Should Jefferies’ Downgrade and Rising Reduced‑Risk Competition Require Action From Philip Morris (PM) Investors?

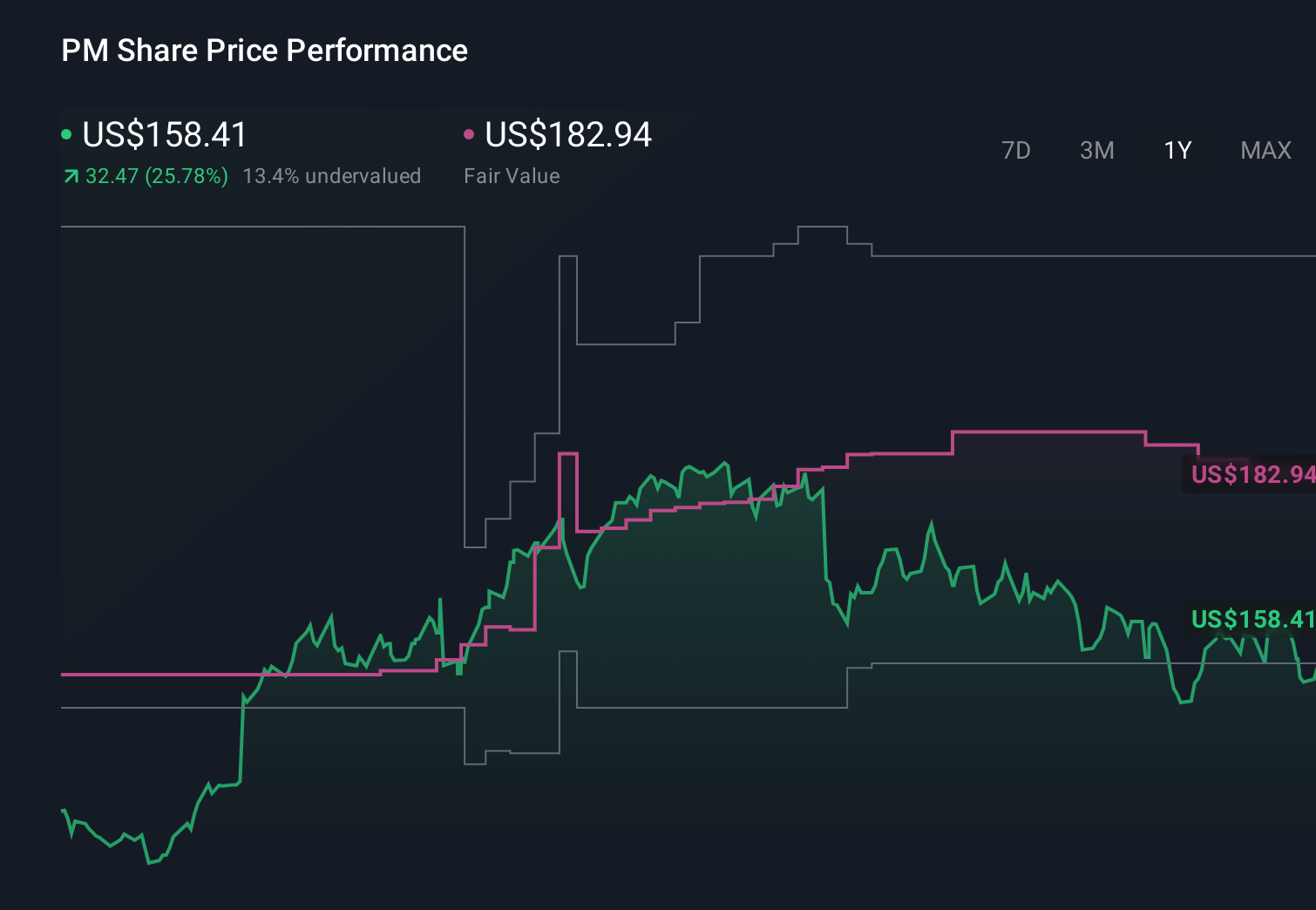

Philip Morris International Inc. PM | 158.10 | +0.49% |

- In recent days, Jefferies downgraded Philip Morris International, citing mounting competitive pressure from British American Tobacco and Japan Tobacco in nicotine pouches and heated tobacco products despite Philip Morris International’s continued multibillion‑dollar US investment program since 2022.

- An interesting wrinkle is that this more cautious analyst stance arrives even as Philip Morris International maintains very strong gross margins and robust free cash flow generation, underscoring the tension between its financial strength and a more crowded market.

- Next, we’ll examine how rising competition in reduced‑risk nicotine products could influence Philip Morris International’s broader investment narrative and risk profile.

These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

What Is Philip Morris International's Investment Narrative?

To own Philip Morris International today, you really have to believe its pivot toward reduced‑risk nicotine products can offset pressure in traditional cigarettes while justifying a relatively full earnings multiple and a sizeable debt load. The short term story has revolved around execution on IQOS and ZYN, regulatory progress like the IQOS ILUMA MRTP process, and the company’s ability to keep translating its strong margins and free cash flow into dividend growth. Jefferies’ downgrade adds a new wrinkle here, because it explicitly questions how durable PMI’s product and pricing edge is as British American Tobacco and Japan Tobacco step up competition in heated tobacco and pouches. The market’s firm share price and only modest discount to analyst targets suggest this concern is being acknowledged, but not treated as thesis breaking for now.

However, the tension between rich valuation and intensifying competition is something investors should keep front of mind. Philip Morris International's shares have been on the rise but are still potentially undervalued by 20%. Find out what it's worth.Exploring Other Perspectives

Fair value estimates from 11 Simply Wall St Community members span roughly US$158 to just above US$221, showing wide dispersion in how people weigh PMI’s strengths and risks. Some see room in those community targets relative to recent prices, while others are more cautious given the tougher competitive backdrop in reduced risk products and PMI’s high earnings multiple. It is worth considering these different viewpoints alongside the shifting risk profile before reaching any firm conclusion.

Explore 11 other fair value estimates on Philip Morris International - why the stock might be worth 11% less than the current price!

Build Your Own Philip Morris International Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Philip Morris International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Searching For A Fresh Perspective?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find companies with promising cash flow potential yet trading below their fair value.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.