ServiceNow (NOW) Valuation Check After Recent Share Price Volatility

ServiceNow, Inc. NOW | 102.00 | -1.96% |

ServiceNow (NOW) is back on many investors’ screens after a sharp pullback, with the stock showing a negative move over the past month and past 3 months that contrasts with its longer term total returns.

At a share price of US$129.62, ServiceNow’s 30 day share price return of 16.15% and 90 day share price return of 30.66% contrast with a 1 year total shareholder return of 43.33%. The 3 year and 5 year total shareholder returns of 36.78% and 12.39% respectively place the recent pullback in a longer term context and indicate that sentiment around its growth and risk profile has shifted over time.

If recent volatility in ServiceNow has you reassessing your tech exposure, it could be a good moment to scan other high growth tech and AI stocks for fresh ideas.

With ServiceNow trading at US$129.62 and sitting at what looks like a 35% intrinsic discount, the key question is whether the recent share price slide has created genuine value or if the market is simply recalibrating to future growth that was already priced in.

Most Popular Narrative: 42.6% Undervalued

At $129.62, the most followed narrative sets ServiceNow’s fair value at about $225.84. This points to a sizeable gap between price and modeled worth.

The analysts have a consensus price target of $1142.588 for ServiceNow based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $1300.0, and the most bearish reporting a price target of just $734.0.

Want to see what kind of revenue build, margin profile and future earnings multiple could anchor a much lower fair value than that earlier target? The full narrative lays out the cash flow path, the profit assumptions and the required return that all have to line up for that $225.84 figure to make sense.

Result: Fair Value of $225.84 (UNDERVALUED)

However, this depends on effective AI execution and successful integration of acquisitions such as Armis and Veza, while any pullback in U.S. federal spending could affect revenue and margins.

Another View: Rich P/E Puts the Discount in Question

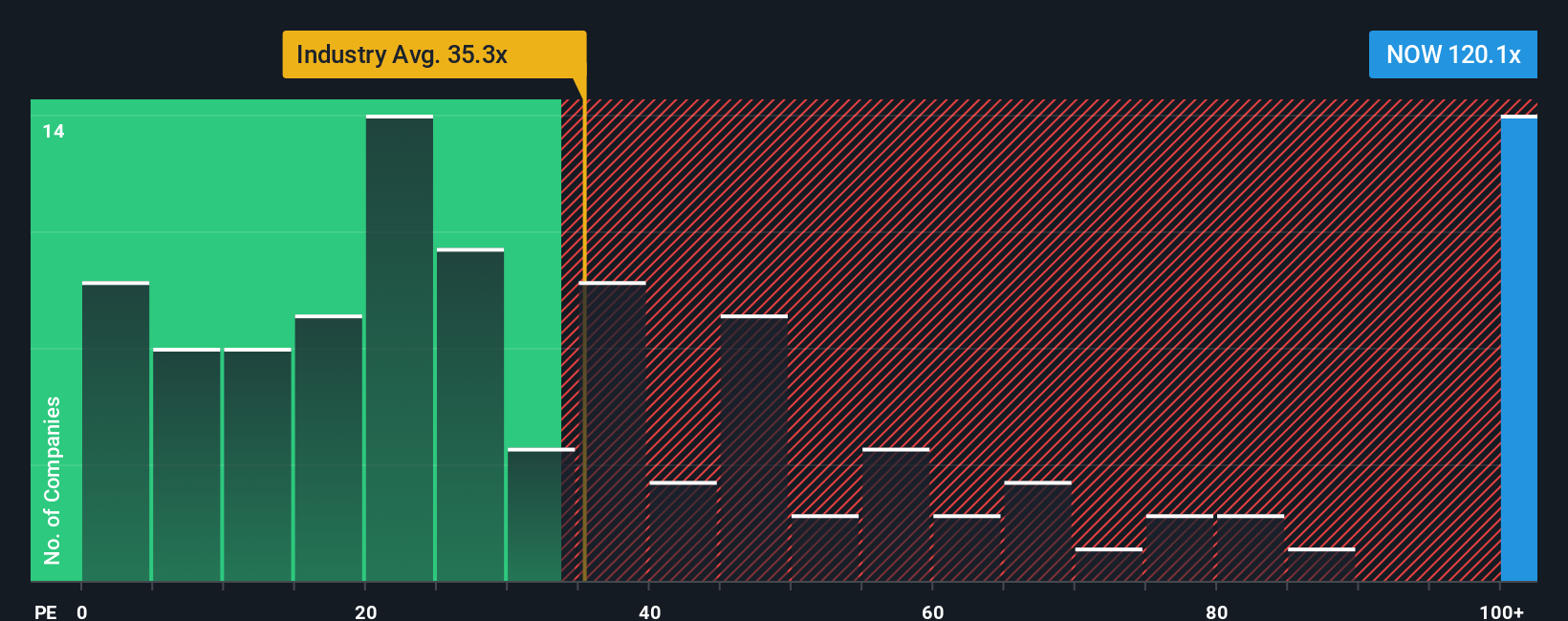

While the narrative and our cash flow work suggest ServiceNow looks cheap, the current P/E of 77.7x is far higher than the US Software industry at 30.1x, the peer average at 49.6x and even the fair ratio of 44.3x. Could that premium limit how much of the supposed discount actually closes?

Build Your Own ServiceNow Narrative

If you look at these numbers and reach a different conclusion or prefer to test your own assumptions, you can build a custom thesis in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding ServiceNow.

Looking for more investment ideas?

If ServiceNow has sharpened your interest in tech, this is a great time to widen your radar, compare different angles and pressure test where your capital goes next.

- Spot potential bargains early by scanning these 880 undervalued stocks based on cash flows that may be trading below what their cash flows suggest they could be worth.

- Ride the AI wave thoughtfully by checking out these 24 AI penny stocks that tie real revenue models to artificial intelligence themes.

- Capture income ideas by reviewing these 14 dividend stocks with yields > 3% that pair higher yields with underlying business fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.