Should Afrezza Pediatric Approval And New Data Shift MannKind’s (MNKD) Technosphere Platform Investment Narrative?

MannKind Corporation MNKD | 0.00 |

- MannKind recently reported past milestones including FDA approval of Afrezza for children aged 6 and older and new clinical and real‑world data on Afrezza and FUROSCIX presented at the 2026 American Diabetes Association Scientific Sessions.

- The breadth of data, from pediatric safety and treatment satisfaction to gestational diabetes, automated insulin delivery use, lung cancer risk, and FUROSCIX hospitalization outcomes, highlights how MannKind is testing its Technosphere platform across multiple high‑need patient groups.

- We’ll now consider how MannKind’s progress with Afrezza’s pediatric expansion and new IPF inhaled therapy data could reshape its investment narrative.

Find 48 companies with promising cash flow potential yet trading below their fair value.

MannKind Investment Narrative Recap

To own MannKind, you have to believe its Technosphere platform can convert Afrezza’s broader label and emerging inhaled lung programs into a sustainable, diversified revenue base. The key near term catalyst is Afrezza’s pediatric launch and uptake; the new ADA data and IPF trial progress both speak to that platform story but do not, by themselves, resolve the current risks around slow Afrezza adoption and continued operating losses.

Among the recent updates, the advancement of nintedanib DPI into the global Phase 2 INFLO-2 trial stands out. It directly ties Technosphere to idiopathic pulmonary fibrosis, one of MannKind’s targeted high-need lung indications. While the primary focus of INFLO-2 is safety and dose finding, successful progress here would be important alongside Afrezza’s pediatric expansion as investors weigh whether MannKind can reduce its dependence on a narrow set of commercial and royalty streams.

Yet, while Afrezza’s pediatric label expansion looks encouraging, investors should also be aware that persistent adult adoption hurdles could still...

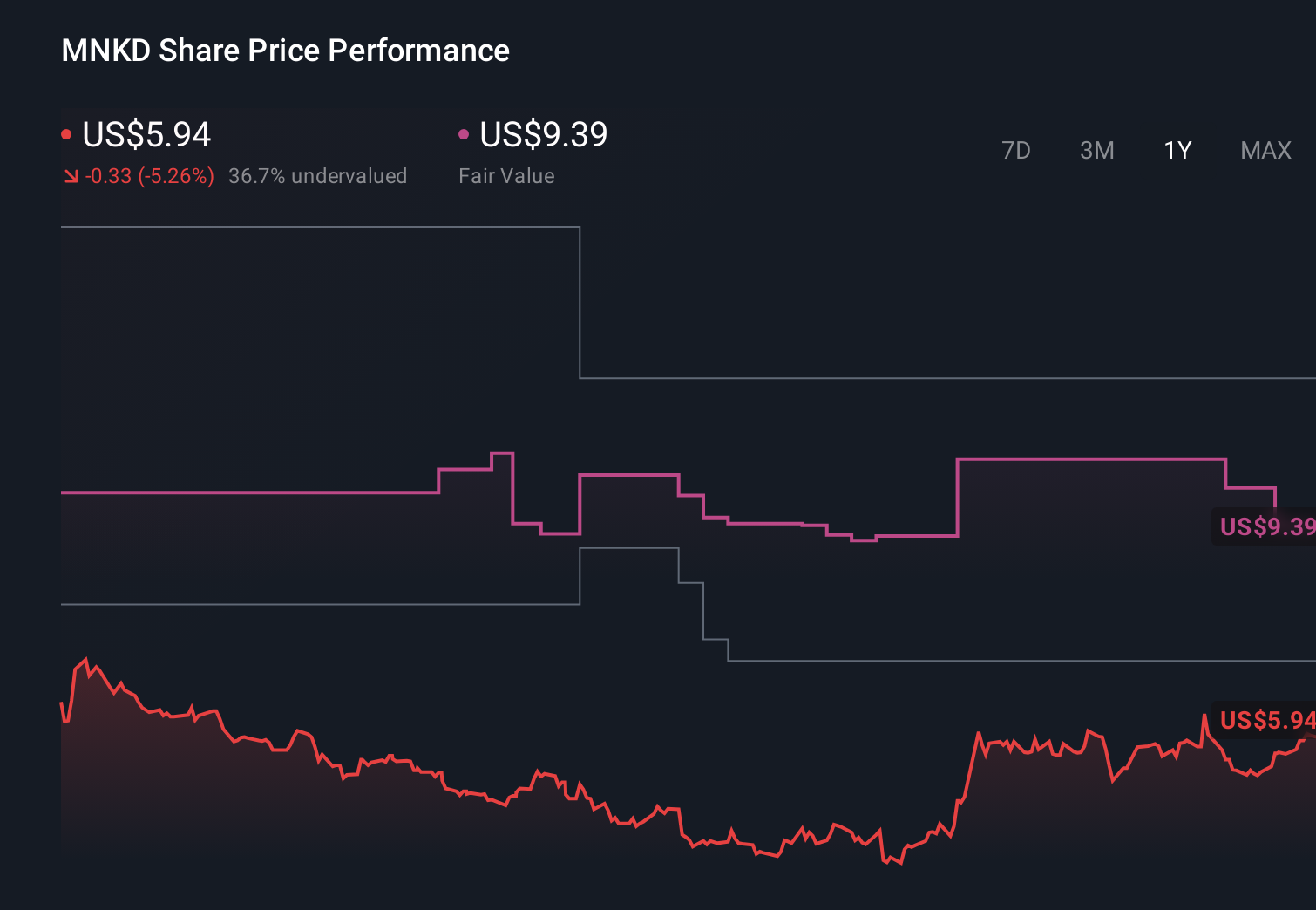

MannKind's narrative projects $544.8 million revenue and $62.0 million earnings by 2029. This requires 16.0% yearly revenue growth and about a $56 million earnings increase from $5.9 million today.

Uncover how MannKind's forecasts yield a $7.17 fair value, a 111% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected revenue to reach about US$650,000,000 and earnings near US$170,000,000, so this new Afrezza and IPF data could either reinforce that upbeat view or challenge it, depending on how you weigh adoption risks and the possibility that inhaled therapies remain a niche choice.

Explore 3 other fair value estimates on MannKind - why the stock might be worth just $4.83!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MannKind research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free MannKind research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MannKind's overall financial health at a glance.

No Opportunity In MannKind?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 13 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.