Should Paychex’s Q4 Earnings Outlook and Client Trends Require Action From Paychex (PAYX) Investors?

Paychex, Inc. PAYX | 0.00 |

- In the past week, Paychex announced it would report its fiscal 2026 fourth-quarter results on June 24, with analysts expecting earnings per share of US$1.31 on revenue of about US$1.61 billion, reflecting solid year-over-year growth and continued profitability.

- An interesting angle is the market’s focus on trends in client retention, new client additions, and interest income, which together may reveal how durable Paychex’s current earnings power really is.

- With analysts watching client retention and revenue momentum closely, we’ll now examine how this upcoming earnings report could reshape Paychex’s investment narrative.

Find 45 companies with promising cash flow potential yet trading below their fair value.

Paychex Investment Narrative Recap

To own Paychex, you need to believe its payroll and HR platform can keep earning solid, recurring fees from a broad base of mostly smaller businesses, even as economic visibility remains mixed. The upcoming June 24 earnings are a key near term catalyst, with client retention, new client wins and interest income under close scrutiny. This update may not materially shift the long term story, but it could sharpen views on margin pressure and demand resilience.

Among recent announcements, the launch of the AI powered WISE intelligence layer across Paychex Flex, Paycor and SurePayroll stands out in the context of this earnings release. With analysts focused on operating efficiency and the margin trajectory, WISE is directly tied to the catalyst of technology driven productivity gains, while also intersecting with the risk that rising expenses and integration complexity could cap the benefit from these tools in the near term.

Yet behind the steady headline numbers, one risk investors should be very aware of is how changing client behavior could quietly pressure...

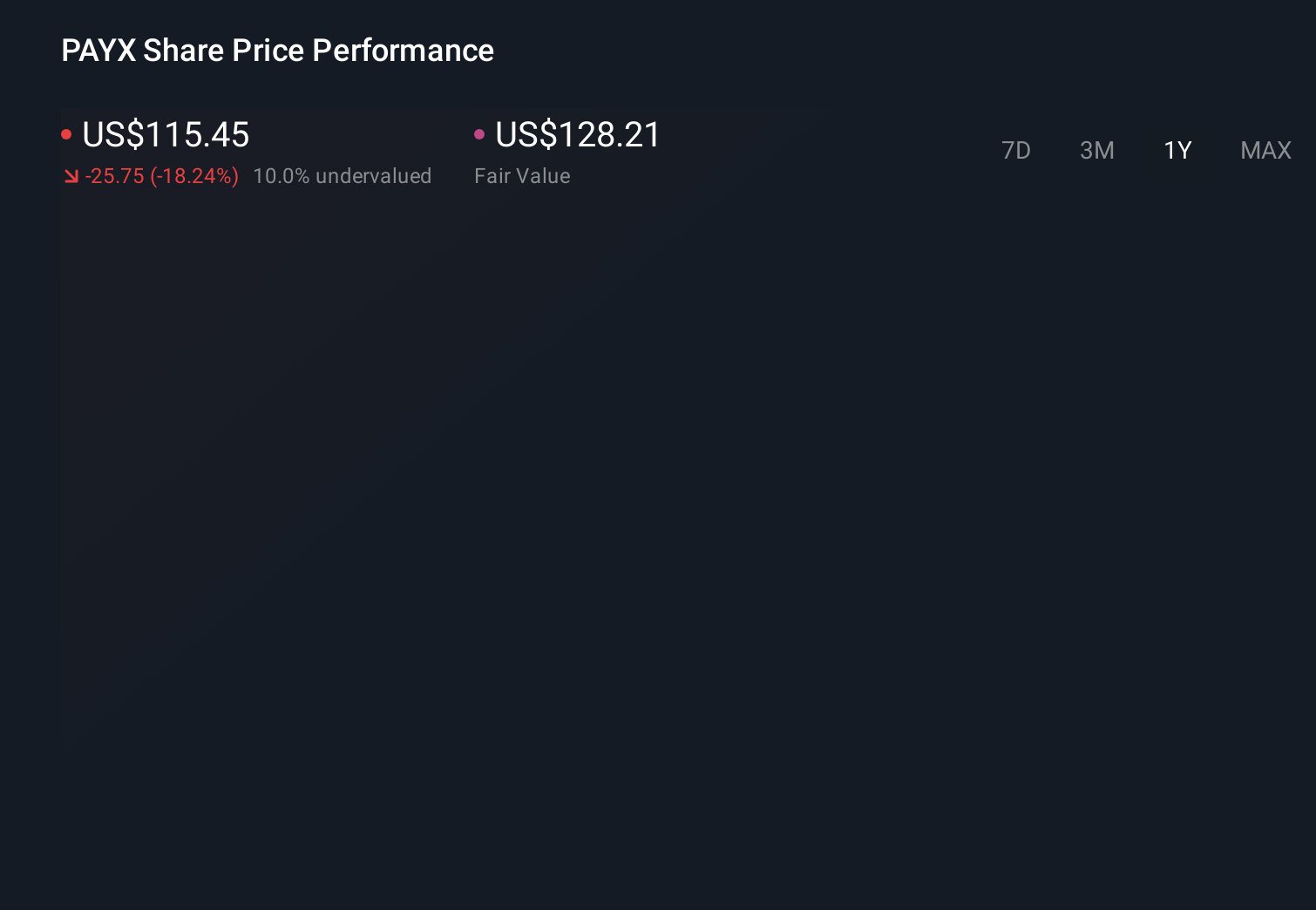

Paychex's narrative projects $7.7 billion revenue and $2.3 billion earnings by 2029. This requires 6.7% yearly revenue growth and about a $0.7 billion earnings increase from $1.6 billion today.

Uncover how Paychex's forecasts yield a $102.07 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming only about 5.5 percent annual revenue growth to roughly US$7.4 billion by 2029 and earnings of about US$2.2 billion, which is a far more cautious view than the consensus. If you compare that to the upside they saw from AI driven productivity and Paycor synergies, you can see how far apart opinions can be, and this latest earnings setup could push those expectations in either direction.

Explore 6 other fair value estimates on Paychex - why the stock might be worth 8% less than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Paychex research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Paychex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paychex's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.