesis in minutes by starting with Do it your way.

A great starting point for your Sanmina research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Sanmina is only one piece of your watchlist, do not stop here. Use the screener to spot other opportunities that fit the kind of portfolio you want.

- Spot potential mispricings early by scanning 53 high quality undervalued stocks that pair strong fundamentals with what may be more modest expectations in the market price.

- Strengthen your income stream by reviewing 14 dividend fortresses that focus on companies offering yields of 5% or more alongside an emphasis on resilience.

- Protect against unwanted surprises by checking 87 resilient stocks with low risk scores which highlight businesses with lower risk scores that may suit a more cautious approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.