Seadrill Weighs Premium Sale As New Ultra Deepwater Contracts Build Backlog

Seadrill Limited SDRL | 45.63 | +2.40% |

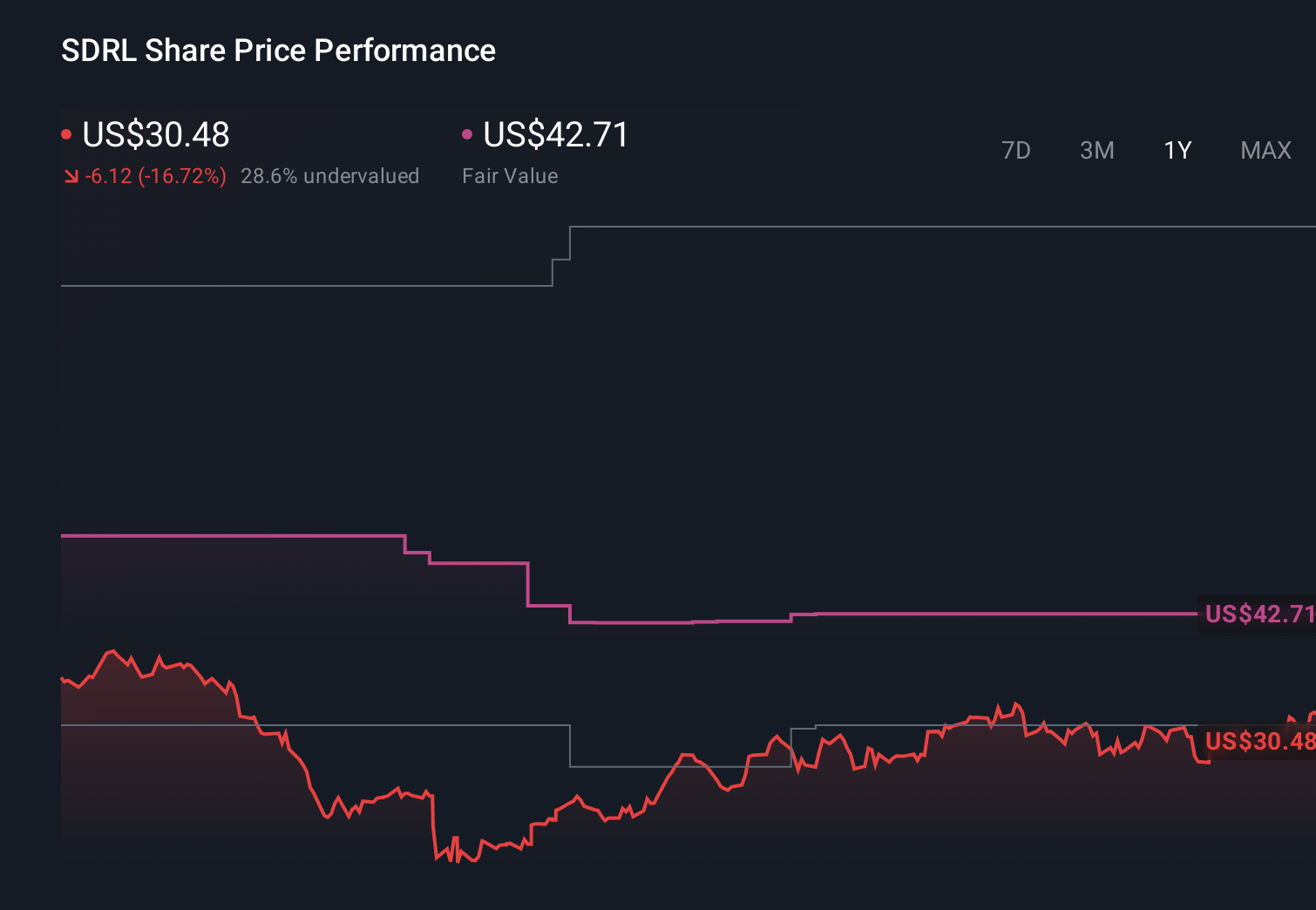

- Seadrill (NYSE:SDRL) is being discussed as a potential acquisition target, with management indicating openness to a sale at a premium.

- The company has announced several significant contract wins and extensions for its ultra deepwater fleet.

- These new contracts add to Seadrill's revenue backlog and provide increased visibility on future operations.

- The combination of M&A interest and fresh contract activity is drawing attention to Seadrill's position in the offshore drilling sector.

Seadrill, which focuses on offshore drilling through an ultra deepwater fleet, is now sitting at the intersection of new contract activity and potential corporate interest. For investors watching NYSE:SDRL, this mix of long term work commitments and talk of a possible sale at a premium brings the corporate story and the operating story together in a very direct way.

For you, the key questions are how durable these contract wins may prove to be and what a premium sale could mean for the timing and structure of any future deal. The situation is still developing, so it is worth paying attention to management commentary and any updates on contract terms, counterparties, and fleet deployment.

Stay updated on the most important news stories for Seadrill by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on Seadrill.

The new contracts for West Saturn, West Capella, West Elara and West Carina signal that Seadrill’s leadership is locking in multi-year work for its ultra-deepwater fleet at a time when potential acquirers may be assessing visible cash flows. For you, this mix of contract-specific clarity and public openness to a premium sale suggests that any buyer would be inheriting rigs with defined workstreams rather than idle capacity, which can be important when comparing Seadrill with peers such as Transocean, Valaris or Noble.

How This Fits With The Seadrill Narrative

The fresh backlog aligns with existing bullish and consensus narratives that focus on Seadrill’s high-specification fleet and focus on deepwater projects in Brazil and the U.S. Gulf. For investors who have been following those narratives, the latest deals look like another data point that management is prioritising long-term contracts and operational visibility while still keeping the door open to capital returns or a corporate transaction.

Risks And Rewards To Keep In Mind

- 🎁 Additional backlog from Equinor and other operators provides more revenue visibility across several regions.

- 🎁 Management’s stated openness to a premium sale could create a catalyst if credible bidders emerge.

- ⚠️ Greenlight Capital’s exit after a minor loss highlights that expected improvements in day rates or utilisation do not always materialise on an investor’s timeframe.

- ⚠️ Analysts have flagged legal disputes, ageing assets and margin volatility as ongoing risks that do not disappear with new contracts.

What To Watch Next

From here, the key things to watch are any concrete developments around a sale process, further contract announcements for uncommitted rigs and how Seadrill communicates capital allocation if a deal does not occur. If you want to see how different investors are interpreting these moves, you can read what others are saying through community narratives on Seadrill and compare that with your own view on the risk and reward trade off.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.