Shopify (SHOP) Stock After 28% Slide This Year Is Valuation Now Reasonable

Shopify, Inc. Class A SHOP | 0.00 |

How Shopify Stock’s Valuation Looks After Recent Moves

Shopify stock often raises the same question for investors: is the current share price offering good value, or are you paying too much for future expectations?

Over shorter timeframes, the picture has been mixed, with the stock up 2.5% over the past week and 12.9% over the past month, while the year-to-date return is a decline of 28.0%. Looking back further, the stock shows a 6.3% gain over one year, 76.2% over three years and a 24.9% decline over five years, which gives important context for any valuation discussion.

Recent news coverage around Shopify has continued to focus on its role as a major e-commerce platform and how investors are weighing that against shifts in broader market sentiment toward growth-oriented software stocks. This context helps frame why the share price has seen periods of strength as well as pullbacks, and why valuation remains a central talking point for many shareholders.

On Simply Wall St’s valuation framework, Shopify currently records a value score of 1 out of 6. This means it screens as undervalued on only one of six checks and calls for a closer look at how different valuation methods line up, before turning to an approach at the end of this article that can help you put those metrics into a broader narrative. Shopify scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Shopify scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Shopify Discounted Cash Flow (DCF) Analysis

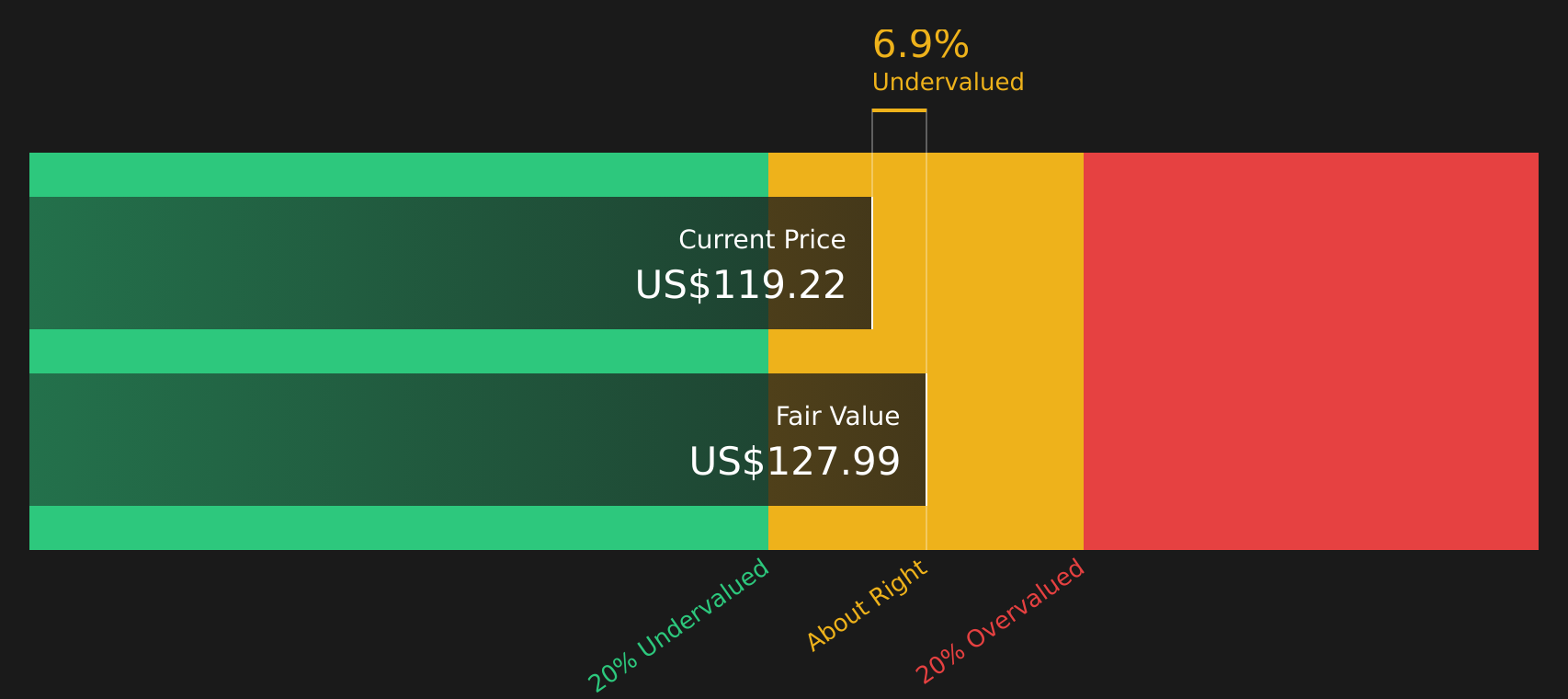

A Discounted Cash Flow model estimates what a stock might be worth by taking projected future cash flows, then discounting them back to today’s value. For Shopify, the model used is a 2 Stage Free Cash Flow to Equity approach, which focuses on cash that could theoretically be available to shareholders after necessary expenses and reinvestment.

Shopify’s latest twelve month free cash flow stands at about $2.1b. Based on analyst inputs for the next few years and further projections extended by Simply Wall St, free cash flow is estimated to reach about $7.1b by 2030. Across the 2026 to 2035 period, the model uses a series of projected annual cash flows, each discounted back to today using a required rate of return to reflect risk and the time value of money.

When these cash flows are added together, the DCF model arrives at an estimated intrinsic value of $118.89 per share. Compared with the current share price, this implies Shopify stock trades at a 4.8% discount, which is a relatively small gap and suggests the market price is close to the model’s estimate.

Result: ABOUT RIGHT

Shopify is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Shopify Price vs Earnings

For profitable companies like Shopify, the P/E ratio is a commonly used way to think about value, because it links what you pay for the stock to the earnings the business is currently generating. In general, higher expected earnings growth and lower perceived risk can support a higher “normal” or “fair” P/E, while slower growth and higher risk often line up with a lower multiple.

Shopify currently trades on a P/E of 110.59x. This compares with an average P/E of 18.51x for the broader IT industry and about 58.11x for its peer group, so the stock is priced at a much higher multiple than both of these benchmarks.

Simply Wall St’s Fair Ratio for Shopify is 53.03x. This is a proprietary estimate of what a more appropriate P/E might be, taking into account factors such as earnings growth, industry, profit margins, market cap and risk, rather than relying only on broad industry or peer comparisons. Because the current P/E of 110.59x is significantly above the Fair Ratio, the shares screen as expensive on this metric.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Shopify Narrative

Earlier it was mentioned that there is an even better way to understand valuation, so on Simply Wall St’s Community page you can use Narratives. Here you and other investors can turn a view on Shopify into a clear story that links drivers like social commerce, AI tools, partnerships and risks to a set of explicit forecasts for revenue, earnings, margins and a Fair Value. That Fair Value can then be compared with the current price and will update automatically when new news or earnings arrive. One investor might build a bullish Shopify Narrative with a Fair Value around US$197.82 based on faster revenue growth and higher earnings power, while another might build a more cautious Narrative with a Fair Value near US$105.00. You can see both side by side to decide which story you think fits the stock best.

For Shopify however we will make it really easy for you with previews of two leading Shopify Narratives:

Fair Value: US$186.64

Implied discount to this Fair Value: about 39.3% below the narrative estimate based on the latest close.

Revenue growth assumption: 12%

- Focuses on social commerce as a large potential market, with a heavy emphasis on mobile driven shopping.

- Highlights AI Store Builder and Sidekick as tools that reduce friction for new merchants and support engagement.

- Points to partnerships with DHL and Amazon as ways to lower setup and fulfillment hurdles for merchants while also flagging tariff policy, consumer confidence and competition as key risks.

Fair Value: US$105.00

Implied premium to this Fair Value: about 7.8% above the narrative estimate based on the latest close.

Revenue growth assumption: 20.98%

- Frames Shopify stock through a more cautious lens that leans on the lower end of analyst price targets.

- Emphasizes risks around e commerce saturation, higher operating and regulatory costs, and potential pressure on margins as features converge across platforms.

- Assumes revenue and earnings increases out to 2029 but with a lower future P/E multiple, arguing that multiple compression and execution risk could limit returns even if the business continues to grow.

Between these two narratives, the gap in Fair Values and assumptions gives you a structured way to decide which story feels closer to how you see Shopify, and how comfortable you are with the trade off between growth expectations, risk and the current share price.

Do you think there's more to the story for Shopify? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.