Should BAC’s New Senior Notes and Capital Returns Shape a New View of Bank of America’s Risk Profile?

Bank of America Corp BAC | 0.00 |

- In recent weeks, Bank of America Corporation has issued a series of new senior unsecured notes across multiple maturities, maintained its regular common and preferred dividends, and completed its 2026 annual meeting where shareholders re-elected all directors and approved management proposals.

- Alongside strong recent earnings, raised net interest income guidance and continued capital returns, this steady funding activity and governance continuity underline how Bank of America is positioning its balance sheet and franchise for ongoing growth and client demand.

- Next, we will examine how this combination of stronger earnings guidance and continued capital returns could influence Bank of America’s investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

Bank of America Investment Narrative Recap

To own Bank of America, you need to be comfortable with a large, diversified bank whose earnings are closely tied to interest income, credit quality and deposit costs. The latest wave of senior note issuances and reaffirmed dividends appears to modestly reinforce its funding flexibility and capital return capacity, but does not materially change the near term catalyst around net interest income guidance or the key risk from potential credit and funding pressure if economic conditions weaken.

The recent $3 billion fixed to floating rate notes due 2037 are most relevant here, because they sit alongside strong Q1 2026 earnings, higher net interest income guidance of 6% to 8% and ongoing share repurchases. Together, this highlights how Bank of America is aligning its capital and funding profile with its focus on digital investment, lending growth and balance sheet management, which remain central to the current investment narrative.

But investors should also be aware that rising competition for deposits could eventually pressure funding costs and net interest income if...

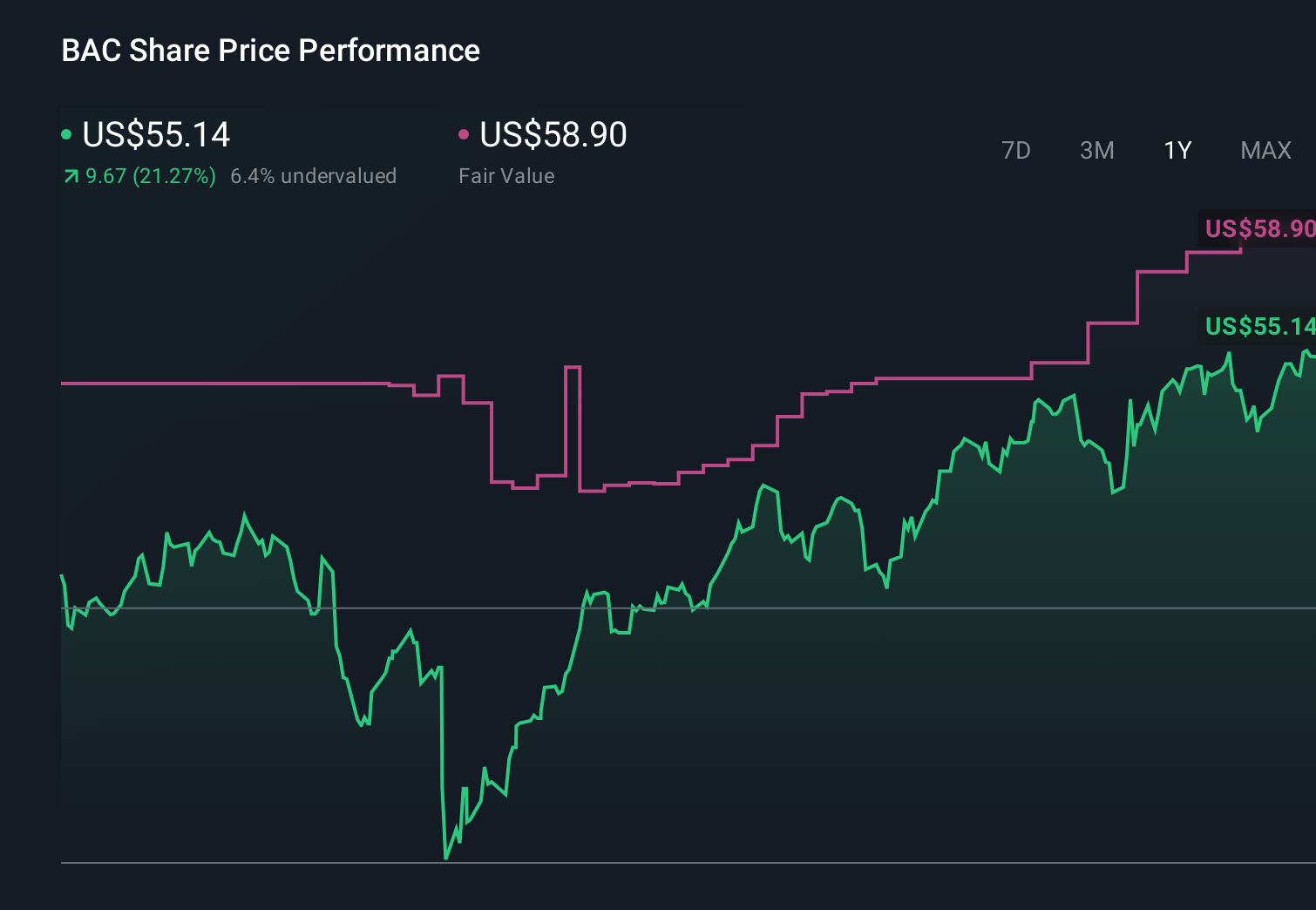

Bank of America's narrative projects $133.5 billion revenue and $36.8 billion earnings by 2029. This requires 6.8% yearly revenue growth and a $6.5 billion earnings increase from $30.3 billion today.

Uncover how Bank of America's forecasts yield a $62.72 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Eight fair value estimates from the Simply Wall St Community span roughly US$58 to US$67.61 per share, showing how far apart views on upside can be. Against that backdrop, the bank’s reliance on digital investments and interest rate management to support net interest income gives you a concrete set of assumptions to test your own expectations about future performance.

Explore 8 other fair value estimates on Bank of America - why the stock might be worth just $58.00!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank of America research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.