Should Deere’s (DE) Expected Q2 Profit Drop Reshape How Investors View Its Precision Tech Story?

Deere & Company DE | 0.00 |

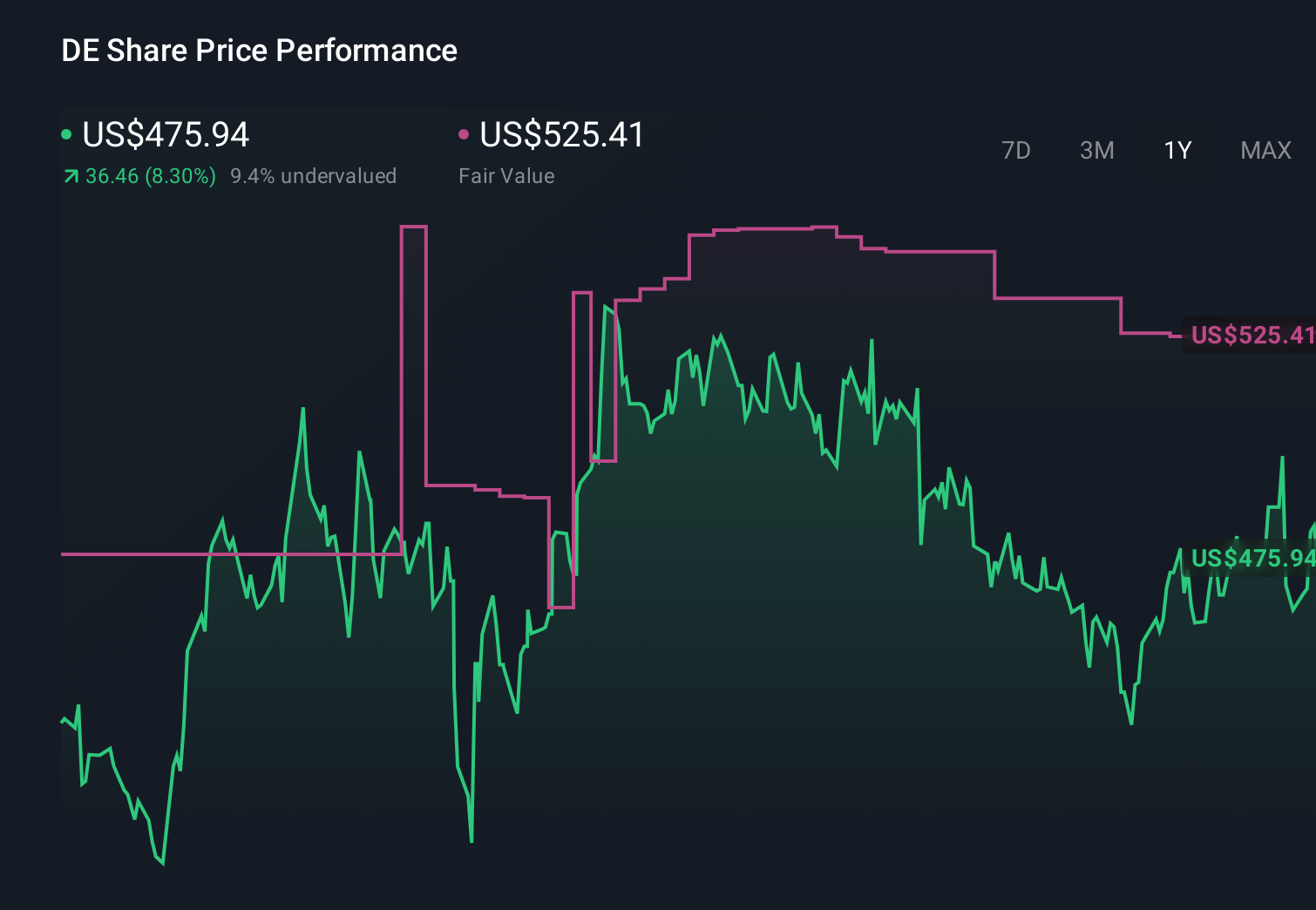

- Deere & Company is scheduled to report its second-quarter 2026 results on Thursday, May 21, with analysts expecting diluted EPS of US$5.81, about a 12.5% decline from the same quarter a year earlier.

- This anticipated profit drop puts fresh focus on whether Deere’s precision agriculture, automation technologies, and cost initiatives can offset weaker near-term earnings.

- We’ll now examine how the expected double-digit profit decline shapes Deere’s investment narrative built around precision tech and margin expansion.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

Deere Investment Narrative Recap

To own Deere, you need to believe its precision technology, automation and cost discipline can support margins through volatile agricultural and construction cycles. The expected 12.5% drop in Q2 diluted EPS to US$5.81 sharpens attention on whether these efforts are gaining traction in the near term. For now, this earnings disappointment does not appear to fundamentally alter the core long term thesis, but it does keep execution risk and end market softness front and center.

Against this backdrop, Deere’s recent settlement of U.S. “right to repair” litigation is particularly relevant. By resolving a prominent legal overhang while maintaining customer access to repair resources, Deere removes a source of uncertainty around its aftermarket and precision tech ecosystem. That clarity matters as investors watch how the company’s software, automation and data driven services contribute to margins at a time when headline earnings are under pressure.

Yet, while precision tech and cost cuts look promising, investors should be aware that margin pressure from tariffs and pricing competition could still...

Deere's narrative projects $47.6 billion revenue and $8.4 billion earnings by 2029. This assumes fairly flat yearly revenue and an earnings increase of about $3.6 billion from $4.8 billion today.

Uncover how Deere's forecasts yield a $665.10 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were projecting earnings to reach about US$10.3 billion on higher margins, which contrasts sharply with today’s weaker EPS outlook and shows how much opinions can differ.

Explore 4 other fair value estimates on Deere - why the stock might be worth just $655.00!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Deere research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Deere research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Deere's overall financial health at a glance.

No Opportunity In Deere?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 19 early-stage AI stocks could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.