ServiceNow (NOW) Valuation Check After AI Sell Off And Growing Focus On Long Term Platform Potential

ServiceNow, Inc. NOW | 102.00 | -1.96% |

ServiceNow (NOW) is back in focus after a sharp software sector sell-off tied to AI disruption worries, as investors weigh its AI-driven growth story, resilient cash generation, and high-profile partnerships with Anthropic, OpenAI, and Microsoft.

After the sharp sector-wide sell-off, ServiceNow’s recent 1-day and 7-day share price returns of 3.67% and 6.29% sit against a 30-day share price decline of 20.45% and a year-to-date share price return of 27.38% in the red. The 1-year total shareholder return of 45.73% lower contrasts with a 3-year total shareholder return of 21.96%, suggesting that short-term momentum has weakened even though longer-term holders still sit on gains overall.

If AI driven software volatility has your watchlist looking lopsided, it might be worth widening your search with our screener of 34 AI infrastructure stocks as potential next candidates to research.

With ServiceNow trading well below recent highs despite annual revenue and net income growth, and with AI products gaining traction alongside positive analyst targets, the key question is simple: is this reset a genuine opportunity, or is the market already pricing in that future growth?

Most Popular Narrative: 52.6% Undervalued

ServiceNow’s most followed narrative puts fair value at $225.84 per share against a last close of $107.08, so the model sees substantial upside baked into its cash flow outlook.

ServiceNow's focus on AI platform and business transformation is gaining momentum, which is expected to drive future revenue growth as demand for AI-driven solutions increases. The acquisition of companies like Moveworks and Logik.ai can enhance ServiceNow’s offerings, potentially improving net margins by driving efficiencies and offering more integrated solutions.

Curious how that growth story translates into a fair value more than double today’s share price? Revenue expansion, margin assumptions and a rich future earnings multiple sit at the core of this narrative. The exact mix of those drivers might surprise you.

Result: Fair Value of $225.84 (UNDERVALUED)

However, those upside assumptions could quickly look stretched if AI execution stumbles or if government and security related deals slow more than investors currently expect.

Another Angle On Valuation

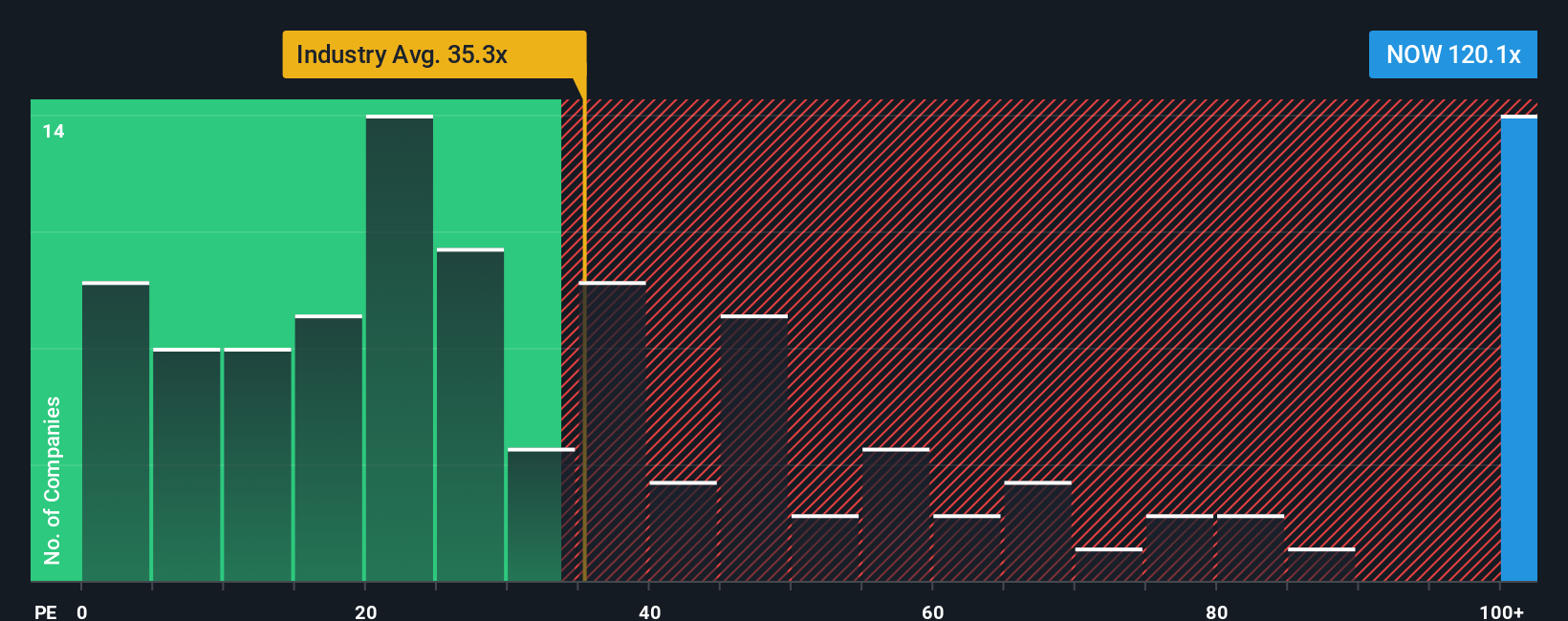

That 52.6% discount to fair value is based on projected cash flows, but the current P/E of 64.1x tells a different story. It is far above the US Software industry at 26.7x, peers at 46.6x, and even the fair ratio of 41.5x. This suggests valuation risk if growth expectations cool. Which signal do you put more weight on?

Build Your Own ServiceNow Narrative

If this version of the story does not quite fit your view, or you prefer to test the assumptions yourself, you can build a custom thesis in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding ServiceNow.

Looking for more investment ideas?

If ServiceNow has sharpened your thinking, do not stop here. Give yourself options by scanning a wider field of opportunities while this story plays out.

- Hunt for potential bargains by checking companies our screener tags as 53 high quality undervalued stocks, so you are not relying on just one high expectation story.

- Prioritise staying power by reviewing businesses in the solid balance sheet and fundamentals stocks screener (44 results), where financial resilience can matter as much as headline growth.

- Get ahead of the crowd by scanning our screener containing 23 high quality undiscovered gems, so you see ideas others might only notice much later.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.