SentinelOne (S): Evaluating Valuation Following Elpha Secure Partnership and Strategic Leadership Shift

SentinelOne, Inc. Class A S | 13.33 | +0.15% |

SentinelOne (S) is making headlines as it teams up with Elpha Secure, rolling out an all-in-one cyber protection and insurance solution designed for small and midsize businesses. This partnership is catching investor attention because it fuses cybersecurity with insurance into a single streamlined offering.

SentinelOne’s announcement with Elpha Secure comes as the stock navigates a stretch of fading momentum, with a year-to-date share price return of -23.57% and a one-year total shareholder return of -32.91%. Despite fresh product launches and new leadership, the stock has struggled to gain lasting traction, reflecting recent pressure on cybersecurity names along with broader tech sector jitters.

If the latest move has you thinking about what’s next in the industry, now is an ideal moment to discover new opportunities using our tech and AI stock screener: See the full list for free.

With shares trading at a notable discount to analyst price targets, the question is whether SentinelOne is being overlooked by the market or if future growth expectations are already fully reflected in today’s stock price.

Most Popular Narrative: 26.6% Undervalued

SentinelOne closed at $17.25, notably below the current consensus fair value estimate of $23.50. The narrative driving this valuation highlights key catalysts that could accelerate the company’s growth far beyond what the market currently reflects.

SentinelOne's robust innovation in AI-driven, autonomous security, supported by substantial enterprise adoption of Purple AI and the AI-native SIEM platform, strongly positions the company to capture growing budgets as cyber threats become more sophisticated. This is likely to drive sustained revenue growth and improve gross margins as their differentiated offerings enable premium pricing.

Curious why the fair value towers above the current stock price? The secret lies in the explosive growth drivers and ambitious assumptions woven deep into the narrative. These bold projections could shake up Wall Street’s expectations. Want to see what’s fueling this valuation and what might push the price even higher? The answers may surprise you.

Result: Fair Value of $23.50 (UNDERVALUED)

However, ongoing reliance on large technology partners and increased regulatory scrutiny could create new hurdles for SentinelOne as it pursues its ambitious growth narrative.

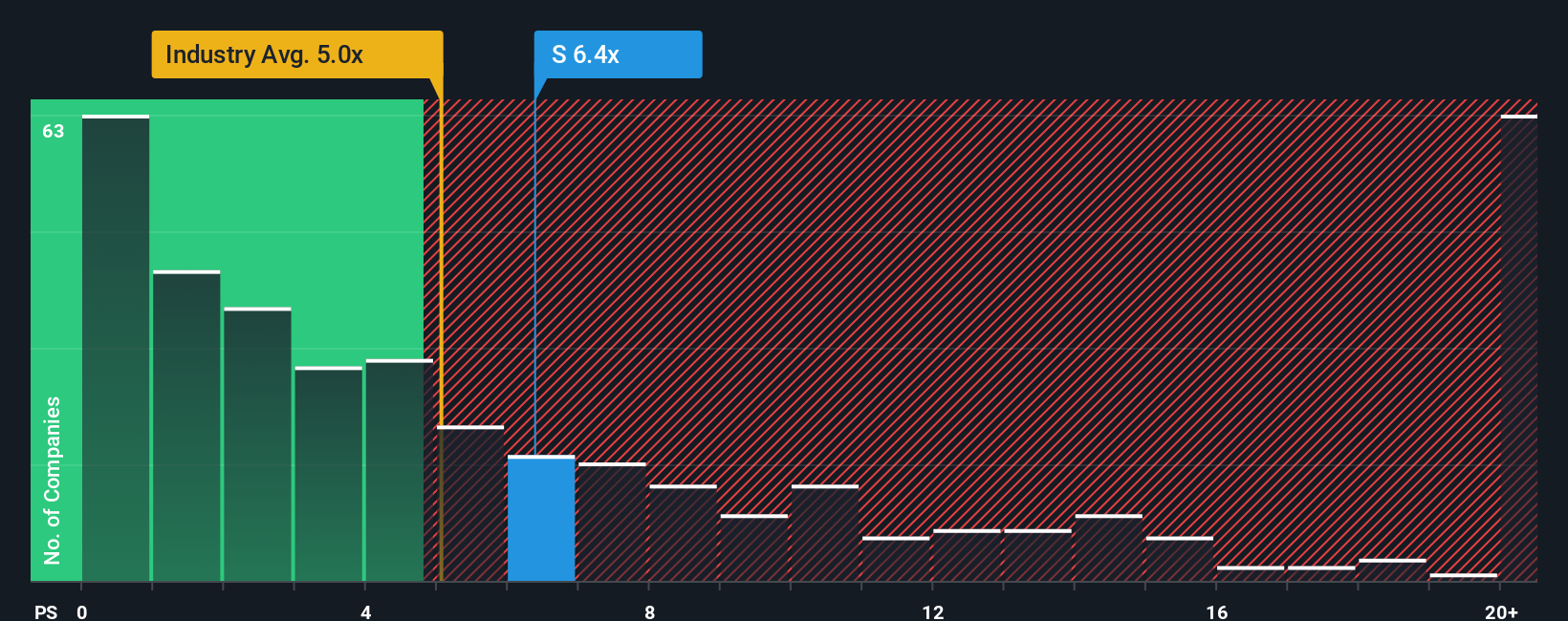

Another View: What Do Valuation Ratios Say?

Looking beyond narrative-driven fair value estimates, SentinelOne’s price-to-sales ratio stands at 6.4x. This is higher than the US Software industry average of 5x, which signals that investors are paying a premium compared to peers. However, it is still below the peer group average of 10.1x and under the fair ratio of 7.2x. This may suggest the market could move upwards. Does this gap represent a hidden chance or elevated risk for prospective investors?

Build Your Own SentinelOne Narrative

If you have a different take or want to dig into the numbers yourself, you can craft a personalized story in just minutes. Do it your way

A great starting point for your SentinelOne research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t let your next big opportunity slip past you. Make your next move count by checking stocks screened for proven growth, value, and future trends.

- Fuel your portfolio with game-changers by tapping into these 24 AI penny stocks that are transforming entire industries using artificial intelligence innovation.

- Secure steady income opportunities when you browse these 19 dividend stocks with yields > 3% with reliable dividend yields above 3%.

- Lead the charge into finance’s next frontier with these 79 cryptocurrency and blockchain stocks at the cutting edge of blockchain and digital currency progress.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.