Seadrill Stock And 2 Energy Picks Backed By Oil Supply Recovery

Seadrill Limited SDRL | 0.00 |

The sudden reopening of the Strait of Hormuz has shifted attention back to how vulnerable many portfolios are to changes in global trade routes and energy flows. With shipments restarting through this critical chokepoint and a 60 day negotiation clock ticking, investors are weighing both the relief in supply chains and the political uncertainty that comes with it. This article looks at 3 stocks from our Energy and Oil Shipping Sector screener that are directly exposed to this news, highlighting where the renewed traffic could support business activity and where lingering geopolitical risk still needs close watching.

Seadrill (SDRL)

Overview: Seadrill is an offshore drilling contractor that owns and operates high specification drillships, semi-submersible rigs and jackups, providing well drilling services for oil super-majors, national oil companies and independent producers across shallow and ultra deepwater fields worldwide.

Operations: Seadrill generates about US$1.4b in revenue from oil and gas contract drilling, with activity concentrated in Brazil (US$636m), the United States (US$390m), Angola (US$327m) and Norway (US$106m).

Market Cap: US$2.4b

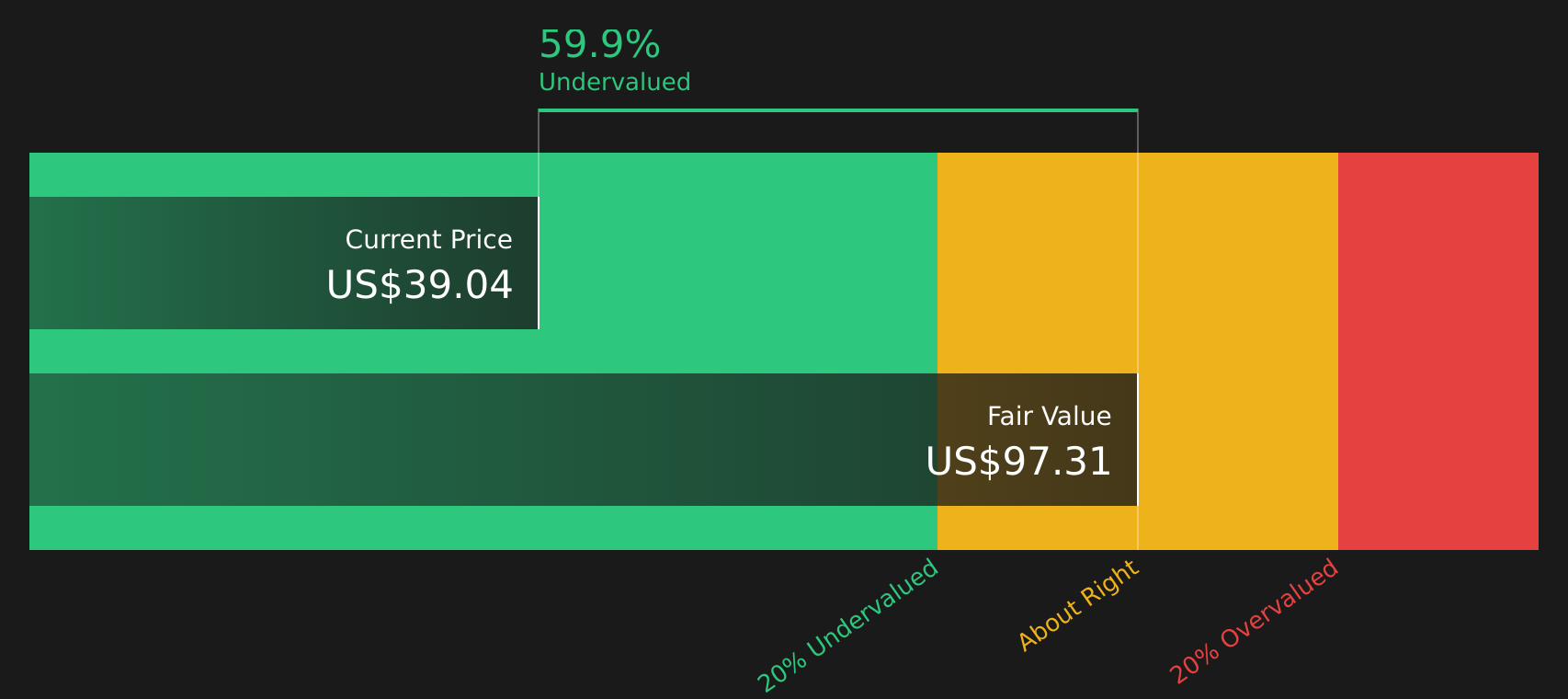

Seadrill sits at the intersection of rising deepwater activity and the reopening of the Strait of Hormuz. Together, these trends support oil project planning and logistics. The company has a focused fleet of high specification rigs, a sizeable contract backlog with long-term deals in Brazil, the U.S. Gulf and Malaysia, and management is highlighting energy security and an emerging exploration cycle as key demand drivers. At the same time, Seadrill is still loss making, faces legal and regulatory issues, relies on higher risk funding and has seen insiders selling shares, so the story is not one sided. Investors who want to understand how these positives and risks balance out, especially with a large buyback authorization and extended credit facilities in place, need to look more closely at Seadrill.

Seadrill’s buyback capacity, extended credit lines and focused deepwater fleet suggest the real story may lie in how its risk profile is changing, so unpack the 2 key rewards and 1 important warning sign

Harbour Energy (LSE:HBR)

Overview: Harbour Energy is an independent oil and gas producer headquartered in London, with a portfolio of fields and projects spanning the UK, Norway, Germany, Mexico, Argentina, North Africa and Southeast Asia, as well as early stage carbon capture and storage activities.

Operations: Harbour Energy generates most of its revenue from Norway (US$4.3b) and the UK (US$3.9b), with additional contributions from Corporate activities (US$7.0b), Germany (US$680m), Argentina (US$574m), Mexico (US$158m), North Africa (US$315m) and Southeast Asia (US$146m), partly offset by US$6.8b of adjustments and eliminations.

Market Cap: £4.0b

Harbour Energy offers exposure to a large, diversified upstream producer with meaningful exposure to Brent oil and European gas at a time when the reopening of the Strait of Hormuz reduces shipping risk for UK exports and supports smoother global flows. The Wintershall Dea assets have widened Harbour’s footprint beyond mature UK fields, and management highlights a lower cost base, investment grade credit ratings and a hedging program designed to protect a portion of cash flows through volatility. Set against that, the company is currently loss making, faces uncertainty around the UK Energy Profit Levy and relies on higher risk external funding while paying a high dividend. The key consideration for investors is how that combination of value signals and policy risk compares once you look more closely at the underlying business.

Harbour Energy now combines a widened global footprint with a high dividend and a hedging program that could be masking the real story of its cash flows, so walk through the analysis report for Harbour Energy

Flowco Holdings (FLOC)

Overview: Flowco Holdings provides production optimization and emissions management equipment and services for U.S. oil and gas producers, supplying high pressure gas lift, plunger lift and vapor recovery systems alongside software that helps operators run wells more efficiently and capture methane that would otherwise be released.

Operations: Flowco Holdings generates about US$521.4m of revenue from its Production Solutions segment and US$316.4m from Natural Gas Technologies, with eliminations of US$60.9m, largely tied to activity in the United States totaling around US$777.5m.

Market Cap: US$1.9b

Flowco Holdings sits in a position where investors looking at the Strait of Hormuz reopening may want to focus on U.S. production volumes rather than long haul shipping routes, with its gas lift and vapor recovery rentals tied to how steadily shale operators keep wells flowing. The company combines this exposure with growing methane abatement and vapor recovery offerings, which align with tightening emissions rules, plus an active capital return program that has retired 6.39% of shares and a rising dividend. Set against that, margins have narrowed from 10.5% to 5.5%, the board is relatively new and the business relies on external borrowing. To assess how those strengths and pressure points compare with the valuation and analyst expectations, investors may need to look more deeply into Flowco’s business.

Flowco Holdings sits at the crossroads of steady production volumes and tightening emissions rules, and the real intrigue is how that balance plays through its analysis report for Flowco Holdings

The three stocks in this article are just a starting point, with the full Energy and Oil Shipping Sector screener surfacing 44 more US, UK and Canadian energy and oil shipping companies that each carry their own potential catalysts and risks. Use Simply Wall St to identify, filter and analyze the specific narratives that matter to you so you can focus on the highest conviction ideas in this theme.

Take Control of Your Investment Journey

If Harbour Energy or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Beyond Energy And Shipping?

Fresh stock ideas do not stay under the radar for long, and momentum can shift before most investors react. Use these focused screeners while it matters to help identify opportunities early.

- Explore potential income streams by scanning hand picked companies in the 8 dividend fortresses that combine dividend payouts with balance sheets designed to support them.

- Look for early breakout potential across high quality businesses using the curated 44 high quality undervalued stocks, before the wider market reacts and closing price gaps change.

- Monitor where AI-related cash flows are already emerging by screening the 61 profitable AI stocks that aren't just burning cash for companies aiming to turn advanced technology into measurable earnings rather than just attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.