Should Japan’s Optune Lua Reimbursement Win Reframe NovoCure’s (NVCR) Access and Utilization Story?

NovoCure Ltd. NVCR | 10.28 | -2.56% |

- In early March 2026, NovoCure reported that Japan’s Ministry of Health, Labour and Welfare approved National Health Insurance reimbursement for Optune Lua for adults with unresectable advanced or recurrent non-small cell lung cancer progressing after platinum-based chemotherapy.

- This milestone not only broadens access to NovoCure’s Tumor Treating Fields technology in a key oncology market, but also adds a new reimbursed indication to support its growing therapy ecosystem.

- Next, we’ll explore how Japanese reimbursement for Optune Lua may influence NovoCure’s investment narrative around access, utilization, and growth.

Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

NovoCure Investment Narrative Recap

To own NovoCure, you need to believe Tumor Treating Fields can become a meaningful part of standard care across several solid tumors, while the company gradually improves its loss-making profile. The key near term catalyst remains broader access and utilization in non small cell lung cancer, and Japan’s national reimbursement for Optune Lua directly addresses prior concerns about uneven coverage, though it does not fully resolve the larger risk around persistent losses and dependence on a single technology platform.

Among recent announcements, the company’s 2026 revenue guidance of US$675 million to US$705 million is particularly relevant. The new Japanese reimbursement decision sits alongside that outlook and may shape how investors think about near term access driven growth relative to those targets, especially when viewed together with ongoing launches and the continued need to control costs while scaling the therapy base.

Yet against this progress, investors should still pay close attention to the unresolved risk around NovoCure’s continued net losses and...

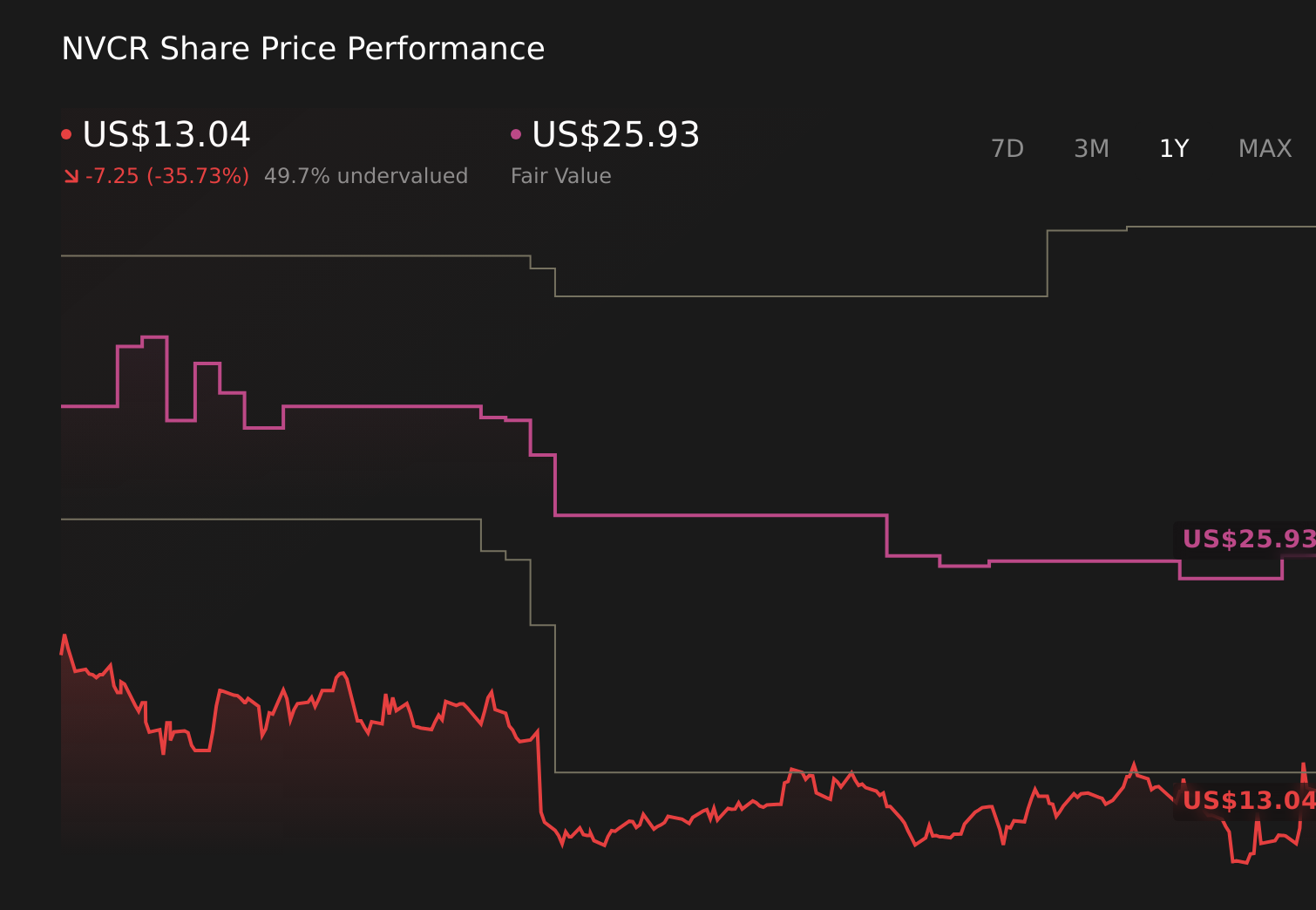

NovoCure's narrative projects $863.5 million revenue and $107.8 million earnings by 2028.

Uncover how NovoCure's forecasts yield a $25.93 fair value, a 101% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling revenues near US$930 million and positive earnings by 2028, so if you view Japanese reimbursement as a sign that access barriers might ease faster than consensus expects, you may see more upside than the baseline narrative. Those bullish forecasts assume a quicker shift toward profitability that others see as uncertain, and this new approval could eventually push perspectives even further apart.

Explore 4 other fair value estimates on NovoCure - why the stock might be worth just $25.93!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your NovoCure research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free NovoCure research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NovoCure's overall financial health at a glance.

Interested In Other Possibilities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Uncover the next big thing with 28 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.