Shopify (SHOP) Stock Looks Near Fair Value While Earnings Sit Above Fair Value

Shopify, Inc. Class A SHOP | 0.00 |

Shopify’s valuation picture has become more finely balanced, with the stock up 94.1% over the past three years, while the Discounted Cash Flow (DCF) intrinsic value estimate now lines up close to the current share price and earnings multiples screen as expensive.

- Shopify’s 94.1% three year return signals that a large part of the story is already reflected in the share price, so fresh upside may need stronger fundamentals to support it.

- Expectations around continued revenue growth supported by Shopify’s expanding AI and e-commerce ecosystem can support current pricing, while questions about profitability, cash flow margins, and regulatory risks may affect how much investors are willing to pay.

- With Shopify scoring 1 out of 6 on our valuation checks, the stock currently appears expensive rather than standing out as a clear bargain.

The stock’s next move may depend on whether Shopify’s future cash generation can justify paying a premium to what the intrinsic value and broader checks currently indicate.

Where Does Shopify Sit on Cash Flow?

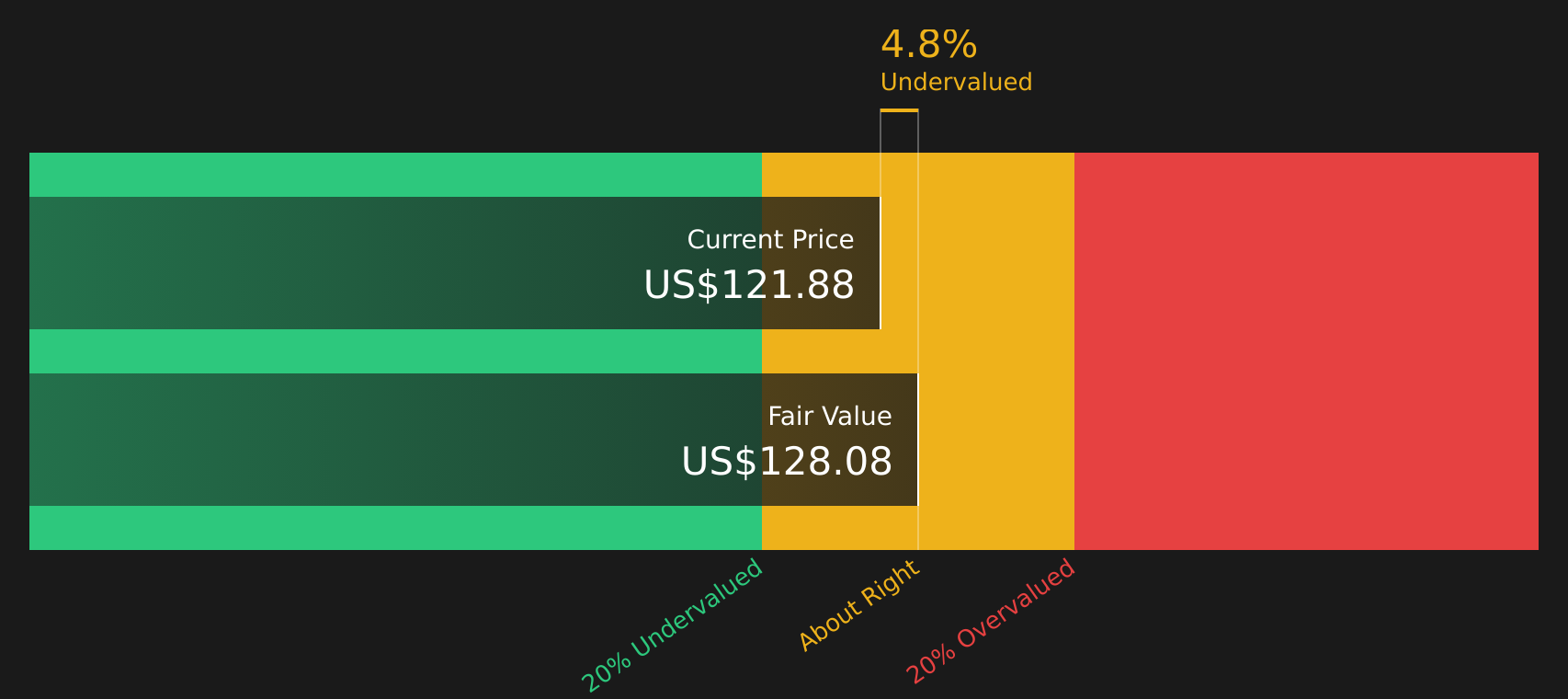

The Discounted Cash Flow (DCF) model values Shopify by projecting future cash the business can return to shareholders and discounting it back to today. On the latest twelve month numbers, Shopify generated about $2.1b of free cash flow in $, and the model assumes those cash flows continue growing rather than shrinking, consistent with the 2 Stage Free Cash Flow to Equity setup.

On that basis, the DCF model points to an estimated intrinsic value of about $128 per share. This sits close to the current market price and implies the stock screens as roughly fairly valued rather than clearly cheap or expensive on cash flows alone. Shopify’s recent share price drop after mixed Q4 earnings and lower free cash flow margin guidance helps explain why the market is no longer pricing in a large premium to this intrinsic value estimate.

Overall, the DCF workup suggests Shopify currently looks about fairly valued on its projected cash generation.

Shopify is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Is Shopify Getting Expensive on Earnings?

P/E is a useful lens for Shopify because earnings are now a meaningful driver of how the stock is priced. Shopify currently trades on a P/E of about 117.3x, compared with an IT industry average of around 18.6x and a peer average near 57.0x. This means investors are paying a much higher price for each dollar of earnings than for many other listed software and internet stocks.

The tailored fair P/E for Shopify, which factors in its growth profile, margins, scale and risk, is estimated at about 50.8x. That is less than half of the current multiple, which indicates that the stock price reflects a relatively generous earnings outlook compared with what this framework would typically suggest for a company with similar characteristics.

On the P/E multiple, Shopify stock currently appears clearly overvalued compared with both its fair ratio and wider industry benchmarks.

The Shopify Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Shopify pick up where the valuation work leaves off by spelling out the specific growth, margin and earnings paths that would need to play out for the stock to be worth materially more or less than its current price, and they sit within the company’s Community page. Instead of giving just a single number from a ratio or model, they describe the future that number relies on so you can watch how Shopify’s actual progress aligns with those assumptions over time.

Community views on Shopify are split between those who see a growing commerce infrastructure story and those focused on cost, competition, and a full valuation.

Bull case: 52% undervalued

"By expanding its role behind the scenes, Shopify increases switching costs, as merchants are less likely to leave a platform that handles payments, inventory, analytics, and customer identity."

Bear case: 14% overvalued

"The global e-commerce market is facing signs of saturation and regulatory scrutiny, including compliance with emerging data privacy and cross-border regulations, which will drive up operating costs."

Do you think there's more to the story for Shopify? Head over to our Community to see what others are saying!

The Bottom Line

For Shopify, the Discounted Cash Flow (DCF) work suggests the current share price is broadly in line with intrinsic value, while the earnings multiples point to an overvalued stock compared with peers and a tailored fair P/E. That split mainly comes down to cash flow expectations versus what the market is willing to pay for each dollar of earnings today. With broader valuation checks screening weak, the key question from here is whether Shopify can deliver the revenue growth and margin profile that would make its premium multiple feel justified rather than stretched.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.