Sempra (SRE) Following Five Year Low Gas Costs Faces A Fresh Valuation Test

Sempra SRE | 0.00 |

Sempra (SRE) is back in focus after subsidiary Southern California Gas Co. reported that the cost it pays for natural gas reached a five year low for March through May 2026.

The Sempra share price has moved to $93.06, with a 1 day share price return of 1.85% and a 30 day share price return of 3.92%. The 1 year total shareholder return of 27.47% and 5 year total shareholder return of 65.00% point to momentum that has built over time rather than being driven solely by the latest gas cost headlines.

If falling input costs at Sempra have you thinking about where else stable infrastructure demand could matter, this is a useful moment to review 35 power grid technology and infrastructure stocks

Sempra’s track record of double digit total returns and recent gas cost tailwinds set the stage for a key question: is the current US$93.06 share price leaving upside on the table or already reflecting future growth?

Most Popular Narrative: 10.1% Undervalued

With Sempra last closing at $93.06 against a narrative fair value of $103.50, the widely followed view frames the stock as trading at a discount while hinging on specific growth and margin expectations.

Analysts are assuming Sempra's revenue will grow by 1.8% annually over the next 3 years. Analysts assume that profit margins will increase from 14.2% today to 28.3% in 3 years time.

Want to see what underpins that big margin step up and earnings trajectory Sempra is being priced against? The narrative leans on measured revenue growth, rising profitability and a future earnings multiple that must compress from today’s level while still supporting that fair value target.

Result: Fair Value of $103.50 (UNDERVALUED)

However, Sempra's heavy spending on regulated utilities and growing LNG exposure could face tougher rules or weaker demand, which would quickly challenge that view of the stock as underpriced.

Another View on Sempra: Expensive on Earnings

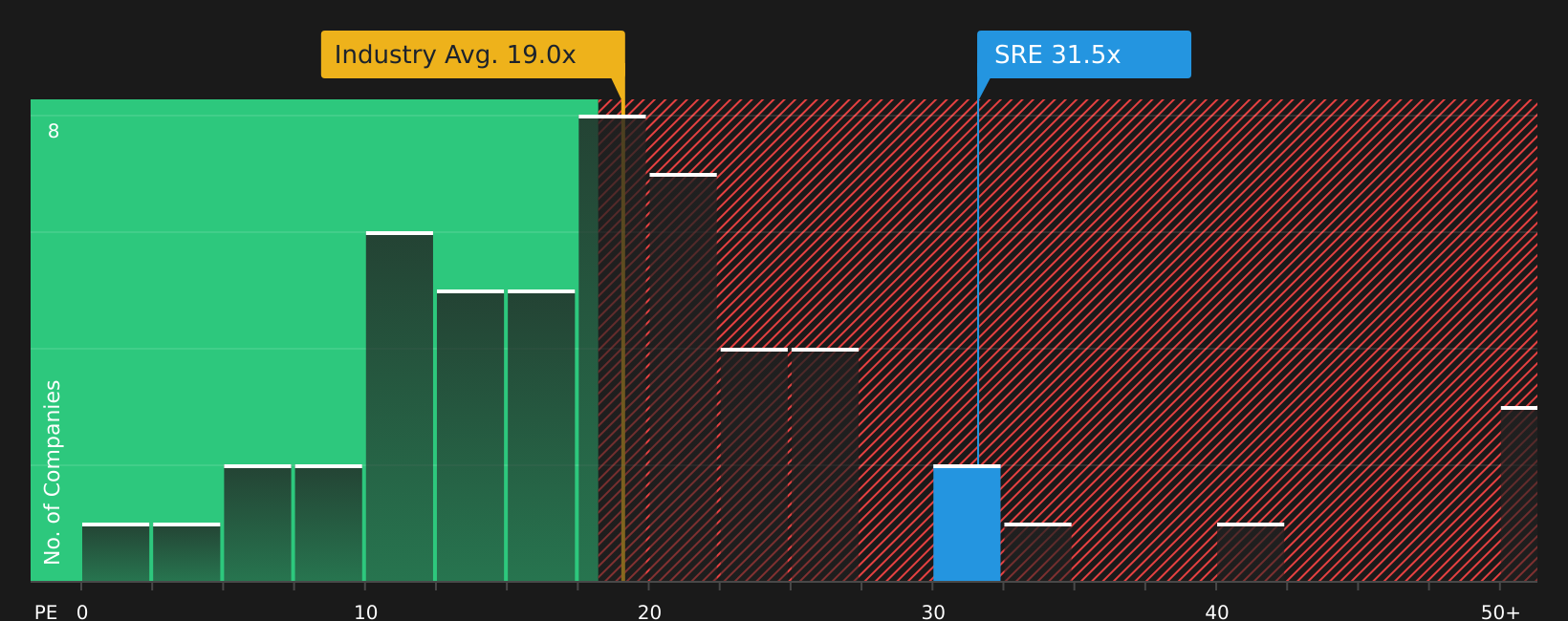

The popular Sempra narrative leans on a fair value of $103.50, yet the current P/E of 31.6x sits well above the Integrated Utilities industry at 19.2x, the peer average at 20.5x, and a fair ratio of 27x, which points to a rich earnings multiple rather than a clear bargain.

If the market eventually gravitates closer to that 27x fair ratio, today’s gap implies more valuation risk than upside purely on earnings. The real question is whether Sempra’s future growth and margins fully justify paying this premium.

Next Steps

Given the mixed signals around Sempra, this is a good moment to review the full picture for yourself and act with intent. You can start with 1 key reward and 4 important warning signs.

Looking for more investment ideas beyond Sempra?

If Sempra has your attention, do not stop there. Broadening your watchlist now can help you spot opportunities before the crowd catches on.

- Target reliable income streams by reviewing 7 dividend fortresses that could complement a utilities holding.

- Zero in on quality at a discount with the 43 high quality undervalued stocks and see which stocks align with your return and risk expectations.

- Prioritize resilience by checking the 75 resilient stocks with low risk scores so you are not the last to respond when conditions change.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.