Shell Stock And 2 UK Energy Picks For Rising Power Price Volatility

Coda Octopus Group, Inc. CODA | 0.00 |

UK energy bills are set to climb again, with Ofgem lifting the price cap by 13% from July and household energy debt reaching about £4.8b. At the same time, wholesale prices are being pushed by conflict in Iran and fresh political debate over how electricity should be priced and taxed. Together, these pressures can reshape margins for producers, networks, and retail suppliers, creating both potential opportunities and risks for investors. This article picks out 3 UK Energy Market Volatility Impact Stocks from the screener, two that could benefit from the current backdrop and one where the pressure looks more challenging.

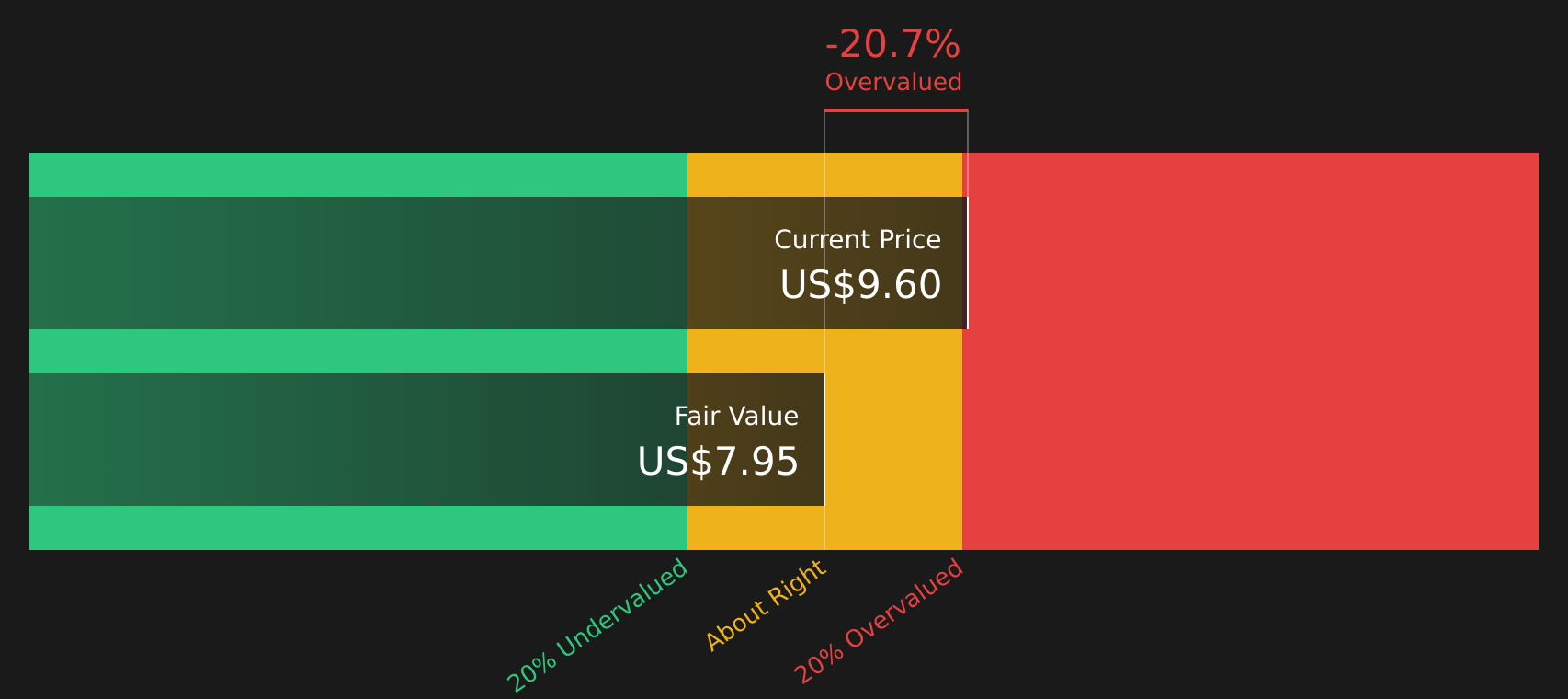

Coda Octopus Group (CODA)

Overview: Coda Octopus Group develops and rents underwater 3D imaging, sonar, and mapping systems, along with acoustic sensors and defense engineering solutions, that support activities such as offshore construction, renewables, oil and gas, subsea defense, and marine survey work across multiple regions.

Operations: The company generates most of its revenue from its Marine Technology Business products at about US$17.8m, with additional contributions from its Defense Engineering Services at about US$9.1m, its Acoustic Sensors and Materials Business at about US$6.0m, and a small corporate segment and intercompany eliminations.

Market Cap: US$108.3m

Investors looking at Coda Octopus Group are being asked to weigh attractive underwater defense and energy infrastructure exposure against some uncomfortable questions. The company is benefiting from high quality earnings, rising net margins at 17.7% and long serving management, while the DAVD and Echoscope technologies are gaining traction in defense and subsea work. Yet revenue growth expectations are only in the low teens, return on equity is just 8%, and the price sits above a Simply Wall St cash flow estimate, so much of the potential appears already priced in. In addition, there is policy risk around defense budgets, higher operating costs, and a funding structure entirely reliant on external borrowings, which can make the stock appear more fragile than the headlines suggest.

Coda Octopus Group’s high quality earnings and rising margins can distract from a valuation that already prices in a lot of hope. Before assuming the story holds, read the DCF valuation analysis for Coda Octopus Group

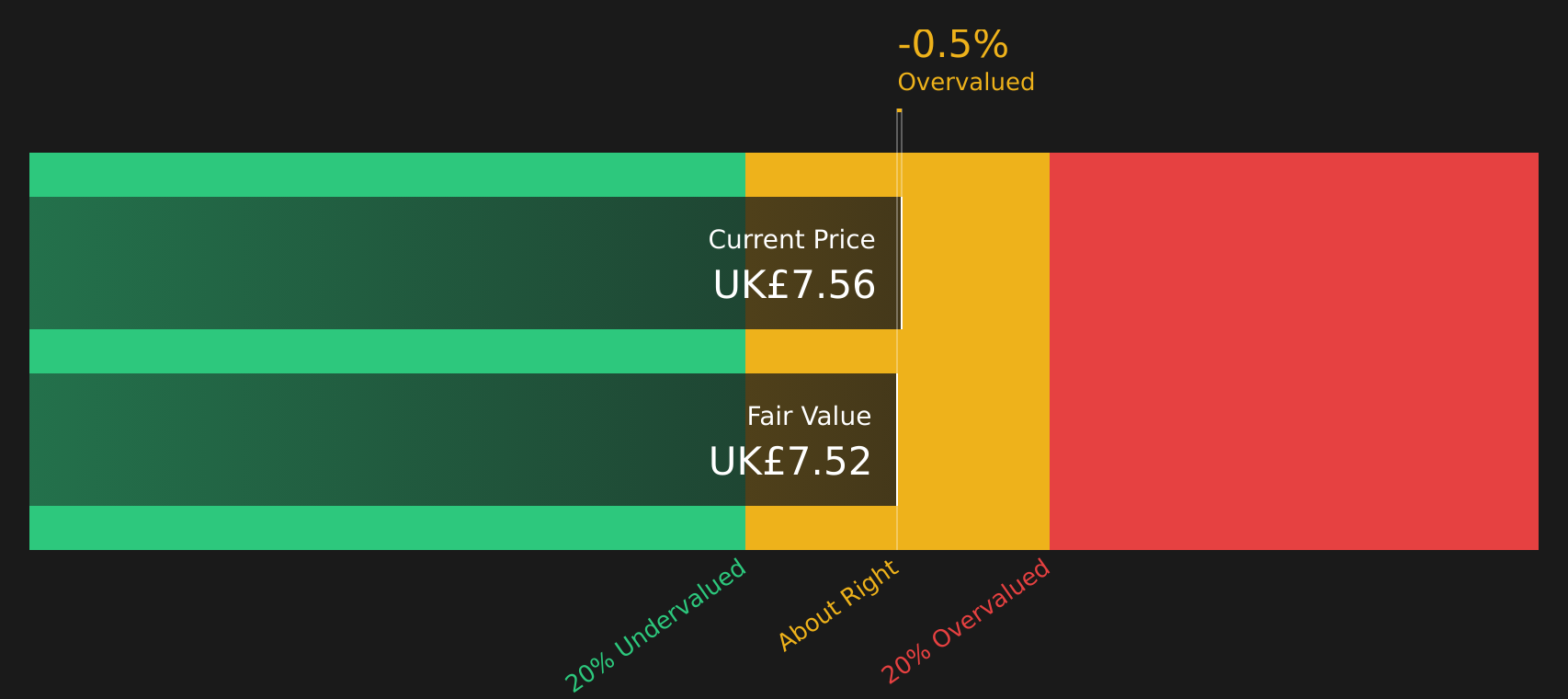

Shell (LSE:SHEL)

Overview: Shell is a global energy and petrochemical company that produces and trades oil, gas, liquefied natural gas, chemicals and refined products, while also supplying electricity, biofuels and low carbon energy solutions to households, businesses and transport customers worldwide.

Operations: Shell generates most of its revenue from Marketing at about US$123.4b and Chemicals and Products at about US$111.4b, with additional contributions from Integrated Gas at about US$47.6b, Upstream at about US$40.5b, Renewables and Energy Solutions at about US$40.1b and a small Corporate segment, partly offset by about US$95.7b of inter segment eliminations.

Market Cap: £161.5b

Shell stands out in the UK Energy Market Volatility Impact Stocks screener because it combines a large LNG and gas portfolio that can benefit from higher wholesale prices with a broad marketing and power presence that keeps it close to end customers. The company is described as trading well below some fair value estimates, with a relatively low P/E and positive earnings momentum. Transcripts also highlight how its trading and LNG optimization businesses can turn price swings into profit opportunities. At the same time, an unstable dividend history, reliance on external borrowing and only moderate forecast earnings growth mean investors still need to weigh funding and income risk carefully before assuming Shell is a straightforward beneficiary of rising energy bills and geopolitical tension.

Shell’s low P/E and discussion of trading well below some fair value estimates suggest the market may be missing something in its LNG and power story, so review the analysis report for Shell

Drax Group (LSE:DRX)

Overview: Drax Group is a UK focused power company that generates renewable electricity from biomass and hydro, produces and sells wood and waste derived pellets, and supplies power and system support services to business customers and the national grid.

Operations: Drax Group generates most of its revenue from Biomass Generation at about £4.4b and Energy Solutions at about £2.6b, with smaller contributions from Pellet Production at about £903.4m and Flexible Generation at about £171.5m, partly offset by £2.8b of intra group eliminations.

Market Cap: £2.5b

Drax Group sits at the crossroads of three powerful themes for UK investors: higher power prices, tighter security of supply, and the push for cleaner, dispatchable energy. Its biomass and flexible generation assets, backed by government support mechanisms and long term capacity contracts, can turn wholesale price spikes into steadier cash flows, even as Ofgem’s cap rise and geopolitical tension keep electricity markets tight. At the same time, thin profit margins, a large recent one off loss and reliance on external borrowing mean the stock is not without risk, especially if regulatory rules on biomass or pellet demand shift. The key issue is whether Drax’s position in carbon removals and grid support can justify that risk when you look more closely at its earnings quality and valuation.

Drax’s biomass and grid support story looks like it could be more than a simple power price play, so check how the 2 key rewards and 3 important warning signs might reframe the risk reward balance hiding behind those thin margins

Take Control of Your Investment Journey

If Shell or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Energy?

New ideas move fast and the best entry points often arrive quietly. Before the next breakout flies, scan these fresh stock shortlists while it matters and get in early.

- Spot under the radar strength and pursue companies with resilient earnings profiles using our curated list of solid balance sheet and fundamentals (48 results) before the crowd starts chasing stability.

- Ride structural momentum in automation and target businesses reshaping factories and logistics with the hand picked 29 robotics and automation stocks while valuations can still reflect early adoption.

- Position ahead of infrastructure upgrades and sift through the carefully selected 35 power grid technology and infrastructure stocks as grid technology spending shifts, so you are not caught reacting after prices move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.