Seagate Technology Holdings (STX) Stock Could Be 22% Overvalued After The AI Storage Rally

Seagate Technology Holdings PLC STX | 0.00 |

Seagate Technology Holdings (STX) is back in focus after a broad rally in technology and AI infrastructure stocks, with investors reacting to strong earnings, upbeat analyst commentary, and rising demand from AI and cloud data centers.

Over the past year, Seagate Technology Holdings has shifted from a relatively quiet hardware stock to a high momentum AI infrastructure play, with a year to date share price return of 258.68% and a very large 1 year total shareholder return. This performance has been helped by repeated price target hikes, strong earnings, AI driven storage demand, balance sheet clean up and the easing of geopolitical risks after the US Iran peace agreement.

If Seagate’s surge has you thinking about where else AI infrastructure demand could show up, it may be worth scanning other storage and compute enablers through the 48 AI infrastructure stocks

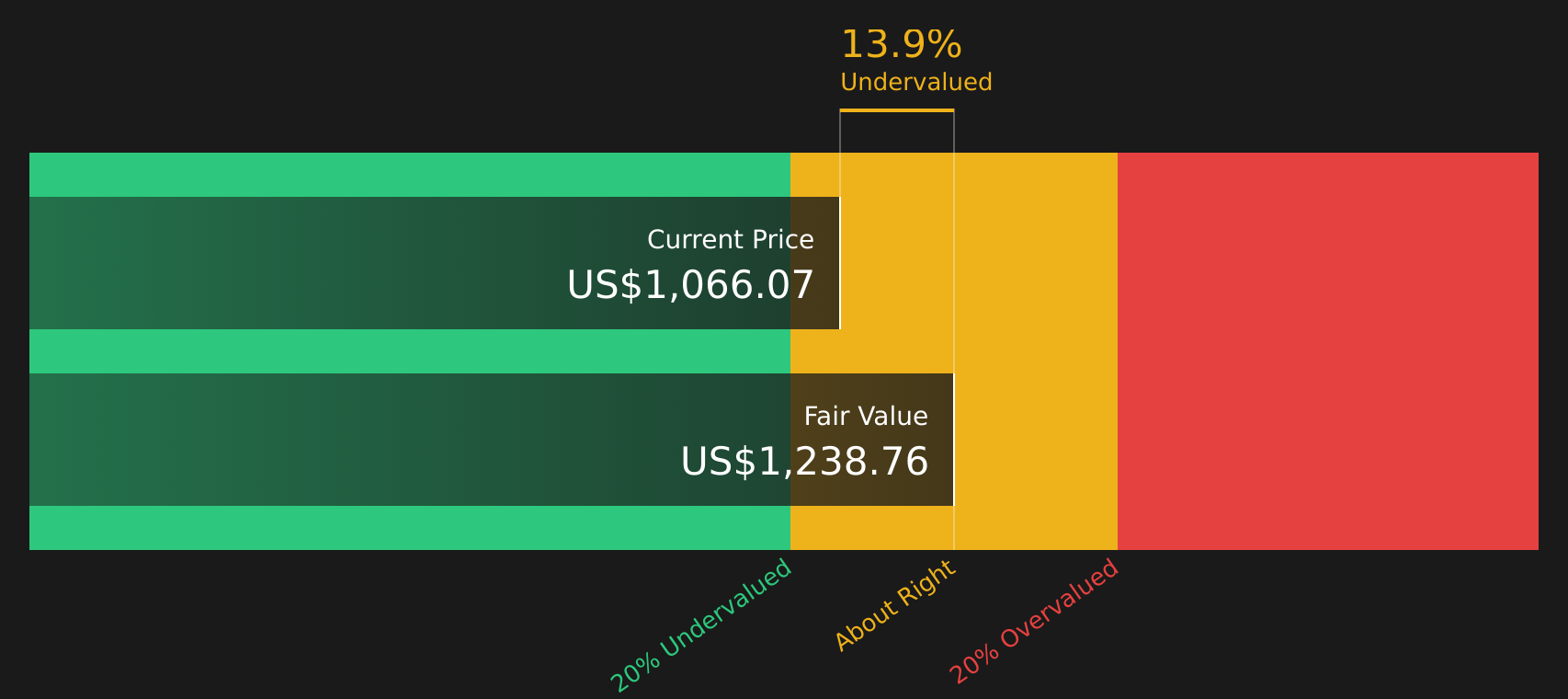

With Seagate Technology now trading above the average analyst price target and showing an intrinsic discount estimate of about 17%, the core question is simple: is there still mispricing here, or is the market already paying up for future growth?

Most Popular Narrative: 22% Overvalued

At a last close of $1,031.34 versus a narrative fair value of $847.68 based on a discount rate of 8.23%, Seagate Technology stock sits above the most widely followed valuation storyline, which leans heavily on AI driven storage demand and margin strength.

The growing demand for mass capacity storage driven by the cloud CapEx investment cycle and data center build outs for AI transformation is likely to elevate Seagate's revenue streams. This increased demand aligns with ongoing cloud infrastructure expansion, suggesting positive impacts on earnings.

Want to see the engine behind that fair value gap? The narrative leans on rapid top line expansion, sharply higher margins and a future earnings multiple more common in market leaders. Curious which specific growth and profitability paths have been baked into those long term projections?

Result: Fair Value of $847.68 (OVERVALUED)

However, Seagate Technology’s story can change quickly if trade policy shifts disrupt hyperscale demand or if SSD and QLC NAND competition starts to pressure HDD pricing and margins.

Another View: SWS DCF Versus Market Pricing

The analyst narrative frames Seagate Technology Holdings as 22% overvalued versus a fair value of $847.68, yet the SWS DCF model points in the opposite direction, with an estimated future cash flow value of $1,239.08 and the stock at $1,031.34. Is the market overshooting, or is it still leaving a gap on the table?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Seagate Technology Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Confused by the mixed signals around Seagate Technology Holdings and what really matters for the next phase of the story? Take a moment to review the underlying drivers, then pressure test the upside against the downside by checking the 3 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Seagate Technology?

If Seagate Technology’s run has sharpened your interest in new opportunities, use these focused shortlists to quickly surface stocks that better match your goals.

- Target potential mispricing by checking out 44 high quality undervalued stocks that pair resilient cash flows with quality balance sheets.

- Prioritize resilience by scanning 67 resilient stocks with low risk scores that score well on financial strength and earnings stability.

- Hunt for future standouts by reviewing the screener containing 20 high quality undiscovered gems before they attract broader market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.