Sempra (SRE) Stock May Be Pricey After First LNG Cargo Milestone

Sempra SRE | 0.00 |

Sempra stock has delivered a 67.0% return over the past 5 years, yet current valuation checks suggest the shares are priced more like a premium utility than a clear bargain. With the stock around US$94.62 and recent returns still positive, the question is whether ongoing projects and growth expectations justify what looks like a full valuation.

- A 67.0% return over 5 years signals that long term shareholders have already captured a solid gain, which can reduce the margin of safety if growth expectations ease.

- New developments such as the first LNG cargo from the ECA LNG Phase 1 project and high rooftop solar adoption at SDG&E may support long term earnings power, while execution risks on major infrastructure projects and changing customer behavior remain a potential drag on valuation.

- Sempra screens as overvalued on the earnings based checks, and scoring 0 of 6 suggests the stock does not currently stand out as a value opportunity on broader metrics.

The stock's next move may depend on whether Sempra's current operations and project pipeline can do enough to make today's pricing look reasonable rather than stretched.

Has Sempra Run Too Far on Earnings?

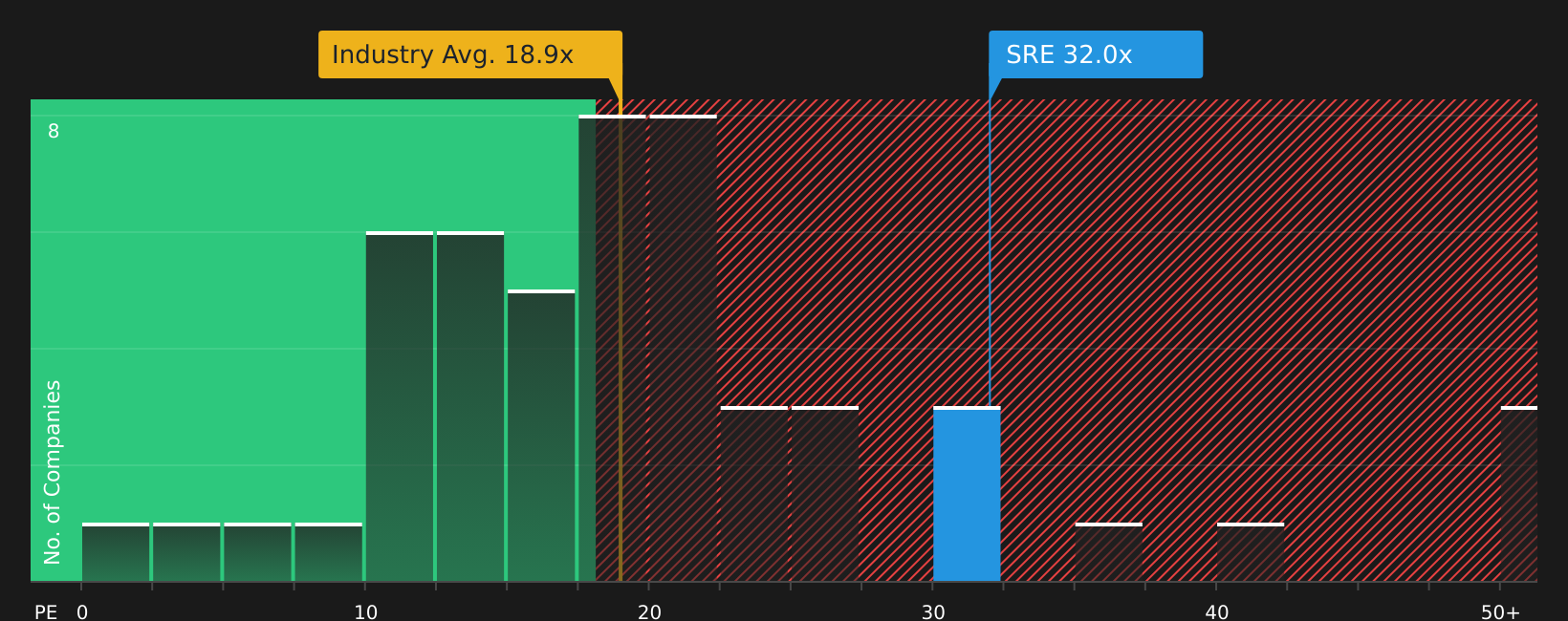

The P/E ratio suits Sempra because earnings remain a primary anchor for how investors value an integrated utility. Sempra currently trades on a P/E of about 32.1x, which sits well above both the Integrated Utilities industry average of 18.9x and the broader peer average of 20.1x. That pricing suggests investors are willing to pay a clear premium for each dollar of Sempra earnings compared with many other utilities.

A tailored fair P/E ratio for Sempra, which takes into account its profile versus similar businesses, is estimated at 27.1x. With the stock trading above that level, the gap indicates Sempra screens as overvalued on this earnings based yardstick rather than simply reflecting sector norms. Despite progress at projects such as ECA LNG Phase 1 supporting interest in the story, the current earnings multiple still prices Sempra ahead of what this framework implies.

On the P/E multiple alone, Sempra stock currently looks overvalued relative to both its tailored fair ratio and utility peers.

The Sempra Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Sempra pick up where the valuation puzzle leaves off by spelling out which paths for Sempra's future earnings, margins and growth would make the stock worth materially more or less than today's price, all in one place on the Community page. Instead of stopping at a single ratio or model output, they clarify the future that figure relies on so you can see what needs to play out and monitor whether it does.

If you have a number driven view on whether Sempra's ECA LNG Phase 1 project and SDG&E's high rooftop solar adoption ultimately make today's valuation look fair or stretched, share a Narrative on Sempra so the community can see your thesis and track how it holds up as new results and project milestones arrive.

Do you think there's more to the story for Sempra? Head over to our Community to see what others are saying!

The Bottom Line

For Sempra, the current picture is that the stock screens as overvalued on earnings-based checks, with the P/E sitting above both peers and its tailored fair ratio. That does not rule out further upside, but it means expectations are already demanding and leave less room for disappointment. The key question from here is whether Sempra's project execution and long-term earnings profile can live up to, and sustain, that premium multiple rather than forcing a reset in how the stock is priced.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.