Sharplink Holdings (SBET) Valuation Check After Recent Share Price Volatility

SharpLink Gaming SBET | 7.14 | +6.57% |

Sharplink stock: context after recent moves

Sharplink (SBET) has drawn extra attention after a sharp one day move, with the share price closing at $6.07 and recent returns over the week, month and past 3 months all in negative territory.

The recent 1 day share price return of 14.27% decline follows a 30 day share price return of 41.30% decline and a 1 year total shareholder return of 7.49% decline, which points to fading momentum as investors reassess both growth potential and risk.

If Sharplink’s swings have you rethinking concentration in a single name, it could be a moment to broaden your watchlist with our 19 cryptocurrency and blockchain stocks screener. This is a way to spot other Ethereum and blockchain related opportunities.

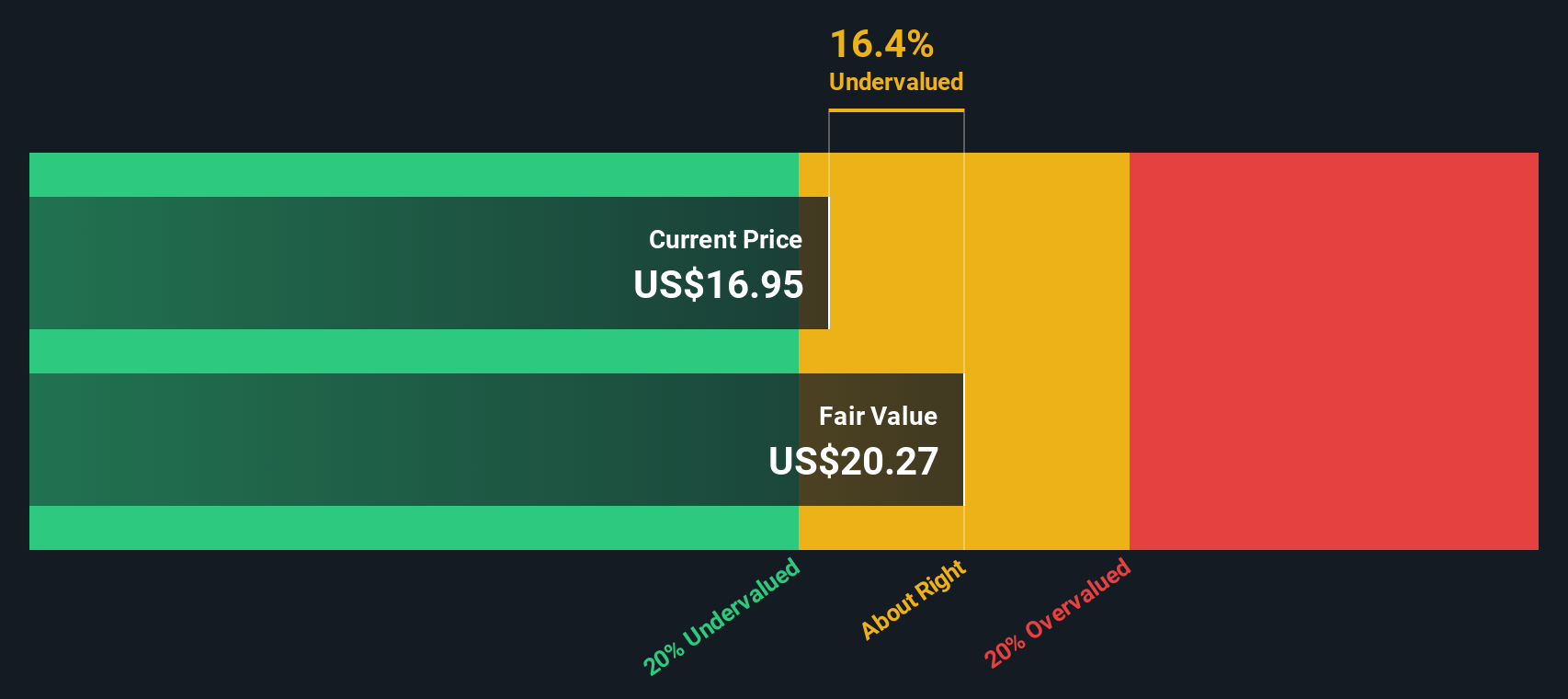

With the stock trading at $6.07 against an analyst price target of $24.00 and screens flagging a potential intrinsic discount of 57%, you have to ask: is Sharplink undervalued here, or is the market already pricing in future growth?

Preferred Price-to-Book Multiple of 0.4x: Is it justified?

On simple valuation checks, Sharplink looks inexpensive, with a P/B of 0.4x at a last close of $6.07 compared to much richer peer benchmarks.

The P/B ratio compares the market value of the company to its book value, effectively showing how much you are paying for each dollar of net assets on the balance sheet. For Sharplink, that 0.4x mark sits well below both the US Hospitality sector average of 2.5x and a broader peer average of 4.6x.

That kind of gap suggests the market is currently pricing Sharplink’s Ethereum treasury and affiliate marketing business at a sizeable discount to asset value, even though forecasts point to revenue growth of 71.4% per year and earnings growth of 90.23% per year, with expectations that the company becomes profitable within 3 years. At the same time, the shares have been volatile, returns over 1 year have lagged both the US market and the Hospitality industry, and existing holders have experienced substantial dilution over the past year.

Against this backdrop, the SWS DCF model estimates future cash flow value at $14.24 per share while the stock trades at $6.07. This lines up with other screens that flag Sharplink as trading 57.4% below an intrinsic value estimate and substantially below an analyst price target of $24.00. Taken together, these signals indicate a wide valuation gap that depends on whether the market ultimately credits the forecast growth path and a relatively new management team and board.

Result: Price-to-Book of 0.4x (UNDERVALUED)

However, you still have to weigh ongoing share price volatility with multi period declines and the risk that expected revenue and earnings growth or Ethereum adoption do not play out.

Another View: What if the gap is justified?

Even after our DCF model points to a fair value of $14.24 per share versus the current $6.07, the market is signaling caution around volatility, recent dilution and an unprofitable business that depends on Ethereum and affiliate marketing. Is this a mispriced opening, or a warning that the cash flow story is still unproven?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Sharplink for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Sharplink Narrative

If this view does not quite match your own thinking, or you prefer to work directly with the numbers yourself, you can quickly build a personalised thesis using Do it your way.

A great starting point for your Sharplink research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are only focused on Sharplink, you could miss other opportunities that better fit your style, so widen your search using the Simply Wall St screener.

- Spot potential value candidates early by checking out our 55 high quality undervalued stocks that meet strict quality and pricing filters in one place.

- Strengthen your downside protection by reviewing companies in our 81 resilient stocks with low risk scores that score well on stability and risk checks.

- Get ahead of the crowd by scanning our screener containing 25 high quality undiscovered gems packed with lesser known names that pass fundamental screens.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.