Should MasTec’s (MTZ) AI‑Driven Backlog Surge and Higher 2026 Guidance Require Action From Investors?

MasTec, Inc. MTZ | 0.00 |

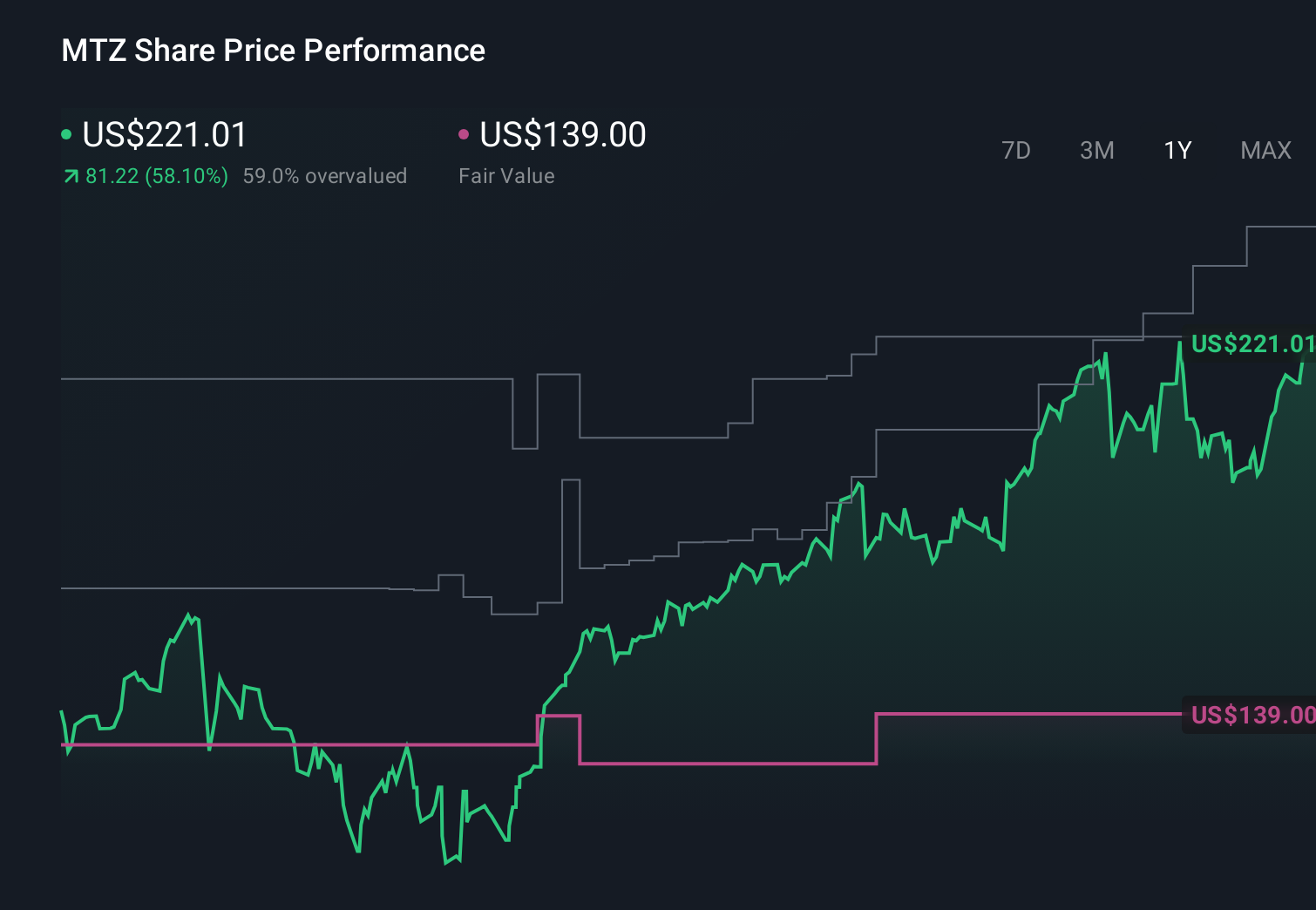

- Earlier this week, MasTec reported strong first‑quarter 2026 results, with revenue rising 34% year over year, a record 18‑month backlog of US$20.30 billion, and higher full‑year revenue and adjusted EBITDA guidance driven by power delivery, clean energy, and data‑center‑related projects.

- A key takeaway is how accelerating AI and data‑center electricity demand is feeding directly into MasTec’s grid modernization and transmission work, deepening its exposure to long‑duration infrastructure spending.

- We’ll now explore how the upgraded 2026 EBITDA outlook and record backlog may reshape MasTec’s existing investment narrative and risk profile.

Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

MasTec Investment Narrative Recap

To own MasTec, you need to believe that long term demand for grid modernization, clean energy, and AI driven data center infrastructure will keep translating into profitable work across its core segments. The upgraded 2026 outlook and record US$20.30 billion backlog support the near term growth catalyst, but they also heighten the key risk that project delays or execution issues could pressure already thin margins if this backlog does not convert as expected.

The most relevant recent development is MasTec’s lift in full year 2026 revenue and adjusted EBITDA guidance following its first quarter 2026 results. Management tied this upgrade directly to stronger activity in Power Delivery, clean energy and data center related work, which are also central to the bull case that MasTec can turn its record backlog into sustained earnings growth, while still leaving open questions about how consistently it can execute such a large, complex project slate.

Yet investors should also be aware that if project awards become lumpier or key customers delay spending, MasTec’s record backlog could quickly turn from a strength into a source of...

MasTec's narrative projects $20.3 billion revenue and $880.9 million earnings by 2029.

Uncover how MasTec's forecasts yield a $348.72 fair value, a 16% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming MasTec would reach about US$21.6 billion in revenue and US$848.8 million in earnings by 2029, which is far more cautious than the consensus and underlines how much disagreement there is about whether today’s backlog and data center power demand can consistently translate into the kind of profitable growth you might be expecting.

Explore 6 other fair value estimates on MasTec - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your MasTec research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MasTec research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MasTec's overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.