Should Alnylam’s Billion‑Dollar Quarter and Return to Profitability Require Action From Alnylam Pharmaceuticals (ALNY) Investors?

Alnylam Pharmaceuticals, Inc ALNY | 0.00 |

- In the first quarter of 2026, Alnylam Pharmaceuticals reported revenue of US$1,167.18 million, turning a US$18.25 million net loss a year earlier into a US$205.99 million net profit and delivering positive earnings per share from continuing operations.

- The quarter marked Alnylam’s first time surpassing US$1 billion in combined net product revenue, with its TTR franchise and AMVUTTRA uptake underpinning both sustained profitability and reiterated full-year guidance alongside progress in late-stage RNAi programs.

- Next, we’ll examine how this earnings beat and first-time billion‑dollar product quarter could reshape Alnylam’s investment narrative and risk profile.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Alnylam Pharmaceuticals Investment Narrative Recap

To own Alnylam, you need to believe its RNAi platform and TTR franchise can support durable, profitable growth while the company broadens beyond a single key revenue engine. The Q1 2026 earnings beat and first billion dollar product quarter reinforce near term confidence in the TTR-driven story, but they do not remove the biggest current risk: revenue concentration in AMVUTTRA and the wider TTR portfolio amid evolving pricing and competitive pressures.

The most relevant recent announcement is management’s reiteration of 2026 TTR product sales guidance of US$4.4–US$4.7 billion alongside expanding the TRITON-CM Phase III trial for nucresiran. This combination of sustained guidance and pipeline investment ties the latest earnings surprise directly to two central catalysts: continued AMVUTTRA uptake and successful late stage development of next generation TTR therapies that could eventually diversify or deepen the franchise.

Yet beneath the strong quarter, investors still need to be aware of the risk that concentrated TTR reliance could become a problem if...

Alnylam Pharmaceuticals' narrative projects $7.0 billion revenue and $1.9 billion earnings by 2028. This requires 41.8% yearly revenue growth and about a $2.2 billion earnings increase from -$319.1 million today.

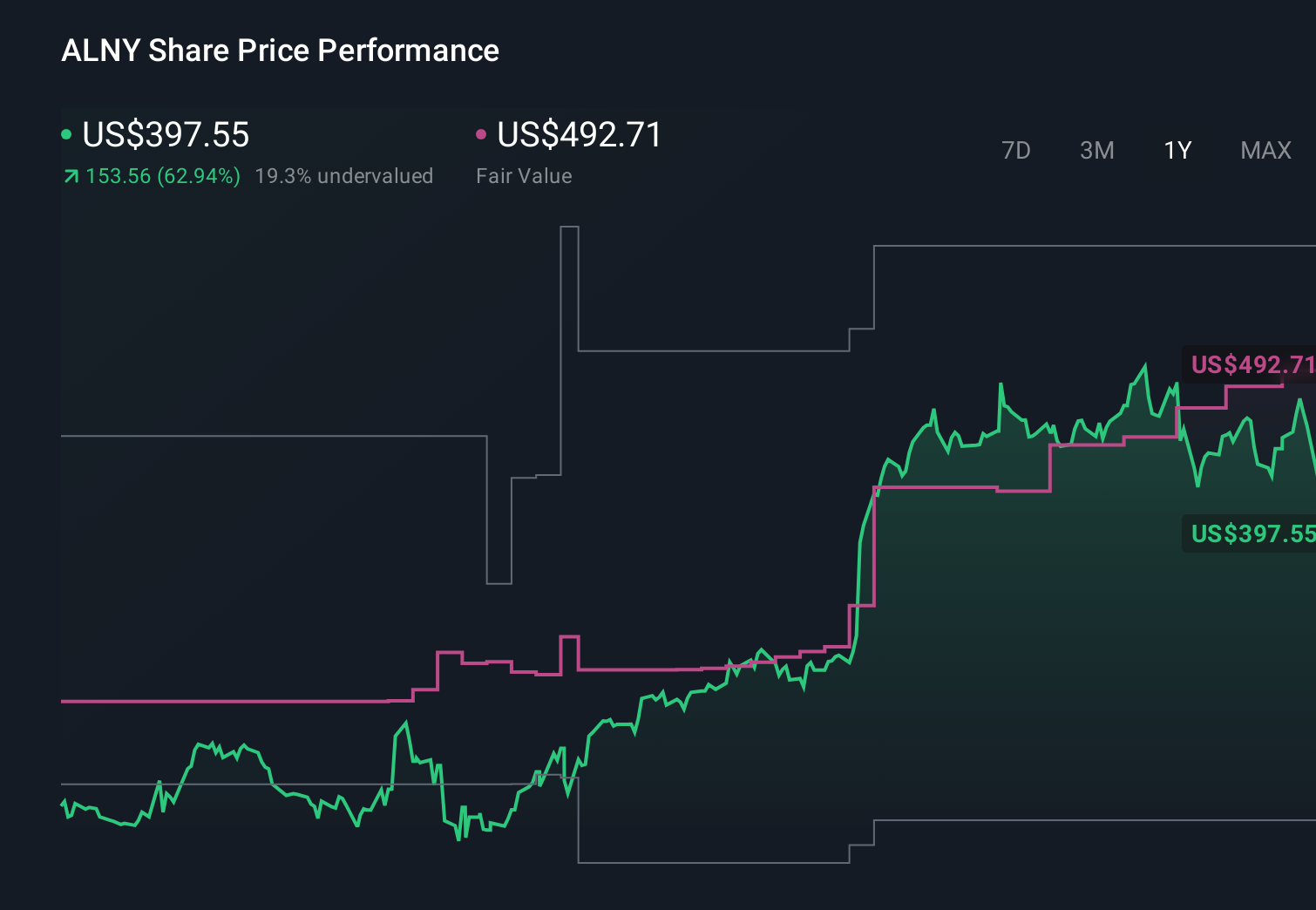

Uncover how Alnylam Pharmaceuticals' forecasts yield a $491.92 fair value, a 66% upside to its current price.

Exploring Other Perspectives

Before this earnings beat, the most bullish analysts were already modeling about US$11.5 billion of revenue and US$3.4 billion of earnings by 2029, which is far more optimistic than consensus. If you are weighing that view against concerns about long term TTR concentration risk, this quarter’s results might strengthen or weaken your conviction, so it is worth comparing how both narratives could evolve as more data and guidance come through.

Explore 5 other fair value estimates on Alnylam Pharmaceuticals - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Alnylam Pharmaceuticals research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Alnylam Pharmaceuticals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Alnylam Pharmaceuticals' overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- Capitalize on the AI infrastructure supercycle with our selection of the 37 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.