Should AZZ’s (AZZ) Debt Refinancing and Lower Interest Expenses Prompt a Closer Look From Investors?

AZZ Inc. AZZ | 0.00 |

- Earlier this month, AZZ Inc. secured a three-year US$150 million accounts receivable securitization facility with Wells Fargo, using proceeds to refinance existing debt at lower interest rates and entering into several associated agreements to facilitate the transaction.

- This move is anticipated to reduce AZZ’s interest expenses and improve financial flexibility, further strengthening its balance sheet position alongside recent operational gains.

- Next, we'll examine how AZZ's lower debt costs through refinancing could strengthen the company's earnings growth narrative and capital allocation plans.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

AZZ Investment Narrative Recap

To be an AZZ shareholder, you need to believe in the company’s ability to drive sustained earnings and cash flow growth by expanding capacity and improving operational efficiency, while managing debt prudently. The new US$150 million receivables facility aligns with the short-term catalyst of reducing interest costs and boosting financial flexibility, while execution risk from new facility ramp-ups and acquisition integration remains the most important challenge to monitor. The refinancing meaningfully improves balance sheet strength, but does not fully address all underlying risks.

Of the recent announcements, AZZ’s robust first-quarter 2026 earnings result, in which net income surged to US$170.91 million on higher margins, directly complements the debt refinancing news. This earnings momentum underscores why improved cash flow and lower interest costs are seen as positive near-term drivers for capital allocation plans, particularly as the St. Louis plant ramps and acquisition efforts continue.

However, despite these gains, investors should also be aware that unforeseen execution challenges at new facilities such as the Washington site could...

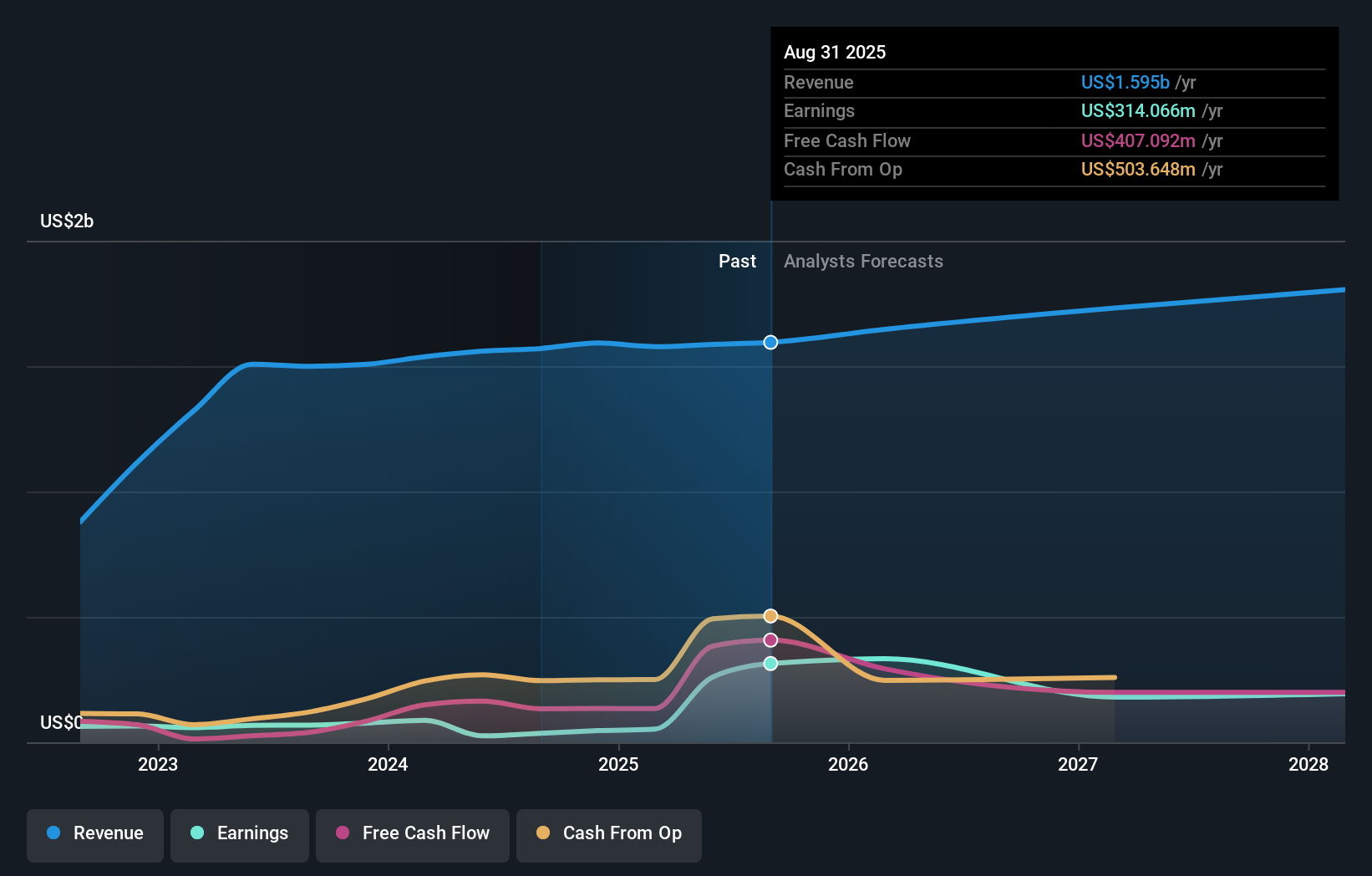

AZZ's narrative projects $1.9 billion in revenue and $264.3 million in earnings by 2028. This requires 5.7% yearly revenue growth and a $211.9 million increase in earnings from the current $52.4 million.

Uncover how AZZ's forecasts yield a $119.75 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Fair value estimates from the Simply Wall St Community range from US$103.97 to US$119.75, reflecting just two differing views on AZZ’s worth. In contrast, upcoming plant ramp-ups present both opportunities for revenue expansion and risks around operational efficiency that could influence future outcomes.

Explore 2 other fair value estimates on AZZ - why the stock might be worth 8% less than the current price!

Build Your Own AZZ Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your AZZ research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free AZZ research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate AZZ's overall financial health at a glance.

No Opportunity In AZZ?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.