Should nLIGHT’s New 70kW Laser Weapon and 2026 Outlook Require Action From nLIGHT (LASR) Investors?

NLIGHT, INC. LASR | 0.00 |

- In late February 2026, nLIGHT, Inc. reported full-year 2025 revenue of US$261.33 million and a net loss of US$23.47 million, and has since guided first-quarter 2026 revenue to between US$70 million and US$76 million while preparing to showcase a newly developed 70kW-class Laser Weapon System at the March Pacific Operational Science & Technology Conference.

- This combination of expanding high-energy laser weapon offerings and continued deliveries to U.S. and allied defense programs highlights nLIGHT’s deepening role in directed-energy solutions for countering airborne and missile threats across multiple military domains.

- Next, we’ll explore how nLIGHT’s new 70kW-class laser weapon system could influence its defense-focused investment narrative and growth mix.

Explore 22 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

nLIGHT Investment Narrative Recap

To own nLIGHT, you have to believe its high‑energy laser technology can convert a growing defense footprint into a more durable business, even as the company remains unprofitable. The latest 2025 results and Q1 2026 revenue guidance support defense momentum, while the new 70kW‑class Laser Weapon System underscores the key near term catalyst: winning and executing on large directed‑energy programs. The biggest risk is still concentration in U.S. and allied defense budgets, which could magnify any program delays or funding shifts.

Among recent announcements, the expanded Longmont, Colorado facility stands out alongside the 70kW‑class system news. Added manufacturing space for high‑energy lasers directly supports nLIGHT’s push to scale deliveries for U.S. Department of War programs and allied customers, which ties closely to the defense‑driven growth story. If amplifier production and beam‑combined system output ramp smoothly, that could reinforce the company’s role in directed‑energy deployments and its ability to support higher volumes across key programs.

Yet behind the defense excitement, investors should be aware that concentrated government demand could quickly become a headwind if...

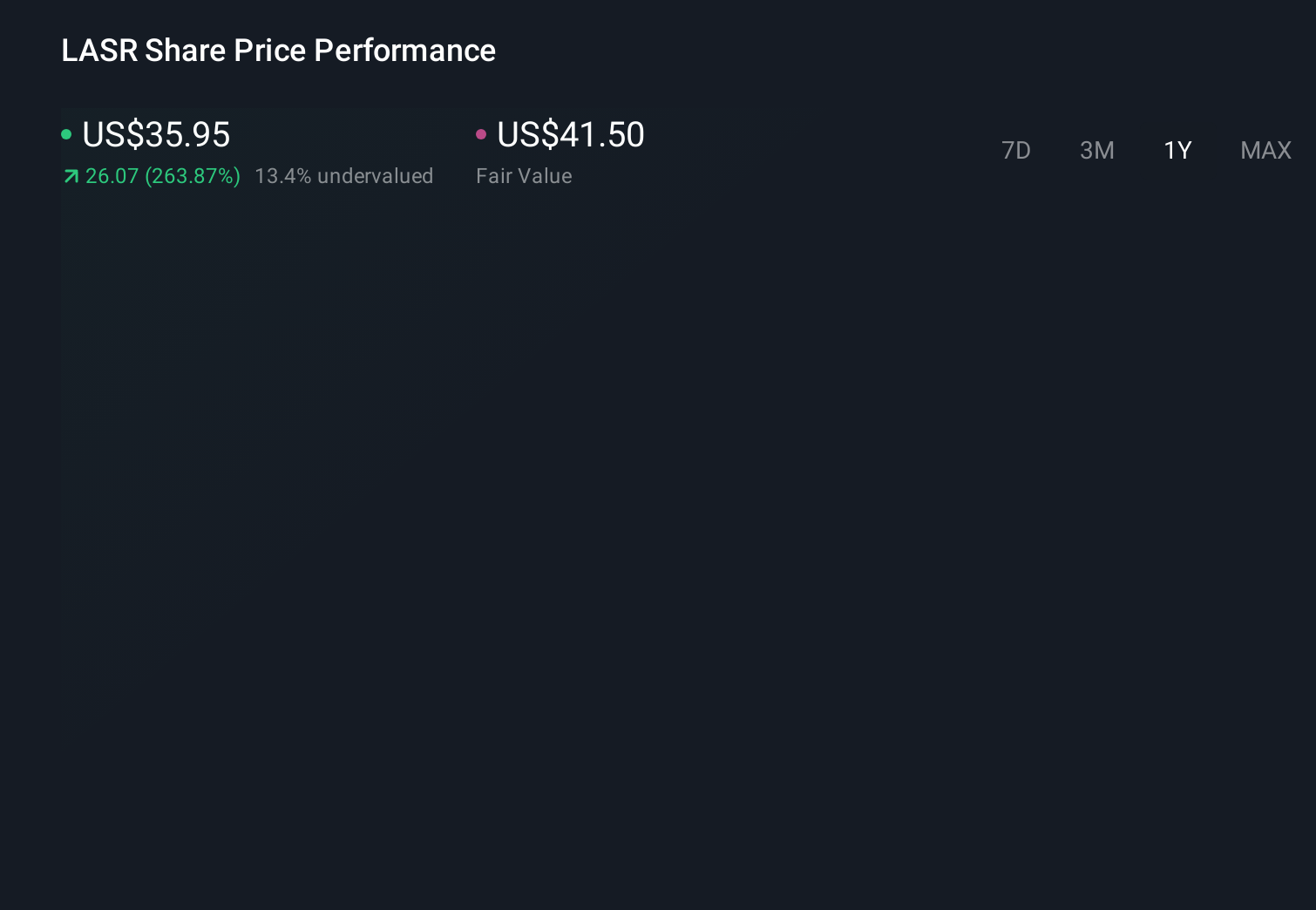

nLIGHT's narrative projects $310.5 million revenue and $28.1 million earnings by 2028.

Uncover how nLIGHT's forecasts yield a $66.75 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts already expected nLIGHT to lift annual revenue toward about US$292 million and earnings to roughly US$26 million in a few years, but this new 70kW system and rising defense exposure might either support that upbeat view or highlight the contrasting risk that heavy reliance on government contracts leaves the story far more fragile than those forecasts suggest.

Explore 6 other fair value estimates on nLIGHT - why the stock might be worth as much as 14% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your nLIGHT research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free nLIGHT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate nLIGHT's overall financial health at a glance.

Want Some Alternatives?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 49 companies with promising cash flow potential yet trading below their fair value.

- Capitalize on the AI infrastructure supercycle with our selection of the 35 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.