Should EPD’s Q1 Earnings Jump and AI-Linked Build-Out Require Action From Enterprise Products Partners (EPD) Investors?

Enterprise Products Partners L.P. EPD | 0.00 |

- Enterprise Products Partners recently reported strong first-quarter 2026 results, with net income attributable to common unitholders rising to US$1.48 billion and quarterly cash distributions of US$0.55 per common unit, alongside US$116 million of unit buybacks under its multi-year repurchase program.

- At the same time, the partnership is advancing nearly US$5.00 billion of capital projects, including new gas processing plants and pipeline expansions tied to growing natural gas demand from AI data centers, reinforcing its long-running focus on income and infrastructure growth for unitholders.

- We’ll now examine how Enterprise Products Partners’ robust first-quarter earnings and ongoing multi-billion-dollar infrastructure build-out affect its existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 39 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to be comfortable with a midstream business that emphasizes steady income, incremental volume growth and large, multi‑year projects. The strong first quarter, higher net income and maintained cash distribution support that case, while the key short term catalyst remains execution on new gas processing and pipeline projects. The biggest current risk, the partnership’s sizeable debt load in a changing rate and credit market, is unchanged by this quarter’s news.

The most relevant recent update is Enterprise’s nearly US$5.0 billion capital program, including new gas processing plants and pipeline expansions linked to rising natural gas demand from AI data centers. Together with completed Permian plants and export projects, these investments are central to the volume driven earnings catalyst investors are watching, even as analysts flag that commodity price volatility and narrowing spreads could temper the benefit of spread optimization over time.

But investors should also recognize how Enterprise’s high debt and leverage targets could interact with shifting interest rates and credit conditions if...

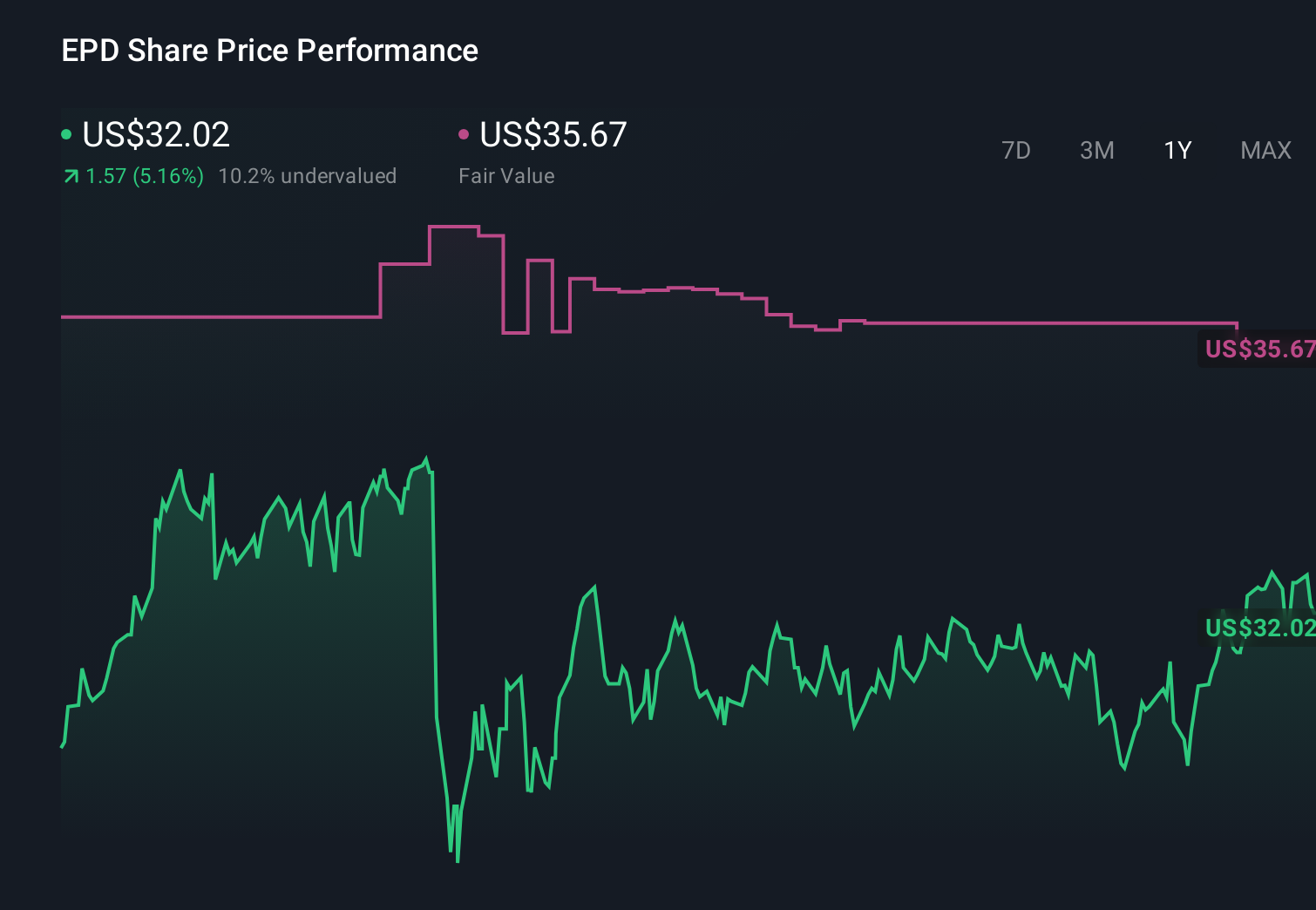

Enterprise Products Partners' narrative projects $61.1 billion revenue and $7.2 billion earnings by 2029. This requires 5.1% yearly revenue growth and about a $1.4 billion earnings increase from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $40.05 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Six members of the Simply Wall St Community currently value Enterprise Products Partners between US$34.42 and US$92.22 per unit, reflecting very different expectations. When you weigh those views against the importance of successful execution on the US$5.0 billion project pipeline, it is worth exploring several alternative opinions on how that build out could influence future performance.

Explore 6 other fair value estimates on Enterprise Products Partners - why the stock might be worth 10% less than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 33 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.