Should Carvana’s (CVNA) Record 2025 Results and $1.23 Billion Equity Raise Require Action From Investors?

Carvana Co. Class A CVNA | 313.91 | +0.58% |

- In February 2026, Carvana reported fourth-quarter 2025 and full-year results showing revenue rising to US$5.60 billion and US$20.32 billion respectively, alongside sharply higher net income and earnings per share.

- At the same time, Carvana completed a US$1.23 billion follow-on equity offering and outlined long-term ambitions to scale annual retail unit sales to millions, underscoring management’s focus on funding and executing further expansion.

- Against this backdrop of record profitability and fresh capital raising, we’ll examine how these results reshape Carvana’s high-growth investment narrative.

Invest in the nuclear renaissance through our list of 84 elite nuclear energy infrastructure plays powering the global AI revolution.

Carvana Investment Narrative Recap

To own Carvana, you have to believe its online used-car model can keep scaling profitably despite heavy operational demands in reconditioning, logistics and marketing. The latest earnings and the US$1.23 billion equity raise appear to reinforce the key near term catalyst of sustaining profitable growth at higher volumes, while the biggest risk remains whether Carvana can manage rising operating complexity without eroding its hard-won margins.

The follow-on equity offering completed in February 2026 stands out in this context, because it increases Carvana’s financial flexibility as it pursues its long term ambition of selling millions of units annually. That extra capital may matter for funding inspection, repair and logistics capacity, which sit right at the heart of both the company’s growth catalyst and the risk that costs per vehicle creep higher if utilization or efficiency fall short.

Yet beneath the strong recent results, investors should still pay close attention to rising operational costs and margin pressure risks that could...

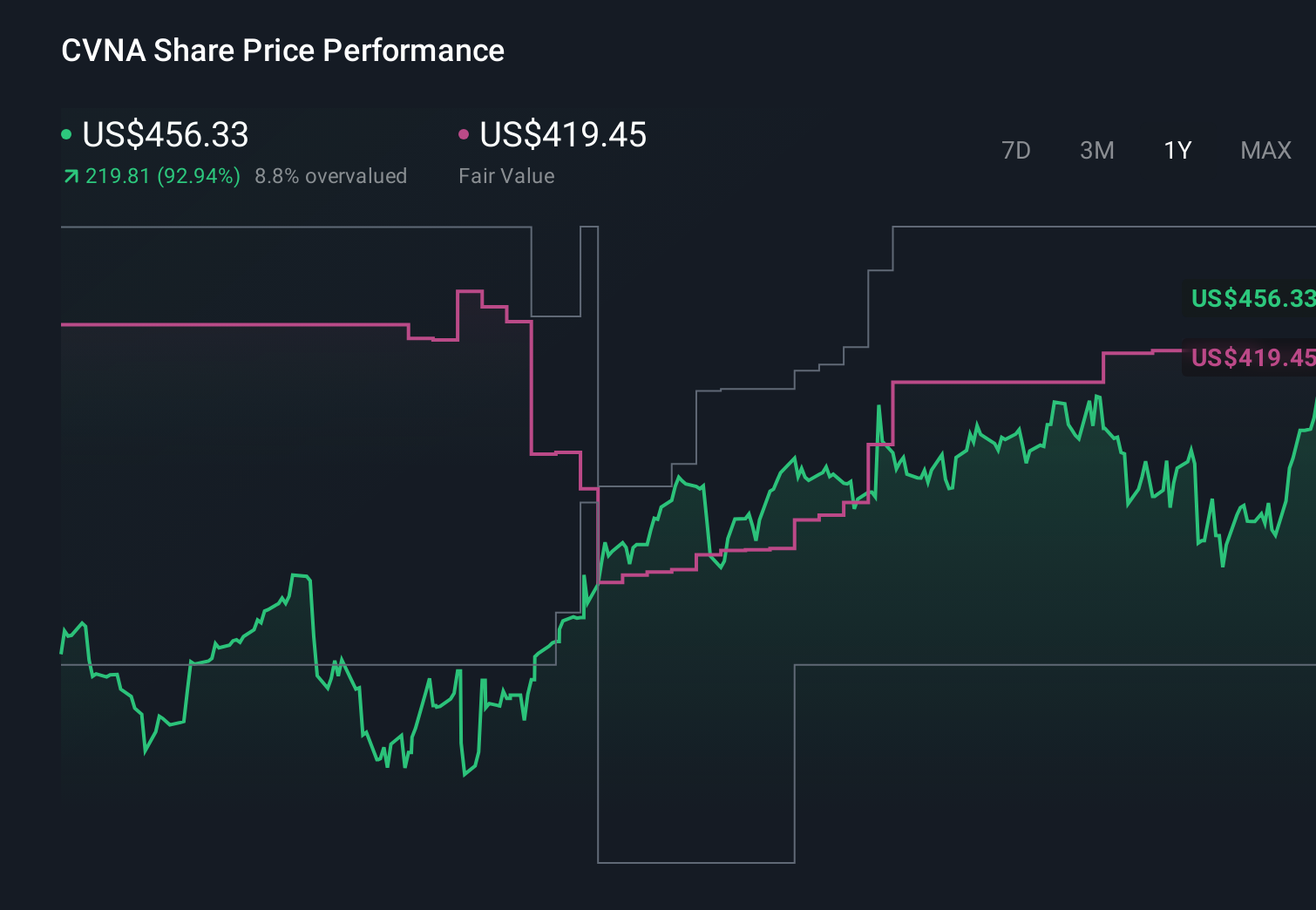

Carvana's narrative projects $33.2 billion revenue and $2.2 billion earnings by 2028.

Uncover how Carvana's forecasts yield a $481.27 fair value, a 49% upside to its current price.

Exploring Other Perspectives

Some of the lowest priced analysts were assuming Carvana would earn about US$1.1 billion on US$26.8 billion of revenue by 2028, which is a much more cautious view than the upbeat growth story implied by recent results and expansion plans. You can use that more pessimistic backdrop to stress test your own expectations and see how new information like this earnings beat and capital raise might shift both the bullish and bearish narratives over time.

Explore 16 other fair value estimates on Carvana - why the stock might be worth as much as 86% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Carvana research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.