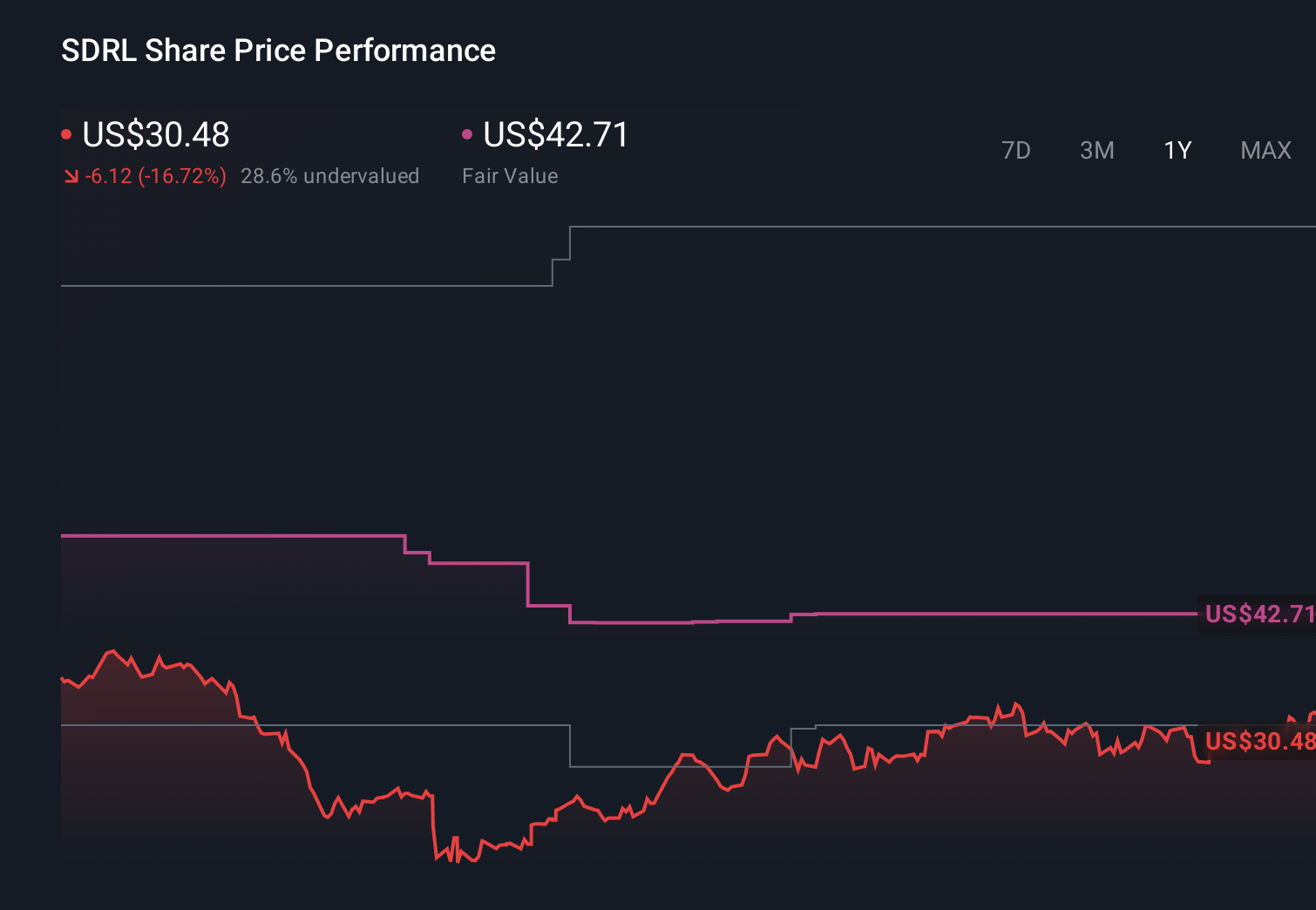

Seadrill (SDRL) Is Up 8.5% After Raising 2026 Revenue Guidance And Narrowing Q1 Losses – Has The Bull Case Changed?

Seadrill SDRL | 0.00 |

- In May 2026, Seadrill Limited reported first-quarter results showing revenue of US$358 million and a net loss of US$7 million, while also raising its full-year 2026 total operating revenue guidance to a range of US$1.43 billion to US$1.48 billion.

- The combination of higher quarterly revenue, a smaller loss than a year earlier, and upgraded full-year guidance signals operational momentum that may influence how investors view Seadrill’s earnings potential and risk profile.

- We’ll now examine how Seadrill’s upgraded 2026 revenue guidance reshapes the company’s investment narrative and expectations for future performance.

Find 54 companies with promising cash flow potential yet trading below their fair value.

Seadrill Investment Narrative Recap

To be a shareholder in Seadrill, you need to believe that offshore drilling demand and day rates will strengthen enough to turn an improving but still loss‑making business into a consistently profitable one. The raised 2026 revenue guidance, alongside a narrower quarterly loss, modestly supports that near term earnings catalyst, but it does not remove key risks around softer utilization, pricing pressure and idle rigs that could still weigh on margins and cash flows through 2026.

The recent upgrade to Seadrill’s 2026 revenue guidance to US$1.43 billion to US$1.48 billion is most closely tied to the steady flow of new contracts and extensions, such as the West Polaris extension with Petrobras that added about US$480 million of backlog. Together with other awards into 2027 and 2028, these contracts provide better visibility on near term revenue, while highlighting how any delays or gaps between projects could quickly become a material risk.

Yet investors should also be aware of how prolonged rig idle time or delayed approvals in regions like Angola could still...

Seadrill's narrative projects $1.7 billion revenue and $194.6 million earnings by 2029. This requires 6.8% yearly revenue growth and a $271.6 million earnings increase from -$77.0 million today.

Uncover how Seadrill's forecasts yield a $51.71 fair value, a 5% downside to its current price.

Exploring Other Perspectives

Some of the more pessimistic analysts were only assuming about US$1.5 billion of revenue and roughly US$219 million of earnings by 2029, so this guidance beat may eventually nudge their view, but it also sits alongside their concern that rising regulatory and ESG costs could still compress margins even if revenue grows.

Explore 6 other fair value estimates on Seadrill - why the stock might be worth as much as 78% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Seadrill research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Seadrill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Seadrill's overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.